The economic shutdown due to COVID-19 prompted an unprecedented spike in unemployment, with more than 33 million people filing claims since mid-March. Alongside this widespread job loss, the health insurance safety net is being stretched to accommodate the rapid increase in people in need of coverage. The Affordable Care Act’s (ACA) marketplaces, along with Medicaid, are important tools in covering the newly uninsured.

State-Based Marketplaces Work to Enroll the Uninsured

The ACA’s marketplaces provide a source of quality health insurance and financial assistance. State-based marketplaces (SBM) have control over call centers, outreach efforts, and eligibility and enrollment platforms. As a result, states with SBMs have more opportunities to help consumers during the COVID-19 crisis than states relying on the federally facilitated marketplace.

Creating New Opportunities to Enroll

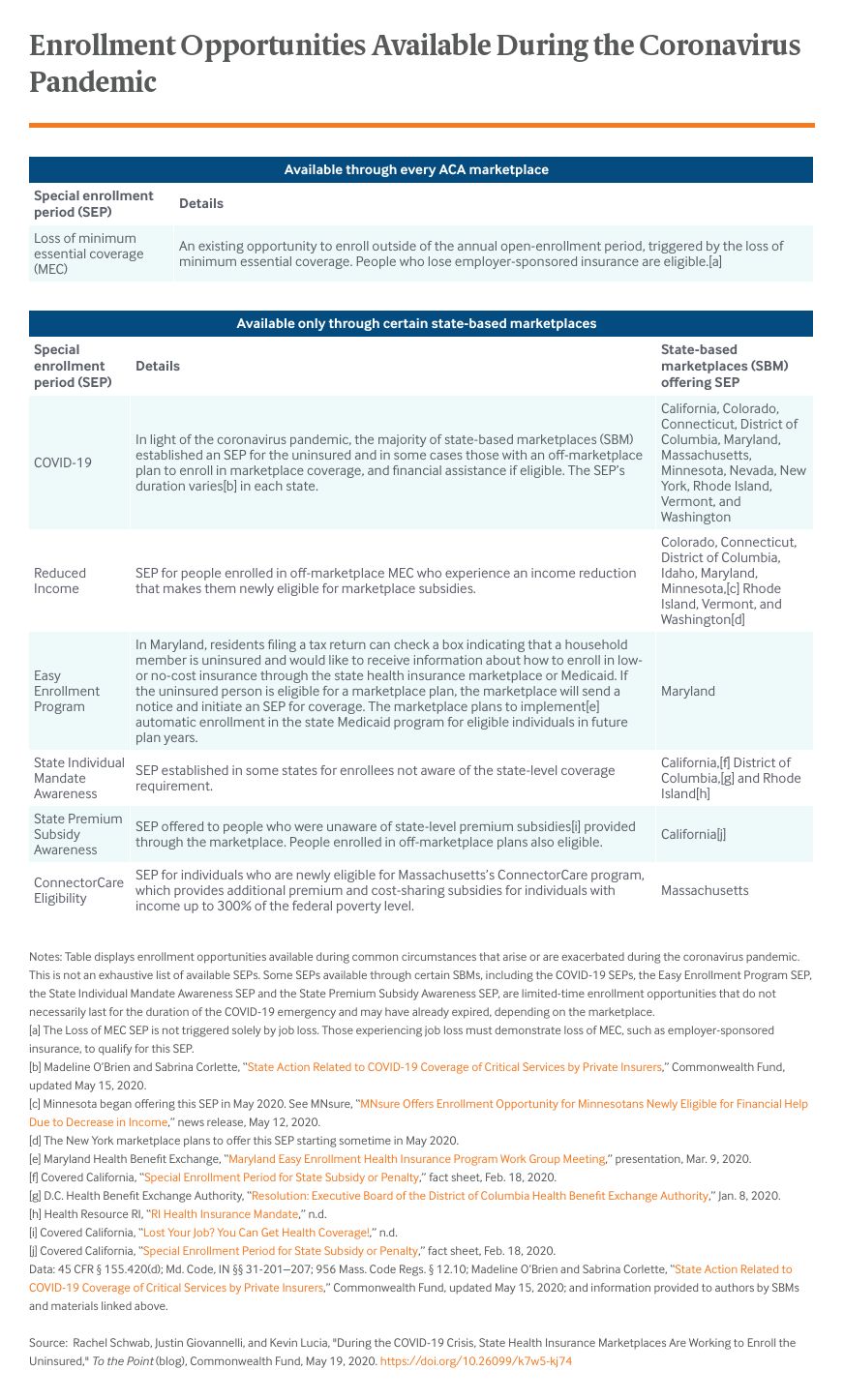

The coronavirus pandemic struck shortly after the end of the ACA’s annual open-enrollment period, the only time of year when people can sign up for marketplace coverage barring certain life events, such as losing employer coverage or other minimum essential coverage (MEC), which prompt a special enrollment period (SEP) in every state. There are several SEPs for people seeking coverage during the coronavirus pandemic, but some have been available only in certain states.

