In early January, the outgoing Biden administration finalized a new national standard that bans credit rating agencies from including medical debt on most consumer credit reports. The new rule, which was slated to go into effect in March, prohibits lenders from considering medical debt when assessing the creditworthiness of borrowers. However, the Trump administration has placed it on hold.

The impact could be significant: unpaid medical bills are the largest source of debt reported to collections agencies. About 15 million people have medical bills on their credit reports, worth an estimated $49 billion.

This new rule isn’t the first of its kind. Several states have also taken action to remove medical bills from credit reports, with at least six states fully prohibiting the practice. In 2023, the nation’s three largest credit rating agencies — Equifax, Experian, and TransUnion — removed medical bills of $500 or less from consumer credit reports along with records of medical bills that had been repaid.

Why remove medical debt from consumer credit reports? What makes medical debt different from other sources of debt?

Historically, medical bills have been the leading source of unpaid bills on credit reports. In 2021, medical debt made up 58 percent of consumer debt on credit reports. A major reason why medical debt surpasses other types of debt is the very high cost of U.S. health care, combined with weaknesses in our health insurance system that leave many people exposed to those costs. And there are other factors that make medical care, and medical debt, unique.

One is the unpredictability and complexity of illness, and patients’ nearly complete dependence on medical professionals to guide their treatment and use of services. Most patients are unable to make quick, informed decisions about which medical services are right for them. Patients often face time constraints, sometimes severe, in getting treatment. And most people lack the knowledge to choose appropriately among medical services, which vary in price and quality, among other dimensions. Getting health care isn’t like buying a refrigerator or car.

Another factor is that the services and medications provided in a hospital — hospital inpatient and outpatient care is the most frequently reported source of medical debt — are based on treatment protocols outside of patients’ control. If patients leave the hospital with bills they can’t afford to pay, their health care crisis can quickly turn into a long-term financial crisis.

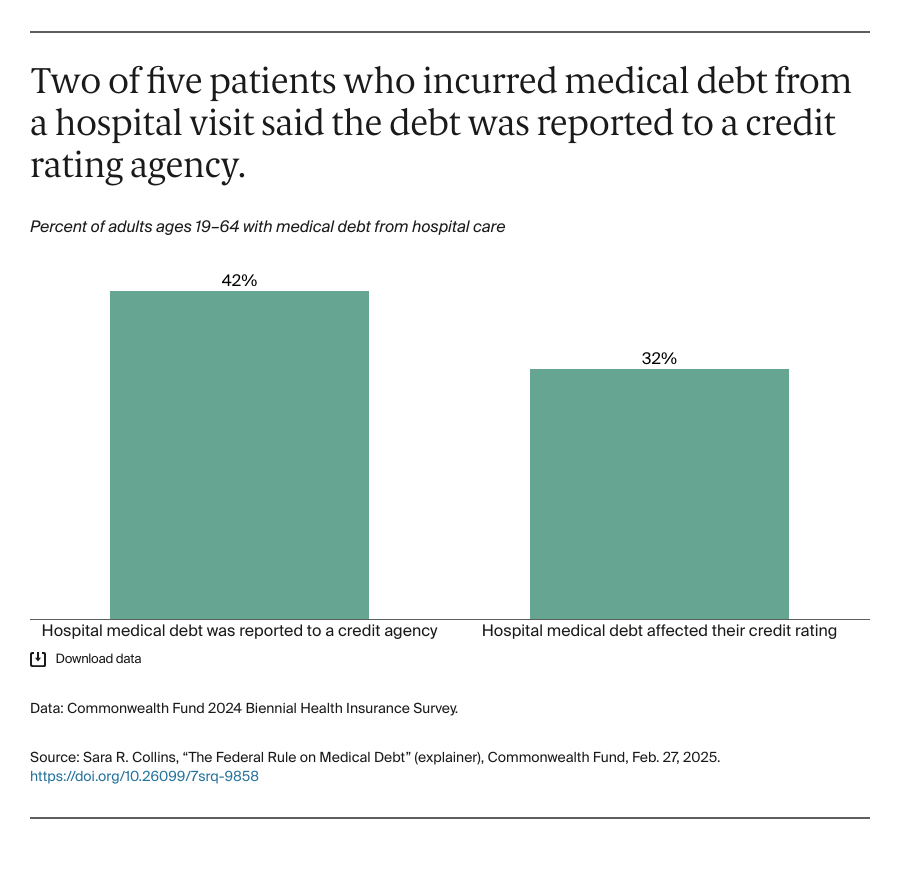

Finally, one of the primary tactics hospitals use to get patients to pay their bills is by reporting the debt to a credit rating agency. Two of five people (42%) with unpaid medical bills from a hospital visit said their debt was reported to a credit rating agency, according to Commonwealth Fund survey data. Nearly one of three people (32%) reported that medical debt from hospital care affected their credit rating.

Who has medical debt and why?

The people most vulnerable to accumulating medical debt are those who lack health insurance and those who have coverage but are underinsured. Although more Americans have health insurance than ever before, an estimated 25 million still don’t have any. Ten states have yet to expand eligibility for Medicaid, and many people who qualify for subsidized insurance remain unaware of their coverage options. Affordability of coverage and eligibility due to immigration status are also factors.

