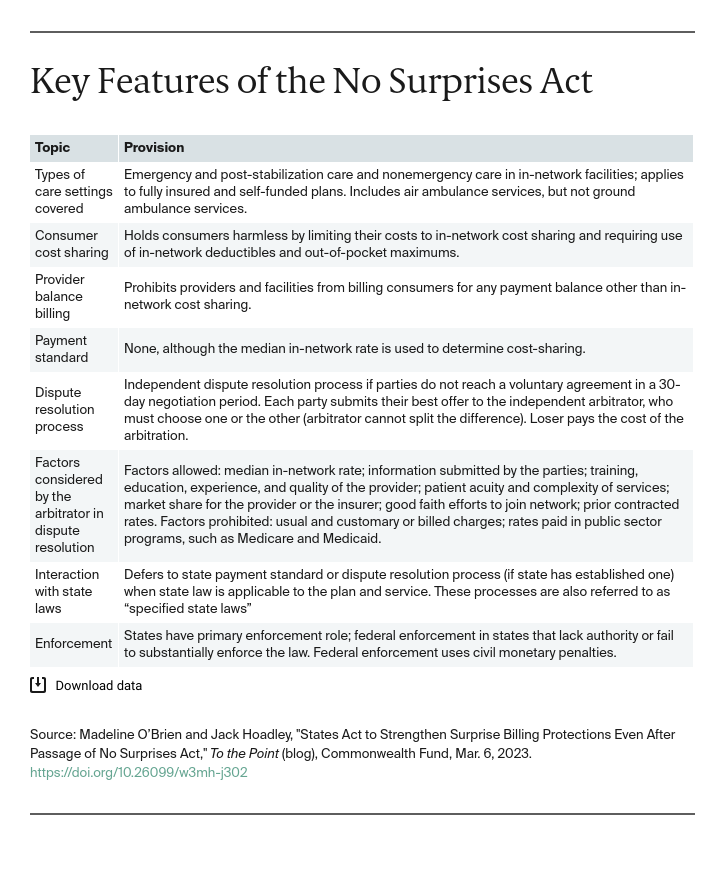

The No Surprises Act (NSA) establishes federal prohibitions against certain surprise medical bills. This may happen, for instance, when patients receive emergency care from an out-of-network provider or facility or from an out-of-network provider at an in-network facility. Prior to the NSA, insurers could refuse to pay these higher out-of-network charges and providers would frequently pass the balance of the bill on to the consumer.

Patients are now protected from these “balance bills,” but states play an important role in making these consumer protections a reality. States may choose to build on the NSA to improve consumer protections, define state enforcement authority, and outline the payment mechanism between providers and insurers. In this post, we discuss surprise-billing laws that states enacted in response to the NSA, as well as future opportunities for states to protect consumers from surprise bills.

State and Federal Roles Under the No Surprises Act

Under the No Surprises Act, states and the federal government work together to enforce consumer protection in three key areas:

- Balance billing protections. Prior to passage of the NSA, 33 states had enacted laws to protect consumers in fully insured health plans from balance billing.1The NSA is generally broader in scope than most of these laws and sets a minimum floor of protections. However, in places where state law is more consumer-protective, the state law remains in effect.

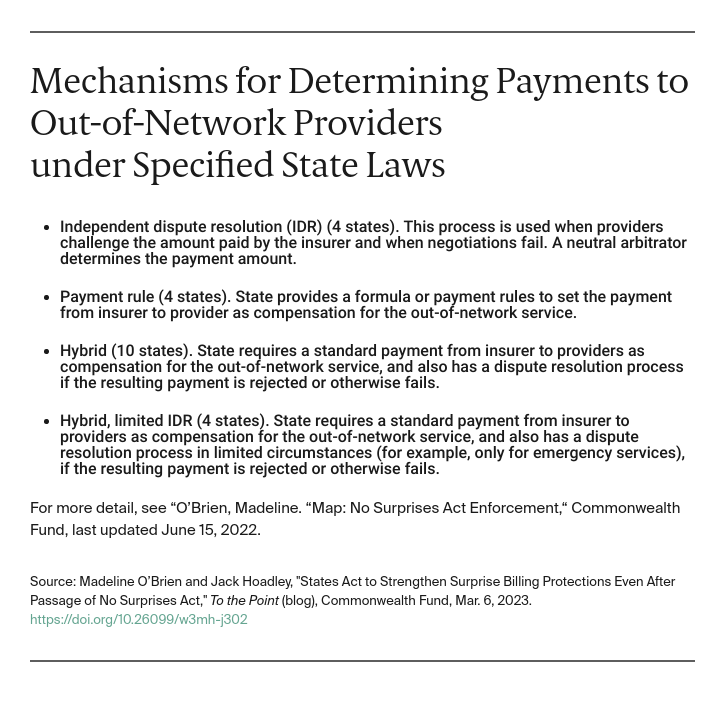

- Arbitration and dispute resolution. The NSA allows states to specify how payment disputes between insurers and providers are resolved. The NSA’s system for resolving such disputes is a combination of negotiations and an independent dispute resolution (IDR) or arbitration process for determining payments to out-of-network providers when negotiations fail. However, the federal approach does not apply if a state specifies its own mechanism (known as a “specified state law”). To date, 22 states have specified state laws that govern NSA dispute resolution.

