At least in theory, PBMs’ ability to negotiate manufacturer rebates and manage formularies to promote cost-effectiveness should, over time, help to control growth in drug prices and patient spending. But PBMs have financial incentives that may contribute to growth in drug prices, higher patient out-of-pocket costs, and the closing of independent pharmacies in rural areas and low-income neighborhoods.

These incentives are rooted in the vertical and horizontal consolidation that the PBM sector has undergone in recent years. For example, a PBM can charge insurers a higher amount for a given drug than what the PBM actually reimburses the pharmacy — a practice known as “spread pricing.” PBMs also commonly steer patients to the pharmacies it owns and under-reimburse smaller, independent pharmacies.

Vertical integration and market concentration within the health industry have also led to a lack of competition, with three PBMs accounting for nearly 80 percent of all prescriptions filled. These three PBMs have vertically integrated through mergers and acquisitions that create business relationships among the PBM, pharmacies, an insurer, and providers. With this market power, PBMs can ensure that patients and pharmacies purchase the drugs that allow them to maximize profits — something the federal government has alleged in cases involving insulin medications and specialty generics.

What are the controversies over PBMs?

Rebates. Drug manufacturers argue that the growing rebates they give to PBMs are forcing them to raise list prices for their products. Total manufacturer rebates paid to PBMs reached $334 billion for all brand-name drugs in 2023.

There is a lot of debate over whether PBMs should be able to keep the rebates they receive from drug manufacturers, which generally aren’t publicly disclosed. Although PBMs pass 91 percent of rebates to commercial insurers, according to one estimate, some policymakers and consumer advocates believe PBMs should be compelled to “pass through” all, or a larger portion, of these savings to insurers and other payers. If PBMs were required to do this, they argue, insurers could use the savings to further reduce people’s premiums and cost-sharing payments. Meanwhile, many small insurers and employers say they don’t receive the same share of savings that large insurers receive.