A 2024 Commonwealth Fund survey found that 35 percent of those who were uninsured for all or part of the year reported having medical debt. But being insured doesn’t fully guard against medical bills either. High deductibles and cost sharing in private plans leave 23 percent of working-age adults underinsured, according to the same survey. They are also vulnerable to accumulating debt: 44 percent of those who were underinsured said they were dealing with medical debt.

A recent analysis by the Consumer Financial Protection Bureau found that those with medical debt on their credit reports are disproportionately people with low incomes and people who live in the South. People living in regions that are majority Black or Hispanic are also disproportionately represented among those with medical debt.

How does medical debt affect consumers?

Medical debt creates long-term financial distress. Two of five people who reported debt said they used up all their savings to pay their bills, more than one-third said they cut back on necessities like food and heat, and one-quarter took on another job or worked more hours.

Is medical debt a reliable source of information to predict consumer creditworthiness?

Studies have shown that medical debt has little predictive value for credit underwriting purposes, finding that people whose credit scores were reduced by medical debt were as likely to repay loans as those with higher credit scores. In addition, medical debt may be the result of billing errors, weakening its relevance in assessing credit risk. One study found that almost 6 percent of medical collections had been disputed at some point, three times the rate of disputes on credit card debt.

Because of medical debt’s limited predictive value in evaluating future credit risk, the credit and lending industries have reduced their reliance on it. In 2023, the three major credit agencies removed medical debts under $500 from consumer credit reports. In addition, analyses by credit scoring companies have found that people with medical debt are less likely to default on future credit accounts than those with other types of debt and have adjusted their scoring models to reflect that. Finally, creditors like Fannie Mae and Freddie Mac are treating medical debt information differently than nonmedical debt in their loan underwriting practices.

Does the new rule remove medical debt from all credit reports?

The rule only applies to creditors making lending decisions, such as banks considering mortgage applications. It doesn’t prevent credit reporting agencies from including medical debt on credit reports to other entities like employers or landlords. It also doesn’t protect patients who used a credit card or a medical credit card to pay their bills.

Will the new medical debt rule make a difference?

Even though the rule is not a full ban on medical debt on consumer credit reports, it is likely to make a big difference in lending decisions. The numbers of people with medical bills on their reports, as well as the total amount ($88 billion), dropped significantly after changes made by the three national credit reporting companies in 2023 to eliminate small medical bills on credit reports. The remaining $49 billion are large debt amounts that exceed the $500 threshold.

The Consumer Financial Protection Bureau has estimated that the new credit reporting rule will boost the credit scores of people with medical debt by an average of 20 points, Higher credit scores increase the likelihood that people will gain approval for loans like home mortgages as well as lower their interest rates. One analysis found that a 20-point increase in a person’s credit score could save a home buyer more than $20,000 in interest payments over the life of a 30-year loan.

Will the Trump administration keep the medical debt rule in place?

The Trump administration has not only placed the medical debt rule on hold but also all activities of the Consumer Financial Protection Bureau. Yet recent surveys show there is bipartisan support for the rule, and red and blue states alike have taken action to protect consumers from medical debt.

What more could be done to reduce medical debt?

While removing medical debt from credit reports is an important step forward in helping millions of people improve their credit scores, policymakers have additional opportunities to reduce the accumulation of medical debt in the first place. Following are options for policymakers:

Strengthen federal requirements for nonprofit hospitals regarding the provision of financial assistance or charity care. Such rules could include eligibility and enforcement standards and extend them to for-profit hospitals. Financial assistance could keep people from becoming buried in medical debt after a hospital stay.

Take more action at the state level. As the primary regulators of hospitals, states could continue to fill in the gaps left by federal policy by strengthening financial assistance programs, as more than 20 states have done. Specifically, states could tie hospitals’ provision of charity care to the fulfillment of community benefit requirements for tax-exempt nonprofit hospitals. They could also use Medicaid state-directed payments to incentivize hospitals to relieve past debt and reduce future debt, as North Carolina did in 2024.

Encourage the health care industry to take greater responsibility for its role in the accumulation of medical debt by patients. The United States stands alone among higher-income countries in the accumulation of medical debt among its citizens. Hospital market consolidation, which reduces competition, and the high prices charged for services and prescription drugs contribute to the country’s uniquely high health care costs. Moreover, insurers frequently leave patients vulnerable to high out-of-pocket costs through high plan deductibles, billing errors, and claims denials.

Cover the remaining uninsured. At the federal level, policymakers could pursue opportunities to cover the remaining 25 million people who are uninsured, including filling the Medicaid coverage gap in the 10 states that haven’t expand Medicaid. They also could make the enhanced marketplace premium tax credits permanent. These credits have led to record marketplace enrollment, particularly in red states like Texas that have not expanded Medicaid. Cutting Medicaid and letting marketplace premiums spike in 2026, as some Republicans in Congress have suggested, would likely increase the number of people with medical debt.

By implementing reforms like these, we can help reduce or prevent the terrible consequences that medical debt has for people’s lives.