Throughout the Affordable Care Act’s (ACA) history, analysts have debated whether making enrollment easier in the individual market will result in adverse selection. Adverse selection refers to people waiting to enroll until they expect to need health insurance. Doing so can drive up costs and premiums for everyone. Therefore, one key reason the ACA limits annual open enrollment to just several weeks is to encourage healthier people to enroll before they need care — to protect against future mishaps.

However, during the course of a year, work or family circumstances can change in ways that unexpectedly affect health insurance coverage. A person covered by group insurance at the start of the year might lose that coverage midyear and want to purchase individual coverage. To address such situations, the ACA allows for special-enrollment periods throughout the year for defined changes in work and family circumstances.

While insurers believe that special enrollment inherently leads to some degree of adverse selection, some experts disagree. Certain analysts believe that shorter open-enrollment periods will reduce the degree of strategic calculation people make; others note that sicker people will be the most diligent about enrollment. Consequently, extending open enrollment will likely bring in more healthy enrollees. Also, professionals who assist people with the special-enrollment process have noted that the cumbersome documentation requirements discourage people with less need for insurance from completing the process.

The COVID-19 pandemic provided an opportunity to put these competing arguments to a test. In the spring of 2020, realizing that millions of uninsured people would likely become desperately ill, a dozen states that operate their own marketplace exchanges chose to extend special-enrollment privileges to anyone without health insurance. These states also eased documentation requirements. As a result, they saw enrollment increase by almost 4 percent, compared to a 2 percent increase in states that kept standard enrollment rules.

For 2021, the federal government mitigated this difference by extending COVID special-enrollment rules to all states that use the federal exchange. In 2022, state and federal exchanges reverted to prepandemic enrollment rules, for the most part. Although the initial divergence among states was limited to just one year, that experience provides a valuable “natural experiment” that can inform enrollment policy going forward — in the event of other unexpected health disasters or in establishing or modifying routine enrollment policies in normal times.

As in a similar study, we use marketwide risk scores to gauge whether substantially expanding enrollment opportunities outside of normal open enrollment caused or mitigated adverse selection. The federal government uses risk scores to calculate the relative medical costs expected for populations in each state enrolled in ACA coverage. Changes in risk scores indicate whether enrollees are becoming more or less likely to incur medical expenses.

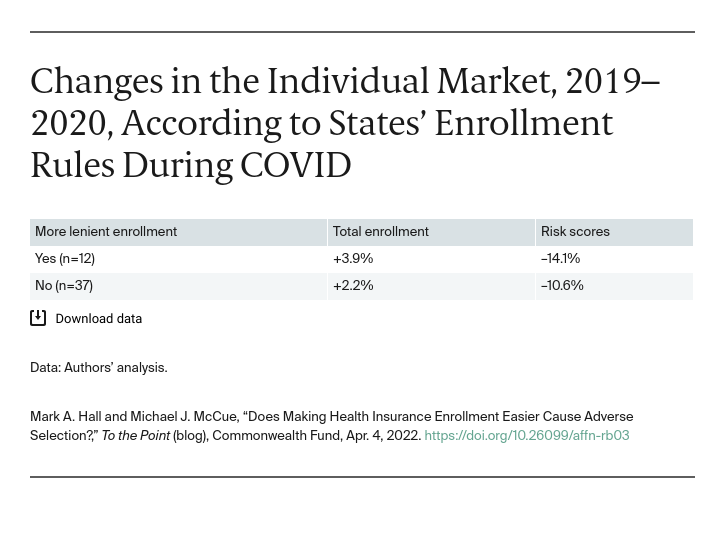

The following table shows how the overall risk score changed from 2019 to 2020, in the dozen states that reopened enrollment in the middle of 2020, compared with states that did not. Risk scores dropped in both sets of states, likely because of increased eligibility for special enrollment due to job losses fueled by COVID. Lower risk scores indicate that medical costs, and premiums, were likely to be lower. Notably, this improvement was almost twice as great in states that reopened enrollment regardless of hardship status. Thus, consistent with other studies using more limited data, we see that more lenient enrollment did not result in adverse selection. In fact, it led to favorable selection, meaning that these states saw almost double the improvement in their risk pools.

Factors other than enrollment rules also could account for this difference. California, for instance, provided enhanced subsidies during 2020, which undoubtedly boosted enrollment. Moreover, the more lenient states have all expanded Medicaid and run their own marketplace exchanges, which devote more resources to outreach, marketing, and enrollment assistance than the federal exchange does. Most of those factors were already present, however, before COVID and by themselves are unlikely to fully explain an improvement in risk scores. It is likely that these states’ enrollment polices attracted healthier members.

Our country undoubtedly will face unexpected health crises in the future. This experience indicates that policymakers should not hesitate to make health insurance enrollment easily available. Even without a crisis, this experience suggests that substantially expanded enrollment is likely to improve, not worsen, the risk pool. When people are given the opportunity to enroll in comprehensive subsidized health insurance, they value it not only for coverage of existing conditions but also the ability to protect against unknown future needs.