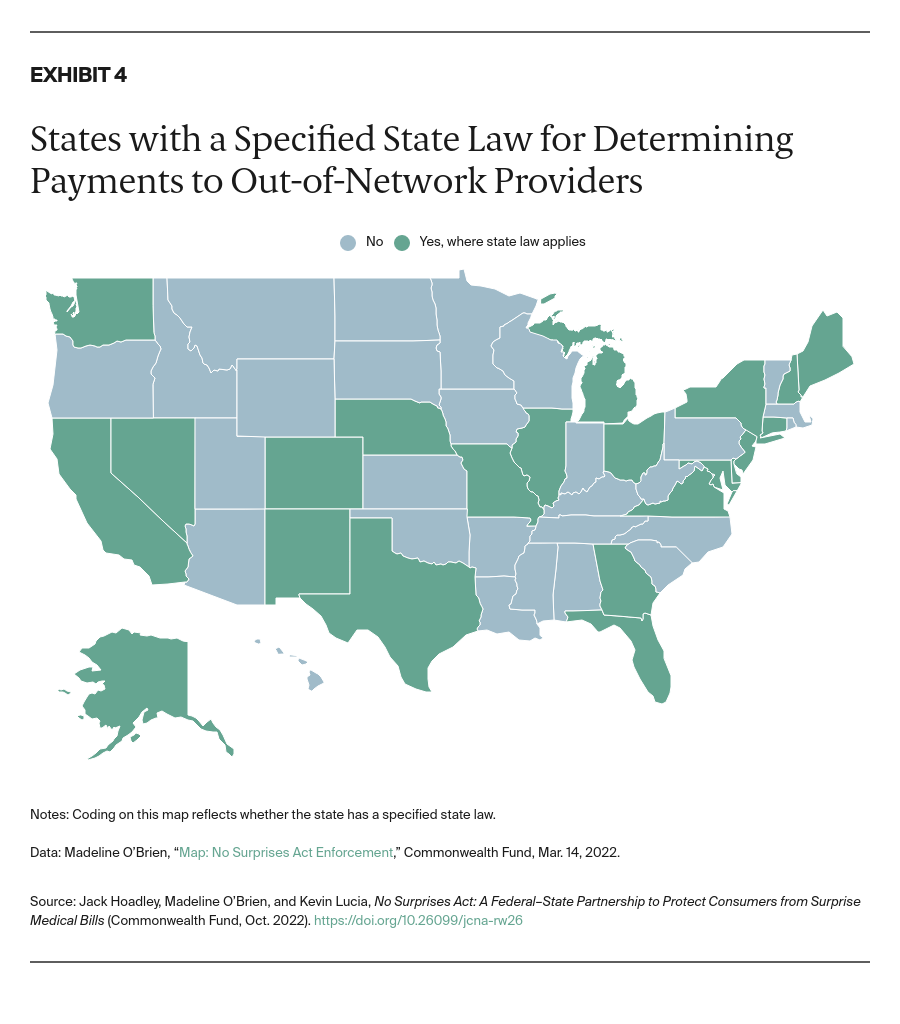

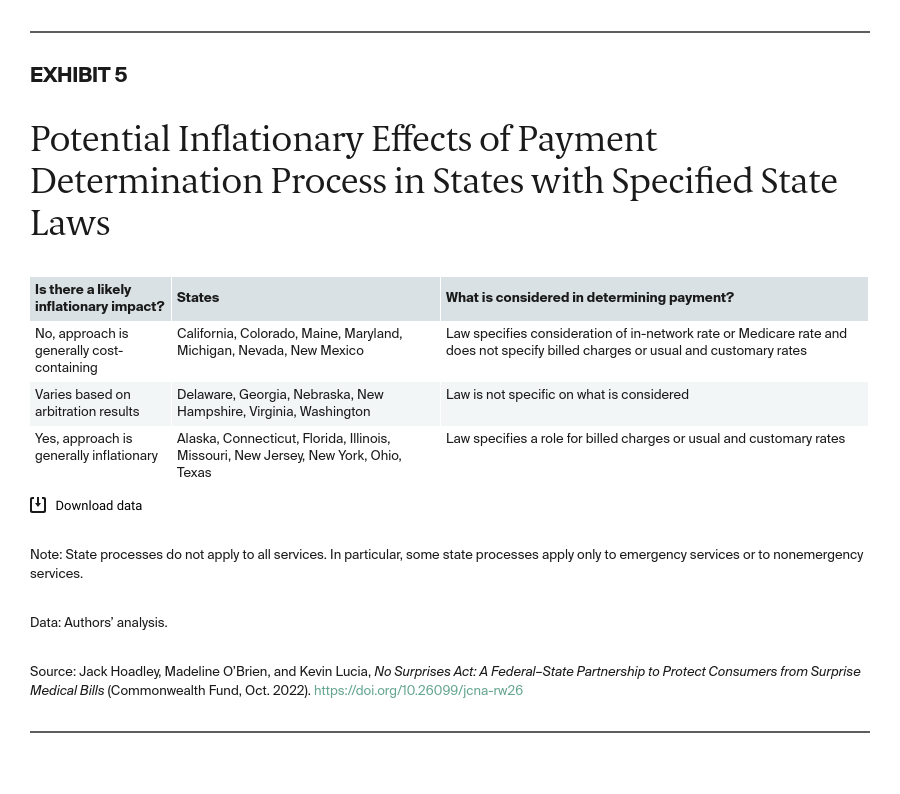

Three state arbitration systems (New Jersey, New York, and Texas) allow consideration of billed charges or usual and customary charges. As a result, these standards are friendlier to health care providers than to insurers and could lead to higher payments for providers.14 In 2022, New York added median in-network charges as another factor that can be considered in arbitration, a move that should provide greater balance between consideration of billed charges and in-network rates going forward. According to one study, median awards by New Jersey arbitrators on average were 5.7 times median in-network prices and often much higher.15 Similarly, Alaska, Connecticut, and Ohio have payment standards that rely in part on charges, which could lead to higher awards.16

Some state systems promote cost containment.

By contrast, the rate standards or arbitration factors used by at least seven states may not promote higher payments and may even bring payments down. California sets payment for nonemergency, out-of-network services at the greater of 125 percent of the Medicare rate (an approach that is not allowed in the federal system) or the health plan’s average contracted rate. Colorado’s standard for providers (not facilities) is the greater of the 60th percentile of in-network rates across insurers or 110 percent of the insurer’s in-network rate. Maine sets payments using the insurer’s in-network rate and directs arbitrators to consider the in-network rate in their decisions, thus limiting the potential for inflationary awards.

Other state systems are more open ended.

In other states, arbitrators have considerable discretion. Virginia and Washington require payments at commercially reasonable rates determined by insurers, which are likely to be close to in-network rates. Georgia requires payments at in-network rates. If these payments are challenged in the state IDR system, the laws do not direct arbitrators toward or away from billed charges. Few arbitration cases have been filed in Washington, even though some insurers report offering payments slightly below median in-network rates.17

While the No Surprises Act expands consumer protections in many states, some state laws offer even greater protections.

