Abstract

- Issue: Adults and children enrolled in Medicaid and the Children’s Health Insurance Program (CHIP) generally must renew their coverage every 12 months. For people who remain eligible for these programs or become eligible for marketplace premium tax credits (PTCs), it’s important to minimize coverage losses due to administrative issues.

- Goal: To estimate the number and characteristics of those still eligible for Medicaid/CHIP and those who become eligible for PTCs one year after enrolling and to estimate the impact of automatic enrollment of former Medicaid enrollees now eligible for PTCs.

- Methods: We enhanced our Health Insurance Policy Simulation Model with new analysis of longitudinal survey data.

- Key Findings and Conclusions: About 87 percent of Medicaid and CHIP enrollees are still eligible one year later. Among the groups most likely to still be eligible are people who enrolled with a near-$0 income, children in families with income below 100 percent of the federal poverty level, and single-parent families. About 2.5 million Medicaid/CHIP enrollees are eligible for PTCs one year later, and we estimate 1.3 million people would enroll in marketplace plans if left to individual responses. A nationwide automatic enrollment and effectuation program would increase enrollment to 1.8 million.

Introduction

People in Medicaid and the Children’s Health Insurance Program (CHIP) must generally renew their coverage 12 months after they enroll.1 People can be disenrolled for two main reasons. First, some lose eligibility due to increased income from job changes or other circumstances. Low-income working families often have a fluctuating income.2 Second, some people are procedurally disenrolled for reasons such as necessary forms not being received in time, even though some of them remain eligible.

Keeping eligible people enrolled is desirable, since disenrollment from Medicaid or CHIP can lead to losses of health coverage, which, even if temporary, can be a problem for beneficiaries and state Medicaid agencies. Research has shown that health coverage reduces mortality3 and improves financial stability.4 Disruptions in health coverage may result in delayed care and higher program costs for Medicaid and CHIP.5 Keeping children insured has been shown to have continuing benefits into adulthood.6

The challenge for state and federal policy is how to maximize renewals and prevent disruptions in coverage without lowering the accuracy of renewal, which could lead to larger numbers of ineligible people having their coverage extended. Two types of Medicaid policies designed to minimize disenrollment among those who remain eligible are 1) continuous eligibility and 2) automatic (ex parte) renewal through data matches. Starting in 2024, states were required to give children 12 months of continuous eligibility. In addition, a growing number of states have obtained waivers to extend continuous eligibility beyond this period for children and to extend it for adults as well. Automatic renewal strategies were important in many states during the Medicaid unwinding, when the federal government granted states temporary flexibilities to expand the scope of automatic renewals. There is interest in making some of these strategies permanent.

A third approach to the dual problem of minimizing coverage disruptions while maintaining enrollment accuracy is to target former Medicaid and CHIP enrollees who are found eligible for marketplace premium tax credits (PTCs) at their 12-month renewal for assistance with the transition to marketplace coverage. One study estimated that only about 3 percent of those losing Medicaid or CHIP coverage enrolled in the marketplaces.7 Some people eligible for PTCs do not enroll because either they do not know they are eligible or they consider the premiums and cost sharing of marketplace coverage unaffordable. The study also found that about 70 percent of those transitioning from Medicaid to marketplaces experienced a gap in health coverage.

