Option 2: Reducing the Employer Affordability Threshold. This policy would improve access to marketplace coverage by lowering the threshold above which employer coverage is deemed unaffordable. Currently, the employee affordability threshold is 9.61 percent of income. Under this proposal, people whose premiums for employer coverage exceed 8.5 percent of income would be considered to have unaffordable coverage and could enroll in a marketplace plan.2

Option 3: Adding a $10 Billion Reinsurance Fund. This policy would fund reinsurance to pick up the cost of medical expenditures above a certain threshold, thus reducing risk for insurers and making nongroup insurance more affordable for people in all states who are ineligible for subsidies. Some states already provide reinsurance in partnership with the federal government under “innovation waivers” that allow them to modify parts of the ACA.3

Option 4: Increasing the Federal Medicaid Matching Rate in Expansion States. This policy would increase the federal Medicaid matching rate for the expansion population to 100 percent. Under the policy of filling the coverage gap (Option 1), the federal government pays 93 percent of the costs of covering the Medicaid expansion population in expansion states, but all the costs for that population in nonexpansion states, thus creating inequitable funding between states.

Option 5: Enhancing and Funding Marketplace Cost-Sharing Subsidies. The final policy would increase and expand cost-sharing subsidies, also known as cost-sharing reductions (CSRs), for subsidized ACA plans for low-income people. This policy would increase CSRs and tie premium tax credits, currently tied to silver-tier marketplace plans, to gold-tier plans. CSRs under this reform would be fully federally funded, which would reduce marketplace premiums because insurers currently pay for the CSRs and cover their costs by raising premiums on benchmark silver-tier plans. Federal funding for the CSRs would eliminate this practice, known as “silver loading.”

We analyzed the individual and cumulative impact of these proposals on coverage and costs, starting from the baseline assumption of extended ARPA premium subsidies under the IRA.

Coverage and Cost Implications for Five Reform Options

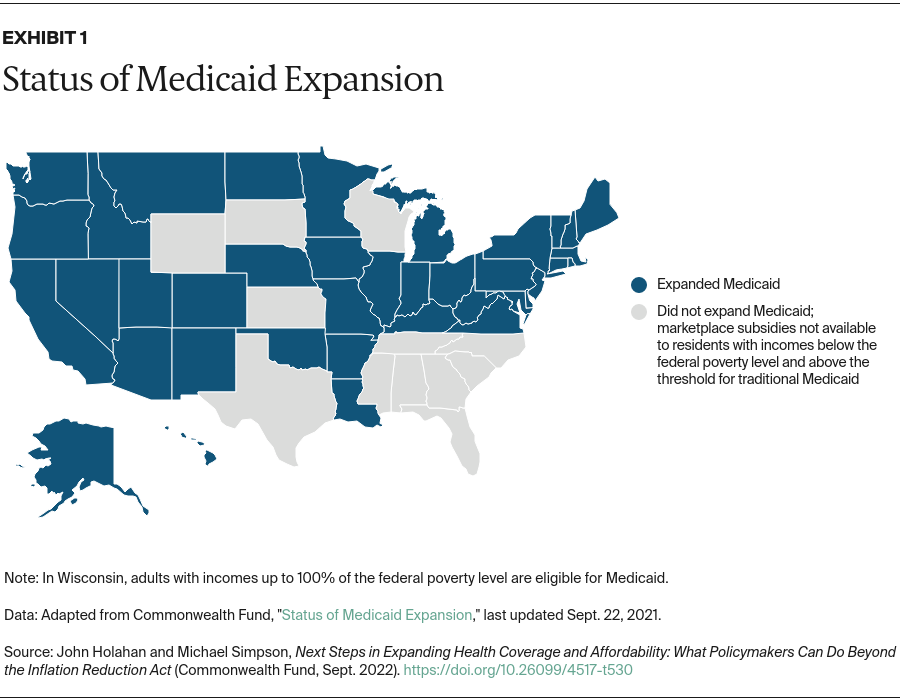

Option 1: Filling the Medicaid Gap in Nonexpansion States. The expansion of marketplace coverage would reduce the number of uninsured by 1.9 million in 2023 (Appendix Table 2). About 2.5 million additional people would receive marketplace subsidies.

