A Brief History of Efforts to Enhance Consumer Choice in U.S. Health Care

Historically, U.S. consumers have faced significant barriers in attempting to consider quality and price when making health care purchasing decisions. Forty years ago, patients could only gather information about quality of care by word-of-mouth, at times from their physicians but often also from friends and family. Simultaneously, generous commercial (primarily employer-based) health insurance plans shielded patients from differences in health care prices across physicians and hospitals. In this context, patients lacked both the information and the financial incentives they needed to make most health care choices based on care quality or price.

Spurred by concerns over differences in quality across health care providers, a movement began in the mid-1980s to provide patients with information about their physicians and hospitals in the form of “report cards.” These reporting efforts were meant in part to encourage patients, as well as insurers, doctors, regulators, and government, to use information about quality when making their health care decisions. By the early 2000s, health plans were introducing greater levels of cost sharing in their benefit designs — often in the form of high deductibles — to incentivize patients to consider cost in addition to quality when choosing whether and where to get medical care. Today, this cost sharing is sometimes tied to quality of care or to physician or hospital health care utilization and spending.

The late 2000s saw the emergence of a movement to give consumers access to information about health care prices to help them identify and select the providers offering the highest value. More people became aware that the amounts that physicians, hospitals, and other providers charge for their services often differ dramatically from the amounts insurers actually pay. In the past decade, insurers, employers, and some states have offered price transparency websites or mobile apps that enable comparison of prices across physicians and hospitals. The increasing numbers of patients in health plans with high deductibles or coinsurance have incentives to perform such comparisons, because they can be responsible for large out-of-pocket costs if they use more expensive providers.

Policymakers and payers continue to promote tools to support informed consumer decision-making about whether and when to seek health care. The 2020 Transparency in Coverage rule, finalized by the Centers for Medicare and Medicaid Services, represents the largest federal policy effort to date to increase transparency in health care pricing. The rule requires health plans to disclose actual prices paid as well as estimated patient cost-sharing obligations for specific health care services, thus enabling consumers to shop and compare providers based on cost.

The experience of the past four decades provides an evidence base for understanding whether policies such as this are likely to improve the value of consumer choice. These lessons also could inform the design of future policies.

Key Findings

Patients’ preferences for lower cost and improved quality should prime them to be discerning health care consumers.

Research supports the view that patients highly value information on health care prices and quality, as well as the opportunity to choose their care providers. Recent polls and surveys consistently find that lowering the costs of care and improving quality are top priorities for patients in the U.S.3 Increasingly, surveys find that Americans want more health care price information, are aware that health care prices vary across physicians and hospitals, and understand that a higher price does not always indicate higher quality.4

Americans also value choice in health care. The well-documented public backlash over the rise of managed care in the late 1990s revealed how dearly Americans hold the ability to select certain physicians and hospitals when they access health care.5 Today, having access to a preferred network of physicians and hospitals continues to be the most important feature of health plans for many consumers.6

Decision-making errors because of use of heuristics and biases frequently affect patients’ health care choices.

At the core of efforts to leverage consumer choice to improve value in health care is the notion that patients can 1) make “high value” decisions informed by an understanding of the relative value of medical care and 2) identify differences across providers, weigh them rationally according to their own best interests, and then choose the highest-quality option at the lowest possible price. However, there is considerable evidence showing that for many products and services, consumer choice is subject to limitations in cognition, use of mental shortcuts or heuristics, and systematic biases. Such limitations result in choices that often do not reflect the consumer’s best interests.

For example, instead of assessing the true probability of an event, consumers often judge the likelihood of future events based on how easily they can imagine the event happening or based on whether something like it has happened to them before (even if the prior event is unrelated).7 Consumers are also overly optimistic about their individual chance of experiencing a bad outcome.8 We also are better able to make decisions in our best interests when all costs and benefits occur in the future. But when some costs or benefits are immediate, we are prone to making shortsighted decisions that produce worse outcomes.

Decision-making errors are most likely to occur when choices are complex, involve high stakes, include trade-offs over time, and when consumers have limited personal experience.9 Health care choices often involve all four of these circumstances.