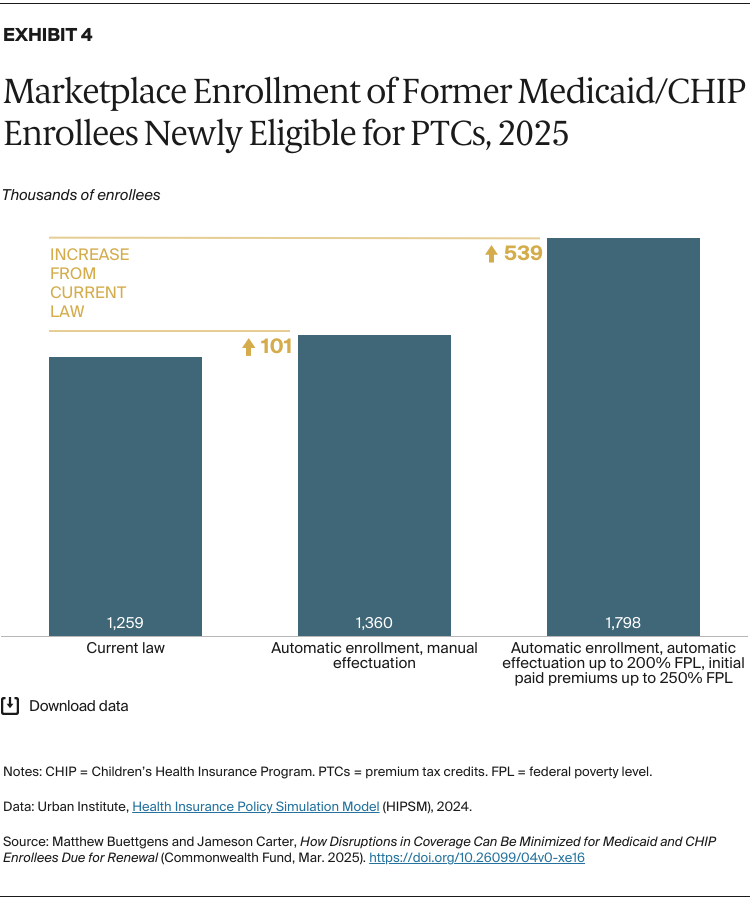

To address this problem, two states recently introduced automatic marketplace enrollment for former Medicaid enrollees. In California, Medicaid and CHIP enrollees who become eligible for PTCs are automatically enrolled in the marketplace under a plan selected for them, but each person must manually complete (or “effectuate”) their enrollment by paying the first month’s premium. Rhode Island goes further, automatically selecting a plan and effectuating the enrollment of people with an income up to 200 percent of the federal poverty level (FPL) by paying their first two months of premiums.8

Key Findings

In this brief, we combined the Urban Institute’s Health Insurance Policy Simulation Model (HIPSM) with new machine learning analysis of the Survey of Income and Program Participation (SIPP) to estimate the eligibility of Medicaid and CHIP enrollees 12 months after enrolling. (For more details, see “How We Conducted This Study.”) The SIPP data add a longitudinal dimension to our analysis, allowing estimates of change in eligibility over time. We show the number of those who retain eligibility and the number of those now eligible for PTCs along with demographic characteristics useful for designing important state and federal policy options for improving continuity of coverage. We also estimate the impact of policies that automatically enroll Medicaid enrollees who have become eligible for PTCs.

Most research on eligibility changes among Medicaid recipients is years old, often predating the Affordable Care Act. We are not aware of other work recent enough to consider current Medicaid eligibility rules and state policy options, the latest marketplace take-up rates, and the introduction of enhanced PTCs. This is also the first 50-state analysis of automatic enrollment policies for former Medicaid enrollees.

Children

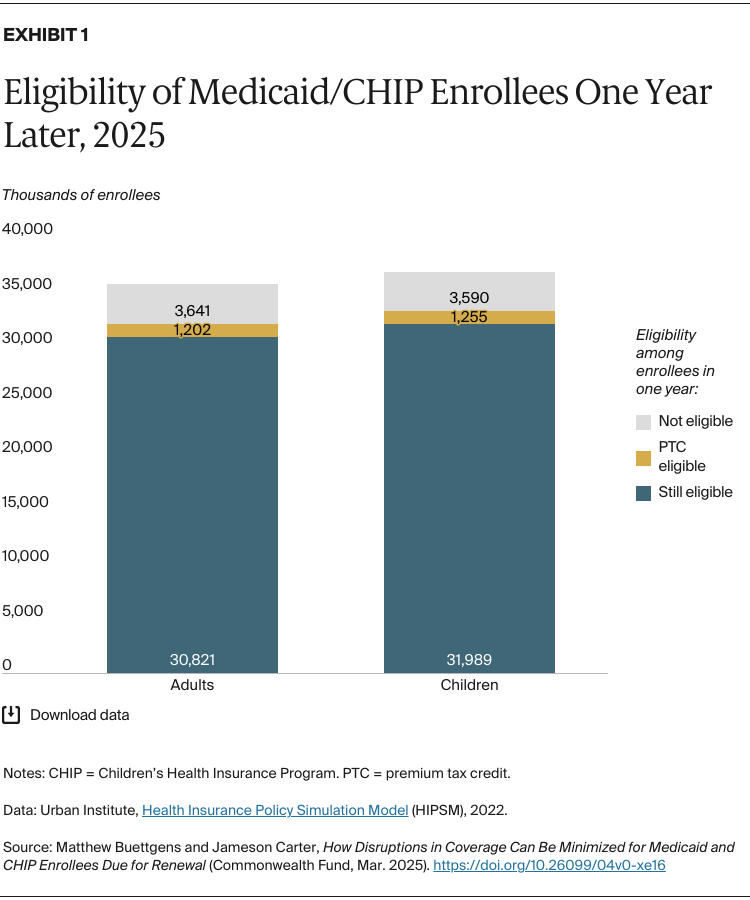

We estimate that about 36.8 million children will be enrolled in Medicaid or CHIP during the average month of 2025 (Exhibit 1). About 32.0 million of these (87%) will still be eligible for Medicaid or CHIP at the time of their renewal 12 months after enrolling. About 1.3 million children (3.4%) will be eligible for PTCs, and 3.6 million will not be eligible for PTCs due to affordable offers of coverage in their family.

