During February’s State of the Union address, President Trump touted his administration’s efforts to expand access to short-term health plans that do not comply with any of the Affordable Care Act’s (ACA) consumer protections. Short-term plans are often cheaper than ACA-compliant plans because they can deny coverage to people with preexisting health conditions, impose higher cost-sharing, and exclude entire categories of services. Under the Families First Coronavirus Response Act, which amends Medicaid to create a state option for providing COVID-19 testing and related visits for the uninsured, Congress defined people with short-term plans as being among the uninsured.

Advocates of short-term plans argue that they provide sufficient coverage for catastrophic medical situations, such as COVID-19. But while recent federal guidance requires private health insurers to cover COVID-19 testing and cost-sharing for related services, this requirement does not extend to short-term plans, which claim to be covering some costs but not all.

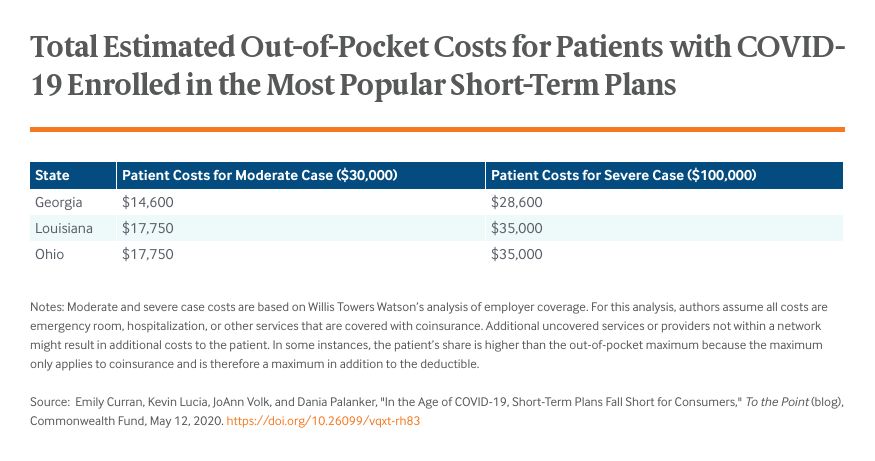

We reviewed plan brochures for 12 short-term plans currently being sold in Georgia, Louisiana, and Ohio and found that people enrolled in them have less financial protection if they need treatment for COVID-19 than people enrolled in ACA plans.

People in Short-Term Plans Likely to Face Coverage Gaps, High Out-of-Pocket Costs, and Nonrenewal

Risks of Coverage Gaps and High Cost-Sharing for Medically Necessary Care

Short-term plans often have major coverage gaps that would extend to COVID-19-related services. Of the 12 short-term plans reviewed, 11 excluded nearly all coverage of prescription drugs, with some providing limited coverage of inpatient prescriptions. At least one plan in every state excluded preventive care like immunizations and most noted that any form of experimental treatment would not be covered, which could include drugs like hydroxychloroquine and remdesivir that are not yet approved or for routine use in treating patients with COVID-19.

Even when services are covered, short-term plans often impose high cost-sharing. Nine of the 12 plans had deductibles of $10,000 to $12,500. COVID-19 patients who require treatment need to pay these amounts before any coverage begins, except in rare instances where some cost-sharing for COVID-19 testing and treatment may be waived. These patients also may be required to meet separate deductibles specific to ER treatment, which we observed in 10 plans. One plan in Louisiana requires consumers who need ER care to first meet a $500 ER deductible, then the plan’s $12,500 deductible, then 30 percent coinsurance. Half the plans set their out-of-pocket maximum at $20,000 or more for a six-month period. Since the deductible does not count as part of the maximum, consumers may be left with $30,000 or more in bills for covered in-network services in the worst situations.