The ongoing COVID-19 pandemic raises the stakes in the debate over surprise medical bills. Consumers’ fear of incurring medical bills could lead some to avoid testing or treatment. While new federal laws require insurers to waive cost-sharing for COVID-19 testing and the associated medical visit, that protection does not extend to treatment. Nor does it prevent balance billing if a patient is treated by an out-of-network provider or facility. Protection, however, may come with the CARES Act Provider Relief Fund. Providers accepting these funds must agree not to send balance bills to any patient for COVID-related treatment. The effectiveness of this protection will depend on its implementation.

Many states already have stepped up to help protect consumers, such as by creating a special enrollment period for state-based marketplace plans, requiring insurers to eliminate cost-sharing for coronavirus testing, and allowing early prescription refills. Several states have even eliminated cost-sharing and deductibles for treatment services.

Balance Billing in a Crisis

Even if cost-sharing is waived for COVID-19 testing or treatment, consumers treated by out-of-network providers run the risk of receiving surprise bills if these providers do not accept the amount paid by insurers. While surprise bills were a problem before the pandemic, patients are more likely to see out-of-network providers as the health system scrambles to respond and patients have less control over who treats them.

Some consumers are better positioned to avoid surprise bills because they have state-regulated insurance and their states have enacted protections. (Employer-sponsored insurance arrangements that are self-funded are not subject to state regulation. The federal Employee Retirement Income Security Act (ERISA) regulates these insurance arrangements.) Congressional attempts to enact a comprehensive federal law to protect all consumers are currently stalled, and emergency federal legislation on the pandemic has not addressed the surprise bills patients incur for COVID-19 testing or treatment.

State Actions in 2020

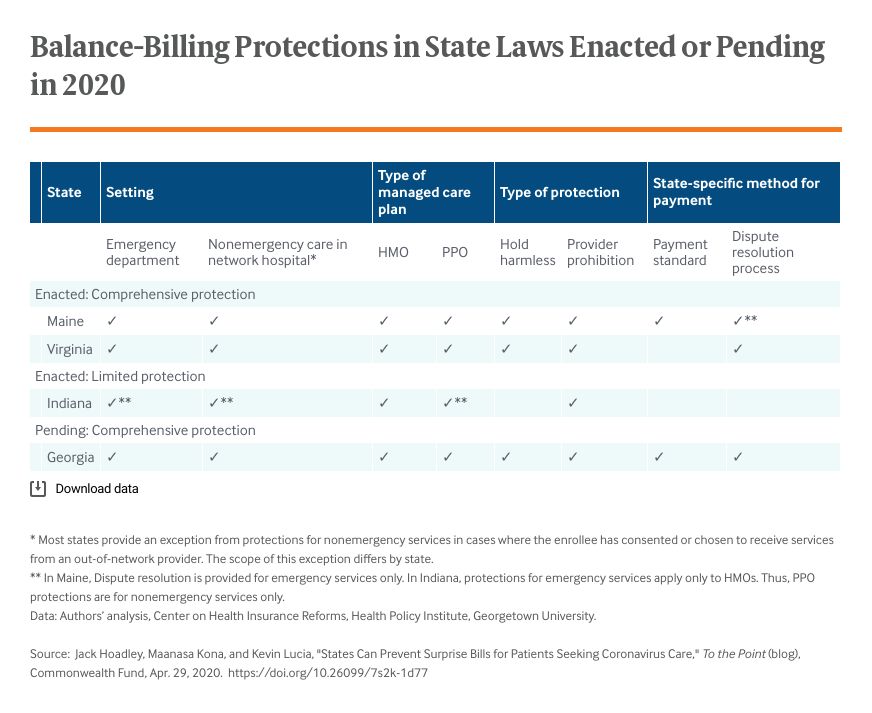

Before the crisis, several states were adding new protections for surprise billing. New laws were enacted this year in Indiana, Maine, and Virginia. As a result, Maine (effective immediately) and Virginia (effective January 1, 2021) residents will have comprehensive protections for plans subject to state regulation. Indiana’s measure adds protection in nonemergency settings and differs from most states; by targeting providers, it seeks to have protections apply to self-insured plans as well as state-regulated plans. Once these new laws are in effect, 15 states will have comprehensive protections and another 14 offer some protection.