Inconsistencies in health insurance plan choices. A large body of literature has examined the plan choices that patients make. Sometimes these choices are consistent with the consumer health care choice model. For example, patients who use more health care than others consistently choose and remain enrolled in health plans that provide more comprehensive benefits.10 Conversely, patients who use less care tend to select and switch into lower-cost, less-comprehensive plans.

In other ways, patients’ choices can be puzzling. Many people fail to sign up for health insurance coverage when it is low-cost or even free.11 People often choose plans that have higher expected out-of-pocket costs than other available options or that charge more for equivalent benefits; such choices are more common among those with impaired cognition.12 And many people stay in the same plans even when better plans become available.13

Effect of cost sharing on both inappropriate and appropriate care. A market-based strategy to increase the value of health care choices is to increase patient cost sharing. The expectation is that patients will cut back on inappropriate care when out-of-pocket costs for that care are higher. Patients are expected to continue to seek out appropriate care, because it is likely to improve their health and thus remains of value despite the higher cost.

Yet when faced with higher insurance deductibles, many patients have not been able to discriminate between care that is needed and care that is not. Instead, they cut back on all health care, even necessary services such as cancer screenings and colonoscopies.14 Correspondingly, when care is free, patients seek out unnecessary services (for example, emergency department visits for nonurgent care), sometimes even exposing themselves to greater harm.15 This behavior is in opposition to what is expected from a discerning health care consumer.

Low use of preventive care. Use of preventive services such as annual cancer screenings or maintenance medications for chronic conditions is far lower than that recommended in evidence-based guidelines.16 Some of this underuse may reflect true patient preferences — engaging in riskier behaviors, for example — or barriers people face in accessing care. But because we know that choices regarding preventive care can be influenced by intertemporal trade-offs as well as a lack of personal experience with serious illness, it is likely some underuse is because of decision-making errors.17

Making different choices depending on how alternatives are framed. In a world with no decision-making errors, everyone makes the same choices about getting medical treatment, regardless of how alternatives are presented. In reality, patients’ choices usually depend on whether outcomes are presented in terms of the probability of good outcomes versus the probability of bad outcomes.18 And people are much more likely to select an alternative when it is presented as the default option.19 Rates of organ donation, for example, are much lower when the default is to not be a donor.20

Patients are more likely to act like informed consumers when information about quality and prices is tied to incentives and presented in a simple, straightforward manner.

The past two decades have seen a proliferation of physician and hospital quality report cards, financial incentives to encourage patients to use higher-quality and/or lower-priced health care, and health care price transparency tools allowing patients to compare prices of local physicians and hospitals. From this evidence, we can learn about how frequently consumers access or use such information and how these efforts affect patients’ choices.21

Use of report cards. Recent surveys show that even among adults with chronic conditions, only a quarter are aware that information like that provided in quality report cards is available to them, and only one in 10 uses such information to compare hospitals or physicians.22 People rely mostly on informal sources, such as the opinions of physicians, or even on social media sites like Yelp.23 The information contained in report cards is most effective when the number of choices is limited; when results are displayed in a positive direction (for example, higher is better); when nontechnical language is used; and when report cards use familiar symbols, such as up and down arrows, combined with simple terms like “better” or worse” to convey quality, as opposed to numeric quality measures like frequencies and ratios.24

Impact of price transparency. Patients can now access information about the reimbursement their doctors and hospitals receive from insurers and estimates of their actual expected out-of-pocket costs that reflect their health plan benefit design and out-of-pocket spending in the year thus far (for example, whether or not they have satisfied their deducible). This price information is often available via online tools directed at patients. But evidence over the past decade reveals that only a small minority of patients use these websites to obtain price information. Moreover, the availability of this information has generally not led patients to switch to lower-priced providers, nor has it led to decreased spending.25

Impact of high-deductible health plans. People in high-deductible health plans are no more likely than those in lower- or no-deductible plans to choose lower-cost providers, despite having a much larger incentive to shop based on price.26 Rather, high-deductible plans have led patients to indiscriminately limit their use of care, including both high-value and low-value services.27 This holds true whether or not these patients have a health savings account, where pretax dollars can be set aside to pay out-of-pocket health care costs or save for future health care expenses. (Consumer knowledge about health savings accounts and how they work is also low.28) Cost sharing is a blunt instrument, and raising it alone will not lead to higher-value choices.

