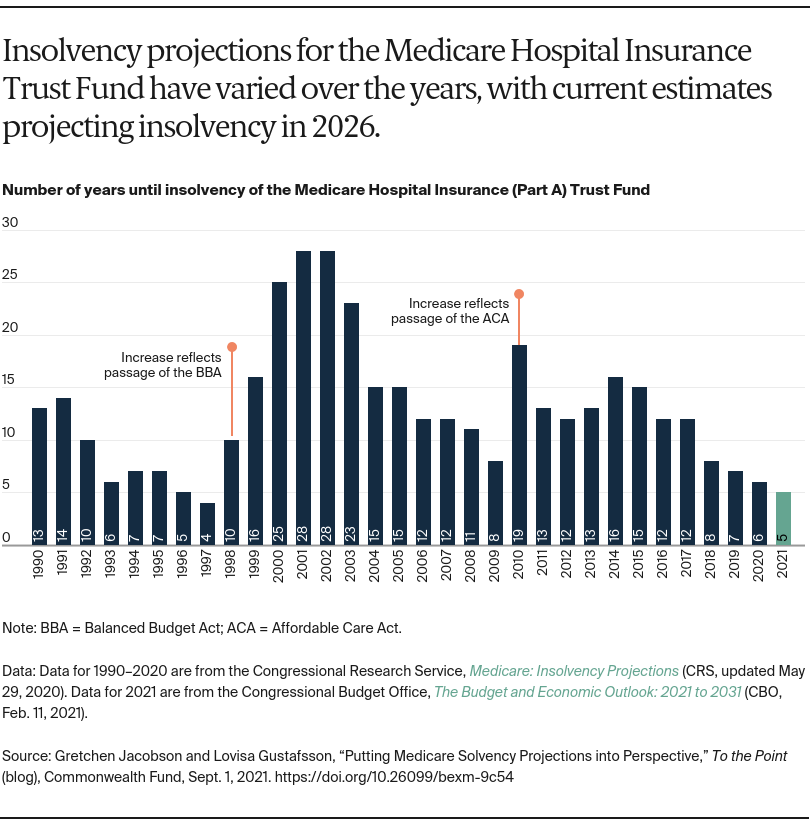

According to recent projections, the Medicare Hospital Insurance (HI) Trust Fund, absent congressional action, will become insolvent in 2026 and no longer be able to fully cover the cost of beneficiaries’ hospital bills. This was affirmed by the recently published report from the Medicare Board of Trustees, and by the Congressional Budget Office (CBO). These projections have not changed from estimates made prior to the COVID-19 pandemic, which leads to the question: Did the pandemic have any effect on Medicare’s finances?

The solvency of the Medicare HI Trust Fund is affected by both revenue into the trust fund and federal spending for Medicare Part A, which covers inpatient hospital care, skilled nursing facility care, hospice care, and home health care. The primary source (88% in 2019) of revenue to the trust fund is payroll taxes, meaning that any increase or decrease in total payroll taxes will affect its financial health. The economic recession and unemployment related to the pandemic raise questions about the volume of payroll taxes flowing into the trust fund. Surprisingly, the pandemic seems to have had relatively little impact on payroll taxes, with actual payroll taxes collected in fiscal year 2020 ($1.31 trillion) higher than projected ($1.281 trillion) before the pandemic. The Trustees project that payroll taxes will be slightly lower in 2021 than 2020, and these amounts also will be adjusted for any overpayments or underpayments in taxes made in 2020. By boosting the economy and lowering unemployment, the American Rescue Plan and other economic or job stimuli could help to further increase payroll taxes, thereby improving the solvency of the trust fund.

The net impact of the pandemic on health care spending has been a matter of significant debate. While the system has incurred new costs associated with testing and treatment, including costly hospitalizations for COVID-related care, there also has been care forgone or delayed. Greater spending than projected prior to the pandemic would shorten the life of the trust fund, while lower-than-projected spending would prolong it.

Based on available data, it appears that traditional Medicare spending declined sharply between March and May 2020, but returned to prepandemic levels by June and remained there for the rest of the year. Traditional Medicare spending, which accounts for 54 percent of total Medicare outlays, declined by about 7 percent between January and October 2020, compared with the same months in 2019. Federal spending for Medicare Advantage plans, which accounts for 35 percent of total Medicare spending, did not change during 2020 because the plans receive predetermined capitated payments that are not tied to actual use of services. Medicare Part D spending, which accounts for the remaining 11 percent of spending, also did not materially change during the pandemic. It is not yet clear whether spending will somewhat increase in 2021 or future years because of receipt of postponed care, or poor outcomes because of forgone care. The costs of COVID-related care and vaccinations in future years also could affect projections.

Funds from the HI Trust Fund were used to make advance payments to hospitals and other providers to help provide financial relief from lost revenues resulting from a drop in hospital admissions and other procedures. The advance payments to providers were substantial enough to have a meaningful effect on the HI Trust Fund, particularly if they are not repaid, as some provider groups have advocated. Providers were required to begin repaying the loans one year from the date of issuance, and the administration recently hired contractors to help recoup the payments.

While many feared the pandemic would have a catastrophic impact on Medicare’s solvency, the net effect seems to be small relative to the amount needed to change the life of the trust fund. Nevertheless, about $240 billion in reduced spending for Medicare Part A benefits or additional tax revenue would be needed to extend the solvency of the trust fund through 2029. The pandemic has not accelerated the program’s financial problems, but the trust fund’s insolvency still looms, just five years away. This is the shortest timeline to insolvency in more than two decades. Congress and the administration are considering several options for extending the life of the trust fund and the potential implications for beneficiaries, spending, and the health care system. Medicare solvency presents an important opportunity to implement reforms that make the program more efficient, effective, and equitable, while meeting the needs of beneficiaries.