In addition, a comprehensive measure in Georgia has passed both legislative chambers and awaits final reconciliation, and proposals have passed one chamber in Hawaii and Kentucky.

State Actions in Response to the Pandemic

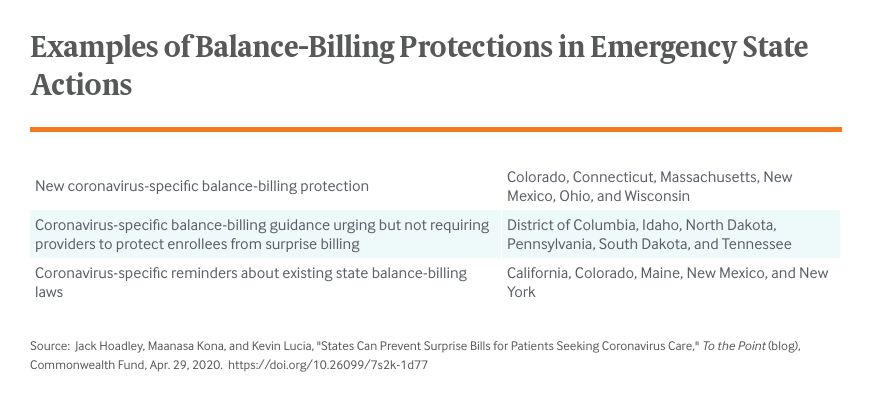

Other states have addressed surprise billing in response to the COVID-19 pandemic. In some states with existing surprise billing laws, such as New York, insurance departments reminded insurers that existing laws apply to coronavirus-related services. Others, such as Idaho and North Dakota, issued bulletins urging, but not requiring, insurers and providers to protect their enrollees from surprise bills.

New protections limited to the pandemic were created in six states, where leaders used emergency powers to add or strengthen consumer protections. In Ohio, for example, HMOs “must ensure coverage for out-of-network emergency services without balance billing,” defined to include testing and treatment for COVID-19. The order also includes a payment standard. A new order in Massachusetts builds on existing protections by creating a payment standard. Colorado and New Mexico declared that treatment related to the coronavirus will be considered emergency care for purposes of their existing protections.

Potential State Actions

Legislatures still in session could take emergency action to protect consumers dealing with the pandemic. As we suggest elsewhere, a short-term fix would ideally ban providers from sending balance bills for coronavirus-related services. And it would require insurers to pay out-of-network providers promptly and limit patients’ out-of-pocket costs to in-network cost-sharing or no cost-sharing. In order to expedite payments to providers in these urgent times, a payment standard could be based on Medicare rates. For example, physicians could be paid 135 percent of Medicare rates — the average commercial rate nationally. Hospitals could be paid at 150 percent of Medicare rates, a modest discount from average commercial rates. Although permanent fixes in many states have incorporated independent dispute resolution or used other payment standards, this approach could be implemented quickly. States might even consider whether they can offer protection retroactively for patients already receiving surprise bills for coronavirus-related services.

States also might consider using emergency powers to hold consumers harmless from surprise medical bills for COVID-19 treatment. The use of emergency powers depends on state law; officials in some states may already have that authority.

Looking Forward

Congress could preempt the need for state action by creating emergency surprise billing protections that apply to all types of insurance. But in the absence of congressional action, states have an opportunity to institute protections for insurance arrangements they can regulate. Fear of incurring high medical bills can discourage people from seeking testing and treatment. With respect to COVID-19, delay in seeking care affects not only those patients but poses a significant public health hazard. States acting during the pandemic may find this a stepping-stone to enacting comprehensive protection.