The No Surprises Act allows certain providers to ask patients in advance to waive protections from surprise medical bills by signing a consent waiver under strict limitations that disallow requests at the time of service and forbid requests for emergency services or for ancillary services surrounding a nonemergency service. Some states go further. In at least four states, no consent waivers are allowed. Several other states require more advanced notice than under federal rules.

Some state laws go beyond the No Surprises Act to include protections for a greater scope of services. For example, protection for ground ambulance services was omitted from the federal law, in part because of uncertainty over how to handle ambulance services operated by cities, counties, and other public authorities. However, 10 states offer some protections for consumers when they use ground ambulance services.18

As in the federal law, most states limit protections for nonemergency services to those delivered in facilities. The No Surprises Act defines facilities as inpatient hospitals, critical access hospitals, hospital outpatient departments, and ambulatory surgery centers. In rulemaking, federal officials have requested public comments on defining facilities more broadly. Some state statutes also include skilled nursing facilities, infusion centers, and dialysis centers, among other sites, or include other services like diagnostic imaging or laboratory services. At least two state laws also extend surprise billing protections to services delivered in physician offices or other outpatient settings.

Federal and state officials appear to recognize that education is important to ensure effective protections.

It is important that consumers, insurers, and providers understand how the No Surprises Act affects them. In an ideal world, consumers would benefit from the new protections without direct action on their part. A provider would no longer send balance bills and limit bills to in-network cost sharing. But during the first year, both providers and insurers will be learning the rules and developing procedures for sharing information and billing correctly.

In addition to leveraging federal efforts, many states are taking additional steps to educate consumers on new protections.

Consumers should be aware of their options if they receive a bill they believe is incorrect. The first step should be to review insurers’ explanations of benefits to determine whether a bill results from something like not having met a deductible. If the bill qualifies as a surprise medical bill, consumers should contact their insurer and provider to ask for a corrected bill.