The largest increases in the number of people covered under this reform would be among non-Hispanic whites, but non-Hispanic Black people would see the greatest percentage decrease in uninsurance. In the 12 nonexpansion states, uninsurance for non-Hispanic Black people would fall by 27 percent while reductions for other groups would range from 8 percent to 20 percent (data not shown; Appendix Table 3 presents uninsurance rates for all states in each option).

Filling the Medicaid gap in nonexpansion states would cost the federal government $27.0 billion in 2023, largely because of greater costs for marketplace subsidies. Households would save $5.2 billion because of access to subsidized coverage. Overall health spending would increase by $14.5 billion in 2023.

Option 2: Reducing the Employer Affordability Threshold. Lowering the employer affordability threshold to 8.5 percent would reduce the number of uninsured by 109,000 in 2023 (Appendix Table 4). Most people who would gain coverage would be those with incomes between 138 percent and 300 percent of poverty.

This policy would increase federal government spending by $2.4 billion in 2023, but some of this would be offset by $400 million in increased revenue because wages, which are taxable, would increase as employer health insurance premiums, which are generally not taxable, decrease. Households would see savings of $0.6 billion, and employers would spend $0.9 billion less on premiums because of lower levels of employer coverage.

Option 3: Adding a $10 Billion Reinsurance Fund. This policy would lower marketplace premiums and reduce the number of people uninsured by 198,000 in 2023 (Appendix Table 5).

Net federal government spending would increase by $1.1 billion in 2023. Because reinsurance would lower premiums, the federal cost of marketplace premium tax credits would fall by $7.5 billion, largely offsetting the $8.7 billion increase in spending for reinsurance.4 Households would see minor savings because premiums would fall for those with unsubsidized coverage, and a small number would leave employer insurance for less expensive nongroup plans. Because there would be fewer covered workers, employers would spend slightly less on premiums.

Option 4: Increasing the Federal Medicaid Matching Rate in Expansion States. This policy would shift about $7 billion in payments from states to the federal government but would not affect coverage nor increase overall spending on health nationwide in 2023 (Appendix Table 6).

Option 5: Enhancing and Funding Marketplace Cost-Sharing Subsidies. As seen in Appendix Table 7, the number of uninsured would fall by 1.5 million in 2023 under this policy. Employer coverage would drop by 810,000 as more people shift to marketplace plans. Two million more people would receive subsidies, and private nongroup coverage would increase by 2.3 million.

Federal government spending under this policy would be higher by $13.0 billion in 2023. Spending for cost-sharing subsidies would increase by $12.2 billion, but there would be only a small increase in federal funding of marketplace premium tax credits despite the new enrollment, because of the decline in premiums. Household spending would fall by $4.8 billion, while employer spending on premiums would drop by $4.5 billion.

