Over the past several decades in the United States, more and more health care providers and health insurers have consolidated, increasing their market power.1,2 Highly concentrated markets have contributed to the growth in U.S. health care spending because they are associated with higher health care prices and insurance premiums, yet are not typically associated with higher quality of care.2-4 Given that states play a large role in regulating health care provider and insurer markets, it’s important to understand how concentration levels vary across the country, as well as examine the relative concentration levels between providers and insurers at the local level. Our previous research has shown that in markets with both high provider and insurer concentration, insurers have bargaining power to reduce prices, yet consumers and employers don’t usually benefit.5 Regulators can use this information to determine if policies are needed to protect consumers, as well as employers that provide health benefits to their workforces.

To illustrate health care market concentration variability across the United States, we tabulated the market concentration of health care providers — hospitals, specialist physicians, and primary care physicians — and health insurers for each metropolitan statistical area (MSA) in 2016 using the methods and data described in the Appendix. Regulators classify markets into categories that range from unconcentrated to moderately concentrated to highly concentrated.6 We created a fourth category called “super concentrated,” to distinguish among the most concentrated markets (see the Appendix for details).

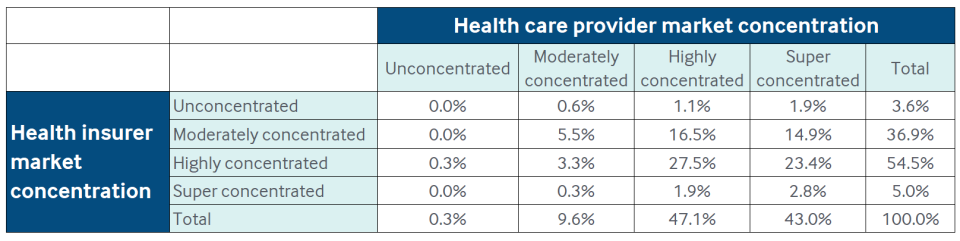

Market Concentration Levels Across the United States

When looking at market concentration levels across the United States, we found that, for both providers and insurers, the concentration levels varied, typically between two concentration categories (see table). For providers, the vast majority of the MSAs were at the concentrated end of the spectrum, either being highly concentrated (47.1%) or super concentrated (43.0%). By comparison, for insurers, almost all the MSAs fell into the middle categories, either being highly concentrated MSAs (54.5%) or moderately concentrated (36.9%).

When examining the relative concentration between providers and insurers, providers generally had the upper hand. Provider concentration was in a higher category relative to insurers in 58.4 percent of the MSAs, while the opposite was true in only 5.8 percent of the MSAs.

State and Federal Scrutiny Is Needed

This study shows that health care market concentration levels vary across the United States. To protect consumers and employers from high prices and premiums, state-level regulatory scrutiny — coupled with federal regulatory scrutiny — of potentially anticompetitive behavior is needed. State officials better understand the nuances of their local markets and are able to ascertain what steps, if any, may be required. For example, more populous MSAs may have lower measured concentration levels because they comprise more than one market. And even if a market is found to be highly or super concentrated, regulators should examine other competitive factors that may mitigate the potentially harmful impact of high concentration. These might include whether it is easy for competitors to enter a market or if there are economies of scale that might lead to lower costs.6 For example, as health care diagnoses and treatments become more complex, larger, more-integrated, and well-capitalized health care providers may be better equipped to lower costs and improve quality. Still, it is important for regulators to increase the likelihood that the benefits of consolidation ultimately flow to consumers and employers.