Short-term health plans were originally intended as a temporary lower-cost option for people who need catastrophic coverage during times of transition. Citing the need for a more affordable option in the individual marketplace, the Trump administration pushed to extend the contract terms on short-term health plans so they could be purchased as a substitute for year-long coverage. In a 2018 rule, short-term health plan coverage was lengthened from three months to just under 12 months. These plans are also now renewable for up to 36 months.

While short-term health plans typically have lower premiums than insurance options that comply with the Affordable Care Act (ACA), they have numerous shortcomings. As we highlighted in a previous blog, these plans often lack protections for people with preexisting conditions, allowing carriers to deny claims and rescind coverage. In addition, short-term plans usually come with high out-of-pocket costs and often do not cover all essential benefits, such as maternity care, required by the ACA. Short-term plans are routinely sold through misleading marketing practices and complicated association schemes, making it difficult for state regulators to enforce laws. These findings are supported by a recent report from the U.S. House of Representatives’ Committee on Energy and Commerce that concluded short-term health plans pose a threat to the “health and financial well-being of American families.”

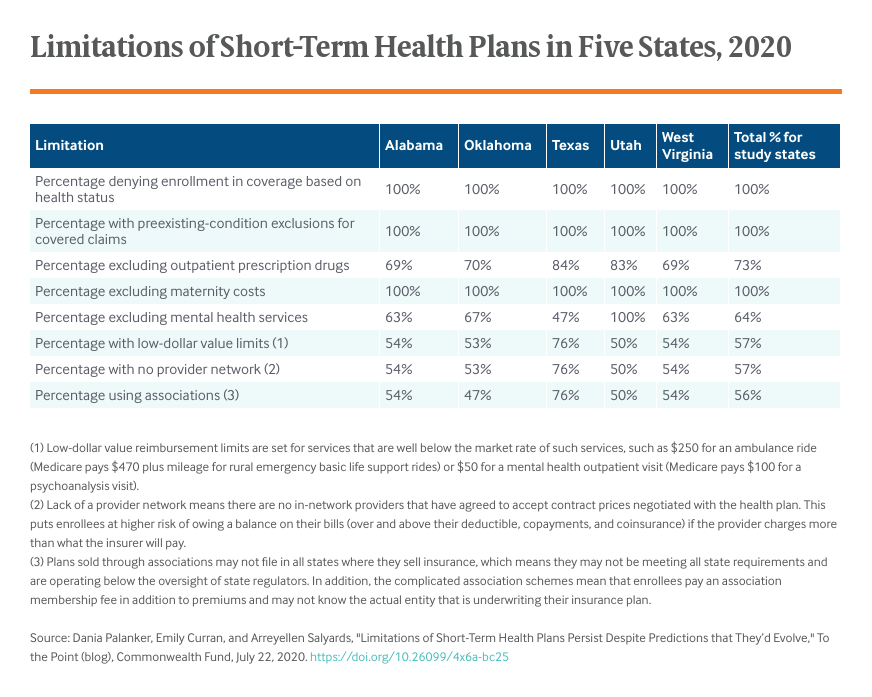

However, a 2019 analysis by the Congressional Budget Office (CBO) projected that the industry would evolve and a new type of short-term health plan would likely become available that offers more comprehensive coverage, including protections against high cost-sharing and catastrophic medical costs. It was expected the industry would offer new plans that could compete with individual market plans. To determine if this projection has come true, we looked at 414 plans with 12-month contracts sold on the online health broker website eHealth in Alabama, Oklahoma, Texas, Utah, and West Virginia. As part of our analysis, we looked at filings the plans made to regulators since the 2018 regulations were issued.

Our review found that most of these products have not increased catastrophic coverage or become more comprehensive.