In 2025, enrollment in the Affordable Care Act (ACA) marketplaces rose to an all-time high of 24 million. This was double the enrollment figure from four years prior, with the increase largely due to Congress enhancing the generosity of the ACA’s premium tax credits in 2021. In addition to lowering premiums and boosting enrollment, the enhanced tax credits also prompted many people to shift to higher-value health plans that reduced their out-of-pocket costs. These coverage gains are now eroding.

Congress failed to extend the enhanced credits at the end of 2025 and, earlier in the year, enacted a tax-and-spending law that further reduced federal spending on marketplace coverage and imposed new paperwork burdens. Sign-ups declined during 2026 enrollment, but to understand the impact of federal policy changes, it’s important to assess what people did after open enrollment ended. Those emerging data point to even more dramatic drop-offs.

Only Part of the Story

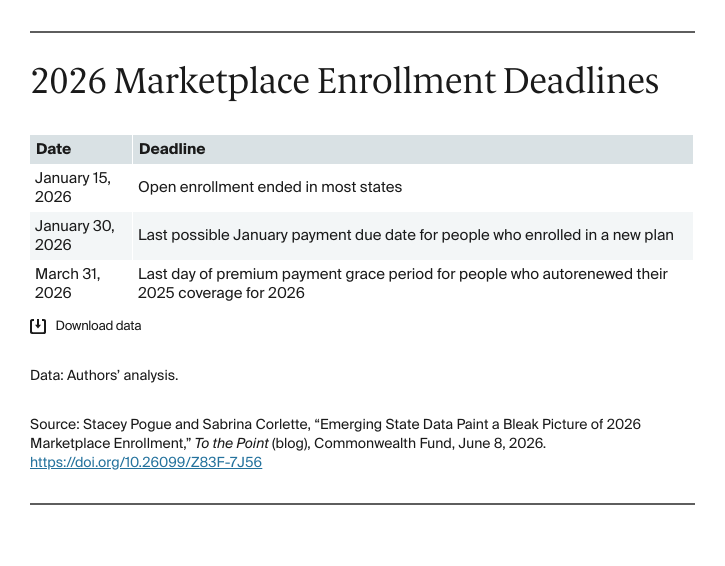

The complete picture will roll out in phases. Federal regulators have so far released data on initial sign-ups during open enrollment, which include people whose coverage was automatically renewed at the end of 2025. However, enrollment is not complete until the first month’s premium is paid. Unprecedented net premium hikes in 2026 have prompted some people who signed up for coverage to drop it — either by canceling their policy or simply not paying their premium. Federal regulators are not expected to release the first snapshot of nationwide paid enrollment data until this summer.

This year, sign-ups during open enrollment fell by 1.2 million, a 5 percent drop from the prior year, the largest decline in any year since the marketplaces opened in 2014. Sign-ups dropped in 41 states, declining by 1 percent to 22 percent. Sign-ups increased in the remaining nine states and the District of Columbia, reflecting state efforts to blunt enrollment losses.

People Signing Up but Dropping Coverage

Several state-based marketplaces have released early data indicating that plan cancellations rose sharply between January and March this year — up 24 percent over last year.

California’s marketplace examined who is canceling, which sheds light on why they are dropping coverage. Middle-income consumers who lost financial help when the enhanced premium tax credits expired and Black consumers canceled at rates twice as high as last year. In contrast, the lowest-income enrollees, shielded from rate hikes by state-funded subsidies, were the only group less likely to drop coverage compared to last year, with no racial or ethnic disparities. This suggests that affordability concerns are driving cancellations.

Enrollment Slides When Premiums Are Due

Experts estimate that 14 percent of people who signed up for a 2026 plan did not, or could not, pay their January premium. Some saw their coverage terminated quickly for nonpayment, but renewing consumers who qualify for tax credits generally get a three-month grace period before termination.

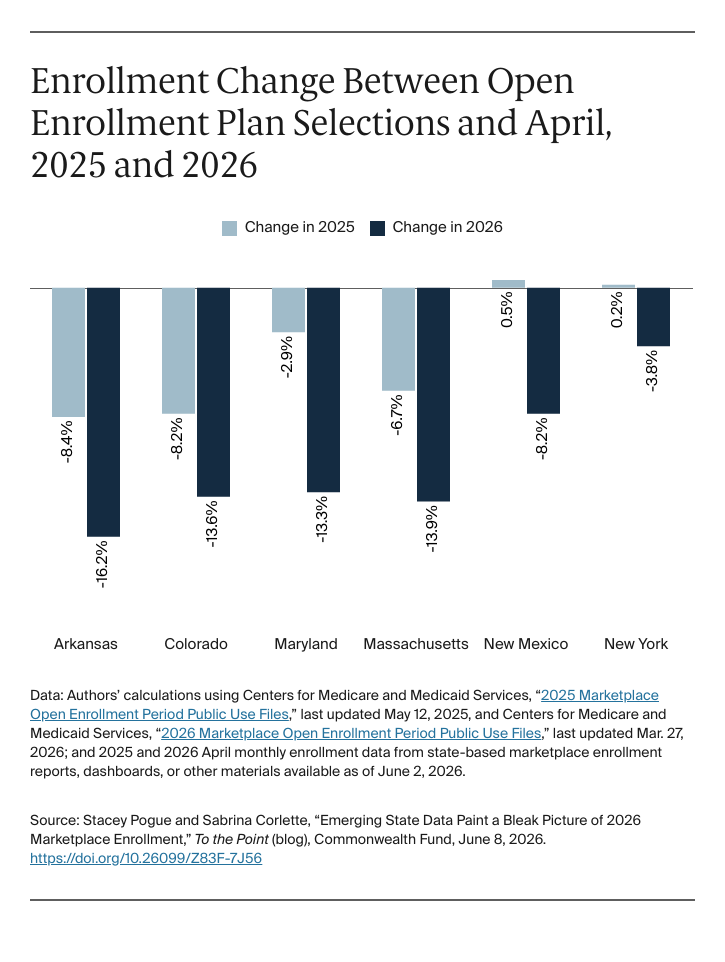

A handful of state marketplaces have released monthly enrollment data through April 2026, which provides more information about enrollment after the expiration of initial grace periods. These marketplaces all show a drop-off between initial sign-ups, including autorenewals, and April. While a drop-off in this period is not unexpected, the magnitude of the decrease compared to last year is stark. For example, Maryland saw a 3 percent drop-off between open enrollment and April last year, compared to 13 percent this year.

This is a small sample of states, but these early indicators may not bode well for national outcomes. These states invest their own funds to boost subsidies or otherwise take steps to make marketplace coverage more affordable, while most states do not.