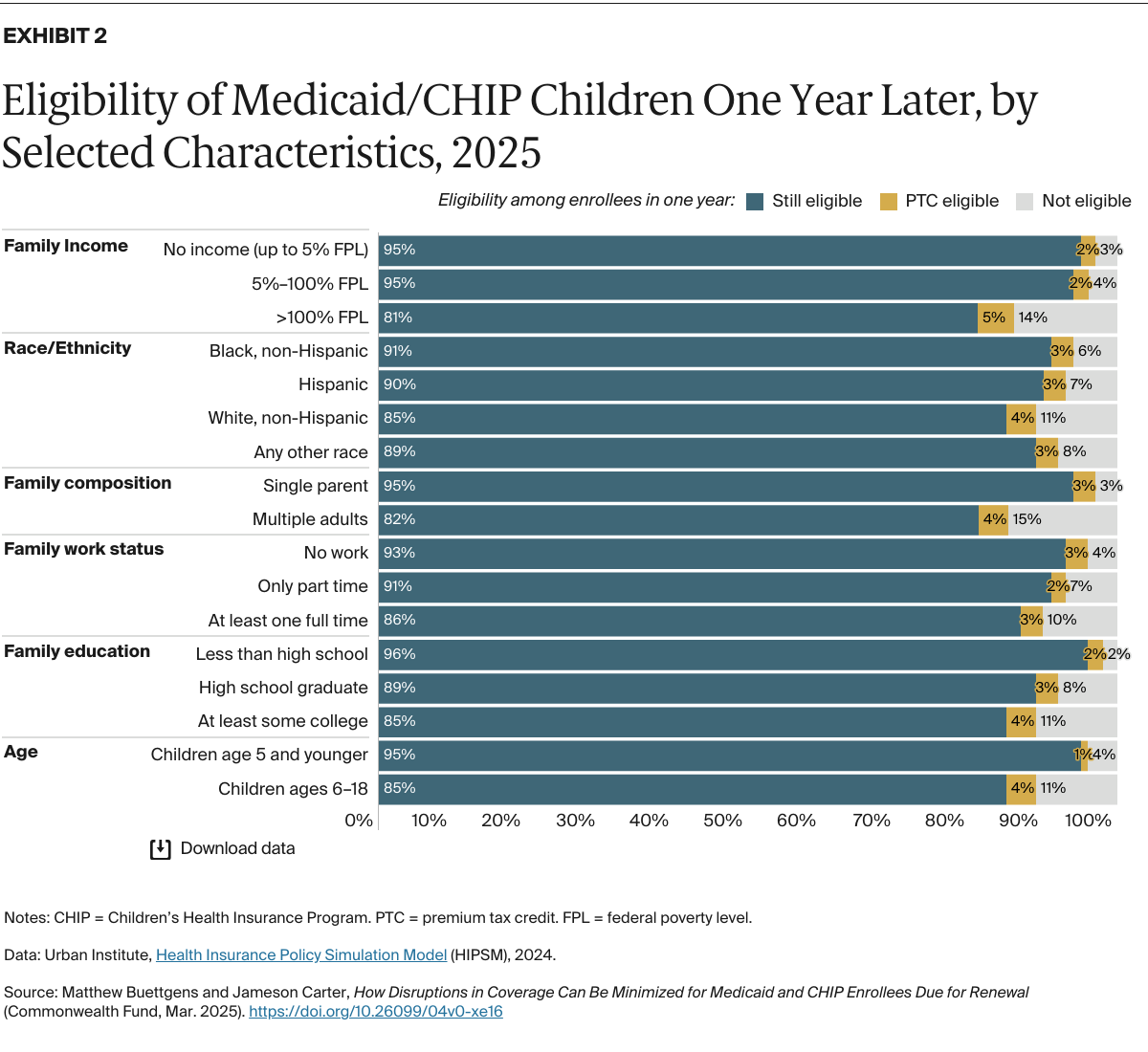

The overwhelming majority of children (95%) who were enrolled with a family income below 100 percent FPL remain eligible one year later (Exhibit 2). The federal Centers for Medicare and Medicaid Services (CMS) temporarily allowed states to automatically renew the enrollment of those whose last recorded income was below this level, and many states have interest in making this change permanent.9 Our estimates suggest that automatic renewal could improve overall accuracy of redetermination, considering the substantial reductions in the disenrollment of eligible children that would result.

Other groups of children extremely likely to still be eligible for Medicaid include those in single-parent families, those in families with less than a high school education, and children age 5 and younger. As of November 2024, Oregon, Hawaii, Minnesota, New York, and Pennsylvania had obtained waivers to extend continuous eligibility to children up to age 5 or 6; our results support this option.10