Promise of incentives for choosing higher-value care. Health insurance benefit designs in which cost sharing is aligned with higher-value health care choices have been more successful. Tiered prescription drug formularies, for example, have led patients to lower their overall use of brand-name medicines and spending — though not without some unintended consequences, including reduced medication adherence.29 Value-based insurance designs, which structure copayments so that patients pay less, or nothing, for drugs or services deemed to be of high value (such as medications consistent with evidence-based guidelines), have improved adherence.30

Similarly, patients in plans with tiered provider networks have lower cost sharing when they choose a physician or hospital assigned to a preferred, or higher-value, tier, based on the insurer’s analysis of provider quality and cost. Tiered networks have led patients away from nonpreferred physicians and hospitals, and they have been associated with 5 percent lower total medical spending than health plans requiring the same cost sharing for all providers.31

Another example is reference pricing benefit design, under which a patient who selects a provider that charges above the health plan’s set price for a service must pay the required cost sharing in addition to the difference between the reference price and the provider’s price. To avoid higher cost sharing, patients must determine which providers have prices below the reference price and select one of them. This process is simpler than comparing prices across many providers and can be made easier when insurance carriers publish lists of such providers. Reference pricing has been associated with the selection of lower-cost alternatives for several medical services. In some cases, patients paid higher cost sharing under reference pricing and, in other cases, lower.32

Rewards programs, on the other hand, pay patients (via check) when they select a lower-price provider. An evaluation of one rewards program found that 1.9 percent of services resulted in a payment.33

Taken together, these responses suggest consumers are more responsive to predictable, well-defined prices that applies to groups of health care services or providers.

Patients want to discuss treatment cost with their physician, but these conversations aren’t happening often.

There are many choices that patients could never make for themselves, given that most people lack in-depth knowledge about their conditions and the potential benefits, costs, and risks associated with different treatments. Patients view their physicians as a trusted source of information not only about their health care needs but about the quality of other physicians and hospitals.34 They rely on their physicians to help with decisions about the quantity and quality of medical care needed, including which specialists to see and which facilities to go to for tests and procedures.35 Moreover, patients and patient advocacy groups are increasingly calling for the inclusion of out-of-pocket costs in patient–provider conversations to help ensure treatment choices are in the patient’s best interest.36

While some conversations around cost-saving strategies and cost–quality trade-offs are taking place, studies of patient–physician interactions during office visits find that providers frequently miss opportunities to engage patients on the topic, even when patients express interest.37 There are likely several reasons: competing demands on physician time, lack of training around initiating and having these conversations, and general unavailability of information on patient out-of-pocket costs in clinical settings. Experts are beginning to understand which strategies may be most effective in promoting and holding meaningful cost conversations, though implementation of these strategies within physician workflow remains a challenge.38

Recent advancements in price transparency may help as well. For example, real-time benefit tools (RTBT), which are designed to be embedded in the electronic medical record, display a patient’s out-of-pocket prescription drug costs for medications during a clinical encounter. They are currently available for prescription drugs only, but wider implementation is expected in part because of a Centers for Medicare and Medicaid Services (CMS) mandate for all Medicare Part D plans to support an RTBT service capable of integrating with at least one prescriber. The goal is for clinicians and patients to use the tools to make medication choices together based on effectiveness and cost. It will be important to watch whether RTBT can improve the value of medication choices.

What Will It Take to Advance Consumerism in U.S. Health Care?