If this step fails, consumers should file complaints. There is no monitoring system where the federal government or state governments track provider bills, and insurers cannot see from claims whether balance bills are sent. Consumer complaints are therefore an essential component of enforcement. The federal government has published resources online for people to learn about their rights and has a portal for submitting complaints.19

Many states also are acting to educate consumers and other stakeholders. In Idaho, Indiana, New York, Oklahoma, West Virginia, Wisconsin, and other states, websites provide basic information on consumer protections as well as links to federal resources.20 Some states also are creating portals and phone lines to take in complaints. Pennsylvania’s online resource page includes a “no surprises bill review request form.”21

One challenge for states is ensuring that information is available when a potential surprise bill is received. Pennsylvania is developing a brochure, conducting social media outreach, and leveraging the governor’s office to help.22 The Montana insurance commissioner issued a statement to publicize the state’s efforts.23 Other states are primarily directing consumers to federal resources. Some states are ensuring that relevant phone numbers and websites are available on the explanation of benefits statements consumers receive from insurers after receiving a health care service. In addition, Colorado, New York, and Texas, among other states, require that insurance identification cards specify whether the insurance is state-regulated or falls under federal ERISA rules. Making this information readily available can help consumers and providers know which government has jurisdiction.

Insurers and providers need to understand their responsibilities.

Even more important is the education of insurers and providers, since they are responsible for ensuring that consumers are notified of their rights and protections and correctly billed when receiving services from out-of-network providers. The transfer of information for out-of-network claims requires new avenues of communication between providers and insurers moving in both directions.

Providers and insurers also need to understand the steps involved in billing disputes, including whether state or federal IDR processes apply. When negotiations and IDR are invoked, participants are required to exchange information about the applicable qualifying payment amount, amounts to be paid, and documentation of factors IDR entities may use in making a payment determination.

There are new federal resources for medical providers and insurers, including a U.S. Department of Health and Human Services website that informs providers where they can submit complaints or get information about the new requirements.24 A separate webpage provides information on the federal IDR process.25 In addition, the U.S. Department of Labor has a webpage for self-funded group health plans.26

Discussion and Policy Implications

Implementation of the No Surprises Act has been a substantial undertaking, requiring federal agencies to develop a complex regulatory framework and facilitate its adoption, all in a short time span. Simultaneously, states have compared their own surprise billing laws to the federal law to understand interactions. Many states have launched websites and educational outreach to ready citizens and stakeholders for a smooth and effective implementation.

Enforcement is a particular challenge. Consumer complaints are critical for identifying compliance issues because there is no systematic way for government agencies to track incorrect bills. The federal government will receive complaints through a federal portal and phone line. In the spirit of this “no wrong door” policy, complaints also may be received by state insurance departments. Ideally, complaints will be routed quickly and efficiently to whatever state or federal agency can best investigate and address them. Many believe that informal contacts to a noncompliant insurer or provider will resolve most complaints.

It will be important to monitor these efforts to learn how well and how quickly complaints are resolved and how often they must be elevated to a more formal enforcement process. For example, the U.S. Department of Labor lacks a track record for effective oversight of self-funded plans.27 And many states lack any history for enforcing requirements on facilities and providers with regard to billing issues.

Inevitably, enforcement processes will evolve. The law anticipates that states have the primary enforcement role, but initially most will partner with federal agencies or rely entirely on federal enforcement. Some states may enact laws to give their agencies clearer enforcement authority, allowing them to take on a larger role in the future. Similarly, collaborative enforcement agreements between federal and state agencies may evolve as experience demonstrates how enforcement works best.

Over time, state policymakers will debate changes to their existing surprise billing laws. Some states may opt to align state protections more closely to the federal law to reduce confusion and simplify procedures. For example, New York enacted changes to update the state surprise billing law to align it with the No Surprises Act.28 Similarly, Washington enacted legislation to expand protections in state law to medical specialties not currently covered, modify their handling of poststabilization services, and make other adjustments.29

Some states also may consider filling gaps in the federal law’s protections. States may also consider expanding protections for services provided by ground ambulances or in facilities other than hospitals and ambulatory surgery centers. Furthermore, Congress may decide to expand on the law in areas such as ground ambulance services, and there are some potential areas where the federal agencies have authority to expand the law.

One unanswered question in the law’s implementation is the final resolution of lawsuits filed by provider organizations challenging the rules for how the qualifying payment amount should be considered in IDR determinations.30 The final rule, released in August 2022, addressed issues raised in the litigation.31 Some litigation remains active, and further changes could curtail the cost-containment goals that were important to congressional sponsors of the No Surprises Act.

Even after litigation is resolved, other battles over payment determination may arise in state legislatures. Providers may push for state payment determination processes that are more favorable to them. Alternatively, advocates for cost containment may push for systems like those in California and Maryland that may reduce costs.

The long-term success of the law also will rely on oversight from state and federal agencies, both to monitor the law’s efficient operation and to identify any adverse consequences. The No Surprises Act calls for various studies of its impact on provider networks, health costs, provider concentration, and the role of private equity. Some states already report on the impact of their state laws on both costs and the prevalence of out-of-network claims. A focus on these issues by government agencies and researchers will be critical to identifying adverse effects and opportunities for adjustments.