- Enforcement. Lastly, states may develop their own processes for enforcing the NSA and specified state laws. The NSA intended for states to be the primary enforcers of the federal law, with the Centers for Medicare and Medicaid Services (CMS) stepping in as needed. Some states have reported legislative and administrative roadblocks to implementing full enforcement authority; guidance from CMS suggests that the federal government will be playing a large role in NSA enforcement in the short term.

State Legislative Action to Protect Consumers

Surprise billing legislation passed in 2021-2022 shows additional ways states may improve protections for consumers.

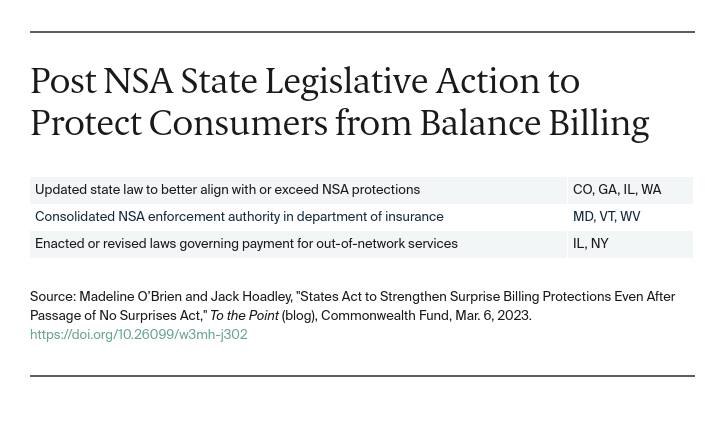

Building on Federal Protections

Several states have updated their laws to align better with NSA protections. Doing so can reduce confusion and simplify procedures. Washington enacted legislation that expands protections to medical specialties not previously covered (e.g., behavioral health providers) and to coverage of post-stabilization services — that is, services that occur following an emergency visit after a patient has been stabilized. Washington includes post-stabilization services under the scope of emergency services. They are also generally considered covered emergency services under the NSA as long as certain requirements are met. In Colorado and Illinois, legislators extended surprise billing protections to cover radiology and laboratory services, which are within the scope of ancillary services under the NSA but were not previously protected under state law. Illinois’s legislation also adopts the NSA’s definition of a qualifying payment amount2 (QPA) for the purpose of determining patient cost-sharing for out-of-network services. In addition, Washington and Georgia have expanded state laws to protect patients from surprise bills for mental health emergencies that are not treated in hospitals. Washington issued guidance defining emergency services as including behavioral health crisis centers, and CMS later confirmed that the NSA’s definition of “emergency services” includes these types of facilities, as well as any type of facility licensed by a state to provide emergency care.

Enforcement Authority

States have acted to consolidate enforcement authority for NSA provisions in their insurance departments to promote more efficient oversight. West Virginia and Maryland passed laws giving their insurance commissioners authority to enforce the NSA. Similarly, Vermont’s law directs the Department of Financial Regulation to enforce the NSA, as it applies to insurers and providers, and gives the department authority to refer noncompliance to state or federal agencies.

Strengthening Arbitration through Specified State Laws

The NSA allows but does not require states to specify how payment disputes between insurers and providers are resolved. The state laws governing these procedures are known as specified state laws, and states have taken action to adjust these laws and modify how surprise billing disputes are settled. New York’s most recent budget bill updated the state’s dispute resolution process by adding a median charge for in-network services to the list of factors that can guide arbitrator decision-making. This action may help address the potential inflationary effect of New York’s prior IDR process, which allowed billed charges to be considered. Data from New York suggests that the consideration of billed charges, which are unilaterally set by providers, can result in higher final payments, which can translate into higher costs and higher premiums for consumers down the line.

Legislation enacted in Illinois revised that state’s payment-dispute process. The updated process allows either party to request binding arbitration following a 30-day negotiation period. The law also modifies the way that arbitrators may consider the factors they use during the process.

Looking Forward

States have continued to innovate to develop ways to protect consumers from surprise medical bills, even after the enactment of the NSA. In 2021-2022, states have acted to build on federal protections, increase state enforcement authority, and reform specified state laws. In enacting or revising laws governing the payment mechanism for surprise bills, states need to be cautious of embracing an inflationary approach that may raise costs for consumers. States further protect consumers by closely monitoring compliance by insurers and providers and consumer complaints related to balance billing.