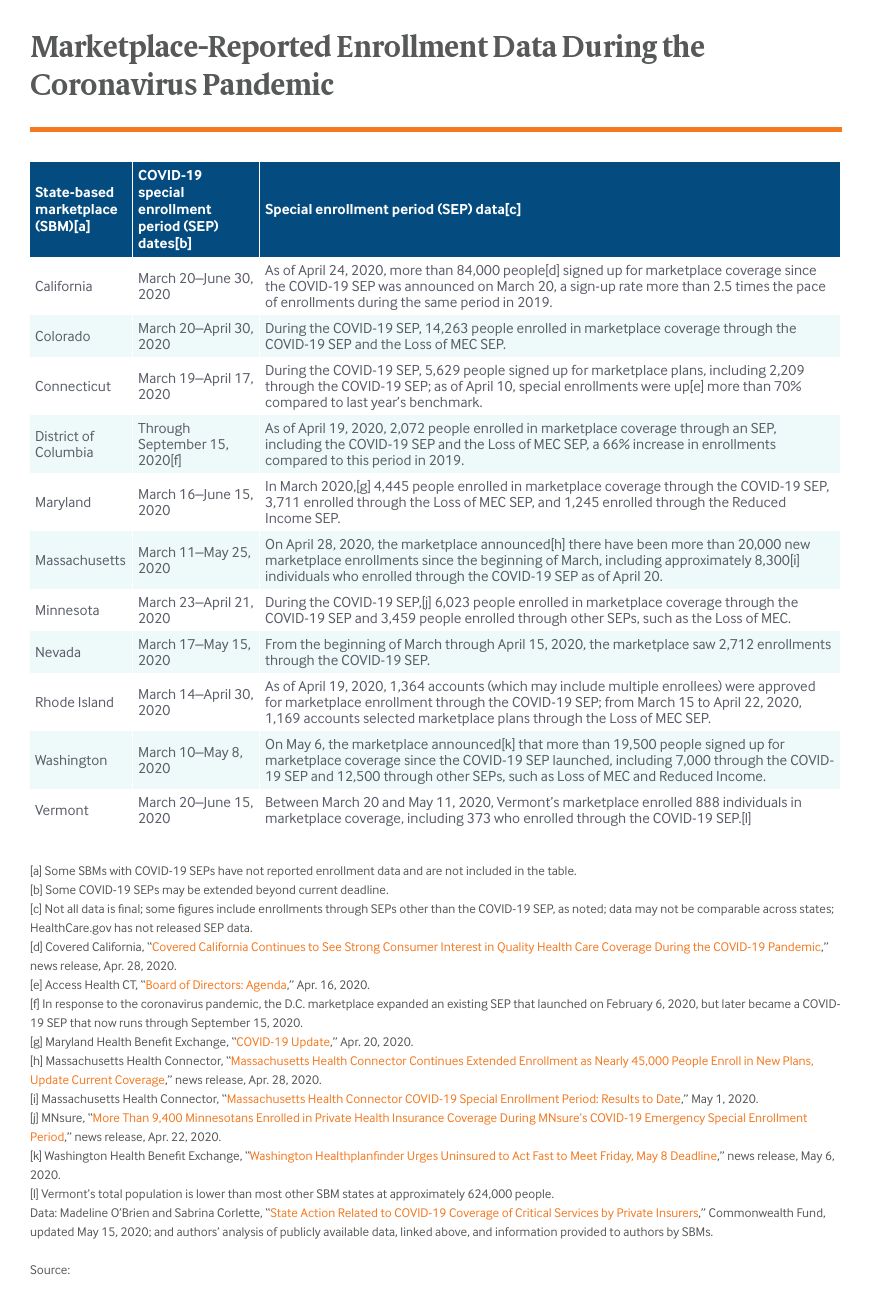

Given the need for access to health care and financial protection during the pandemic, 12 of the 13 SBMs — all but Idaho’s marketplace — established a new COVID-19 SEP, allowing the uninsured to sign up for coverage outside the annual enrollment period. The federal government declined to provide a similar SEP for states relying on the federal marketplace platform, HealthCare.gov, thereby limiting enrollment opportunities in 38 states.

Additionally, some SBMs offer a reduced-income SEP year-round for people enrolled in MEC outside the marketplace. This includes people who bought private individual coverage directly from an insurer and who become newly eligible for marketplace subsidies because of an income reduction. This SEP has not been implemented on HealthCare.gov, although in every state, marketplace enrollees with an income change can adjust or start receiving subsidies if they qualify based on eligibility standards.

Some SBMs also have offered SEPs specific to their state that allow the uninsured to sign up for coverage.