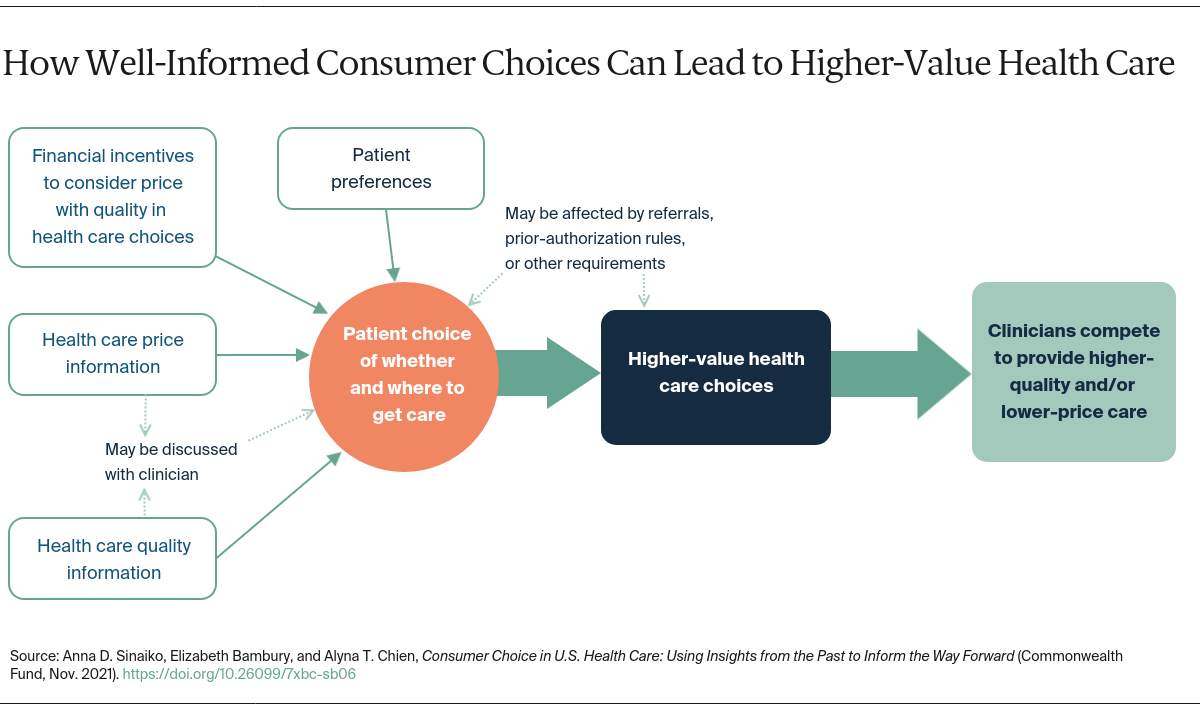

Underpinning policies to increase the amount of price and quality information that consumers have — alone or in combination with policies to change their financial incentives — is the notion that it is the patient seeking care who is the final arbiter of cost–quality trade-offs. Providers, then, have incentives to compete by offering better quality or a lower price. In today’s U.S. health care system, the opportunity for consumers to choose high-value care remains promising, as variations in commercial health care prices within the same market continue to be high and largely unrelated to differences in quality.39

As we have seen, efforts to enhance the value of health care choices by making quality and price information more available, or by employing blunt cost-sharing incentives, have not been very successful. Success will likely require that the three necessary components discussed above — patient financial incentives for selecting lower-cost and higher-quality providers and services, price data, and quality information — be integrated. The evidence also suggests that these efforts simplify choices for consumers, making it is easier for them to learn about options that are most aligned with high value. Policies that promote these outcomes through, for example, improved benefit design or the use of new technologies should continue to be developed and tested. With the knowledge and lessons gained through these efforts, we can learn how information and incentives can be combined to be most effective.

Also important are efforts to make it easier for physicians to partner with patients in their decision-making. With the rising need for and interest in cost-of-care conversations, it may be useful to have deliberate “pauses” or “time-outs” during health care visits so that these discussions can take place.

Role of Purchasers

Employers and other health care purchasers also can play a role in improving the value of patient health care choices. For example, CalPERS, which provides and administers health insurance for California state employees, used quality and price data to develop its reference-pricing benefit design program. That program moved significant numbers of patients to lower-cost facilities for surgeries and selected outpatient tests and procedures.40 Engaging other large purchasers by making marketwide quality metrics and paid prices for physicians and hospitals publicly available could lead to other creative ways of incorporating data with benefit design to drive patients to higher-value choices. It should be noted that in markets where a few large health systems hold significant market power, such strategies are less likely to work, and more regulation might be required to improve efficiency.

Over the past four decades, the amount and breadth of information on health care quality and cost has expanded greatly, as has knowledge about how and when patients use this information to inform their health care choices. Additional change within the health care sector must occur if consumerism is to drive the overall health system toward greater levels of competition, innovation, efficiency, and value.