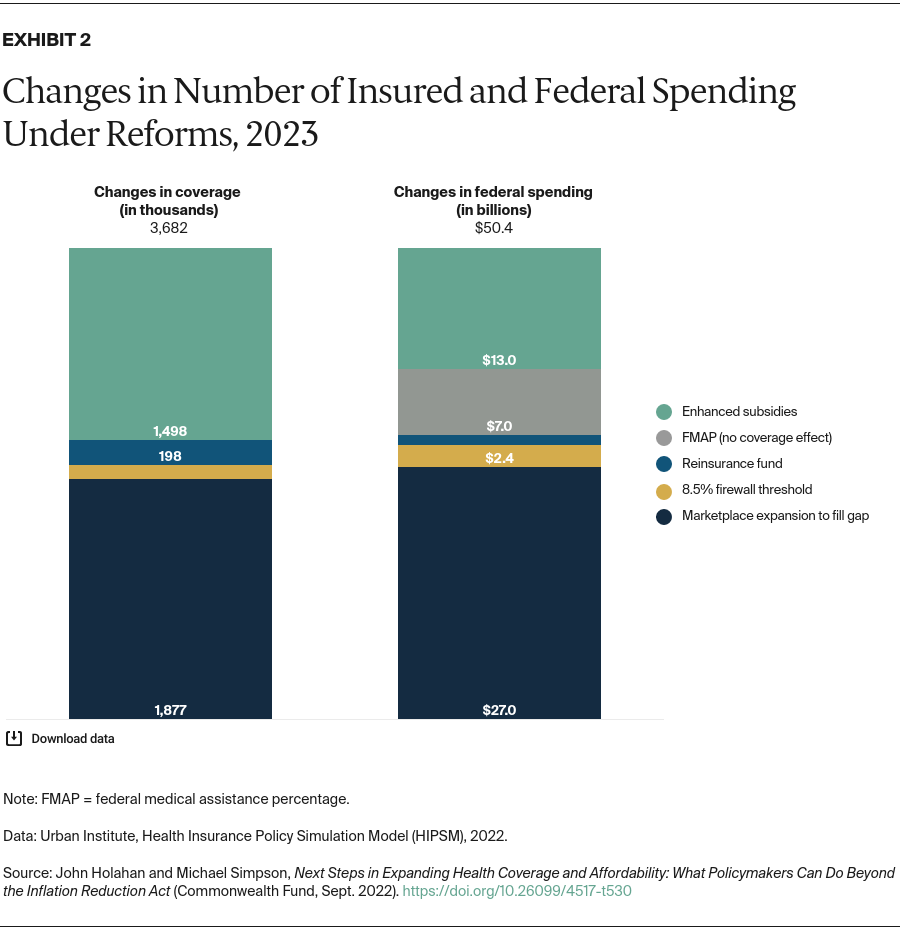

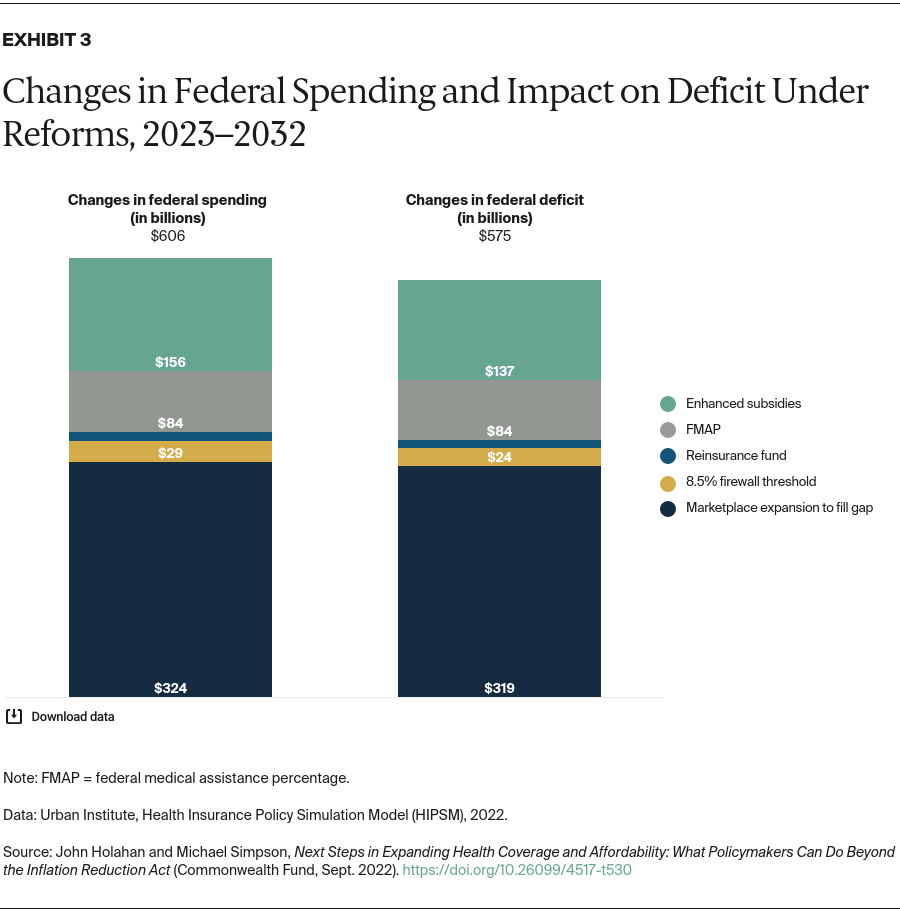

Cumulative Impact on Coverage and Spending for 2023

Exhibit 2 shows the change in coverage and spending for each incremental reform. Together, the five policies would provide coverage for 3.7 million more people in 2023. Filling the Medicaid gap and improving cost-sharing subsidies would have the greatest impact on coverage. These two policies would also have the most significant effect on federal spending. If all five policies were enacted, federal spending would increase by $50.4 billion in 2023.