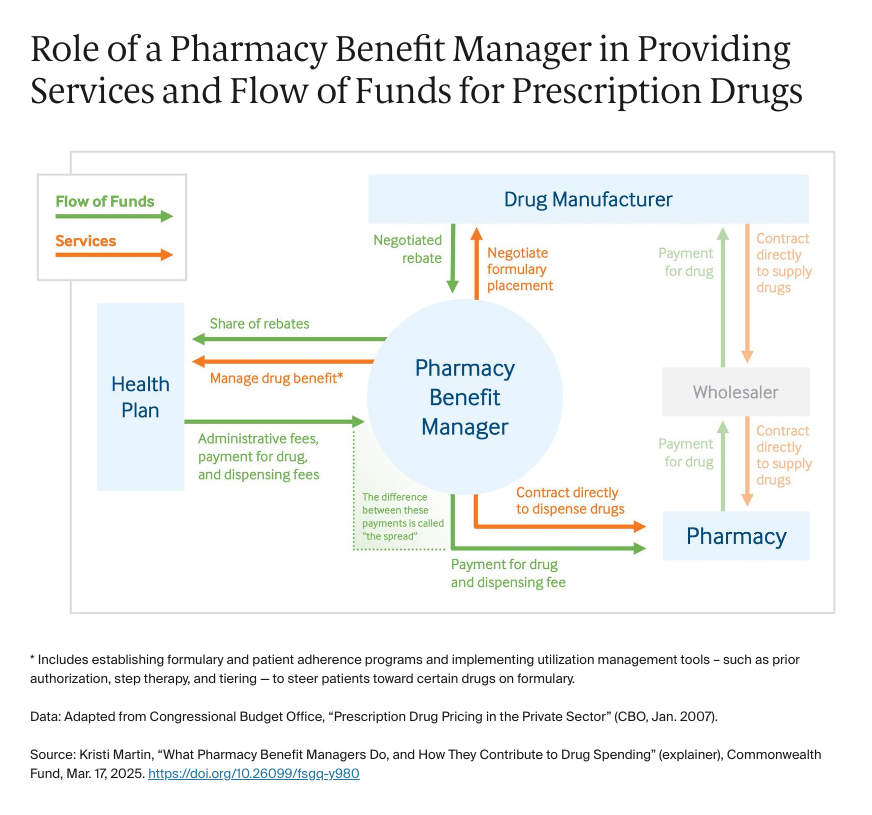

Formularies. One of the primary services PBMs offer to health insurers is developing and managing a list of covered drugs — a formulary. The formulary may include different cost-sharing tiers for generic drugs, preferred brand-name drugs, nonpreferred brand-name drugs, and specialty drugs. Some formularies have as many as seven tiers. In developing a formulary, the PBM negotiates rebates with manufacturers, and rebates are contingent on securing a specific tier for the covered drug. Recent evidence shows that PBMs and manufacturers negotiate rebates that are contingent on excluding lower-cost competitor drugs from the formulary, placing these drugs on a high cost-sharing tier, or applying utilization management rules.

While negotiating additional rebates can lower drug spending, the perverse incentive may encourage PBMs to exclude or prevent access to high-quality, therapeutic alternatives that are cheaper for payer and patient.

Pharmacy contracting. In addition to rebates, PBMs also generate revenue spread pricing, as mentioned above. For generic drugs, PBMs are reimbursed by health plans and employers at prices higher than what they actually pay pharmacies. PBMs then keep the difference. The three largest PBMs generated an estimated $1.4 billion in income from spread pricing for 51 generic specialty drugs over about five years.

Vertical integration. Another concern relates to the industry’s vertical integration, which may incentivize PBMs to steer patients to their affiliated pharmacies, such as specialty or mail-order pharmacies. Independent pharmacies say this creates conflicts of interest that result in higher prescription costs and harms patient access to medicines by creating “pharmacy deserts.” In addition, these pharmacies say it’s difficult for them to ascertain their ultimate payments for drugs based on the contracts they receive from PBMs.

A recent report found that, together, these practices have allowed PBM-affiliated pharmacies for the three largest PBMs to retain nearly $1.6 billion in excess revenue on just two cancer drugs in under three years. A lack of transparency allows these practices to happen, as much of this information is kept confidential from the public, health insurers, and employers.

What reforms have been proposed to address concerns about PBMs?

Policymakers at the federal and state level have considered a number of reforms, many of which have bipartisan support, to regulate PBMs:

- Require greater transparency around rebates. Federal and state policymakers, as well as health insurers, likely need more data on the rebates PBMs receive to gain a more complete understanding of pharmaceutical spending and where reforms may be needed.

- Delink rebates from list prices. Policymakers could restrict PBMs from basing rebates for prescription drugs on their list prices, a practice that incentivizes higher drug list prices. Instead, PBMs could receive a “bona fide service fee” from manufacturers that reflects the fair market value for the services that PBMs provide.

- Standardize contracting terms and practices. Create a level playing field among pharmacies and PBMs by requiring PBMs to 1) provide comprehensive information about pricing prescription drug claims to increase predictability in pharmacy reimbursement, and 2) standardize their pricing terms in pharmacy contracts.

- Ban spread pricing. Ending this practice could help ensure that payers and employers are not overpaying PBMs. A more limited proposal would be to mandate that PBMs update their cost schedules with pharmacies to reflect price increases for generic drugs.

- Clarify and strengthen the “any willing pharmacy” definition. To improve access in pharmacy deserts and ensure that pharmacies are adequately reimbursed, federal and state policymakers could bolster existing rules requiring PBMs to work with any pharmacy that meets their terms and conditions. For example, Medicare Part D plan sponsors and their PBMs are required to include pharmacies in their networks if they accept the plan’s standard contracting terms and conditions and the terms are “reasonable and relevant.” In this instance, policymakers could define “reasonable and relevant,” provide agencies with enforcement tools, and create an easy process for pharmacies to report potential violations by PBMs.

In addition, some experts think that health plans and PBMs could do more to support physicians in prescribing the most cost-effective medications on their patient’s formularies. They also could consider designing high-value formularies, which would encourage PBMs to base formulary decisions and price negotiations on a drug’s comparative health benefits as well as its effect on the total cost of patient care.