Medigap plans, also referred to as Medicare Supplement plans, help make beneficiaries’ out-of-pocket costs more predictable by paying part of their cost sharing. Unlike Medicare Advantage plans, which have variable designs and are managed at the county level, Medigap plans are often noted for their standardization, a result of legislation implemented in 1992, with largely consistent benefit categories for each plan type. This resulted in 10 Medigap plan types (designated by different letters) with varying levels of cost sharing but a consistent benefit set that allowed beneficiaries to make apples-to-apples comparisons across plans. However, regulations allow Medigap plans to offer additional benefits not covered by traditional Medicare, allowing for some variation in benefits across plans, even in this largely standardized market. With Medigap enrollment growing at more than 4 percent a year over the past five years and continued policy discussions on expanding access to dental, vision, and hearing services, it is important to understand the supplementary benefits offered under these plans and whether this addition has an impact on beneficiaries’ ability to navigate and access care through Medicare.

We analyzed Medicare Supplement policy data collected by the National Association of Insurance Commissioners, identifying plans (i.e., specific products) and insurance carriers that offer — either with or without additional premiums — additional “innovative” benefits, broadly defined as vision, dental, hearing, or other services not offered through traditional Medicare. We found that:

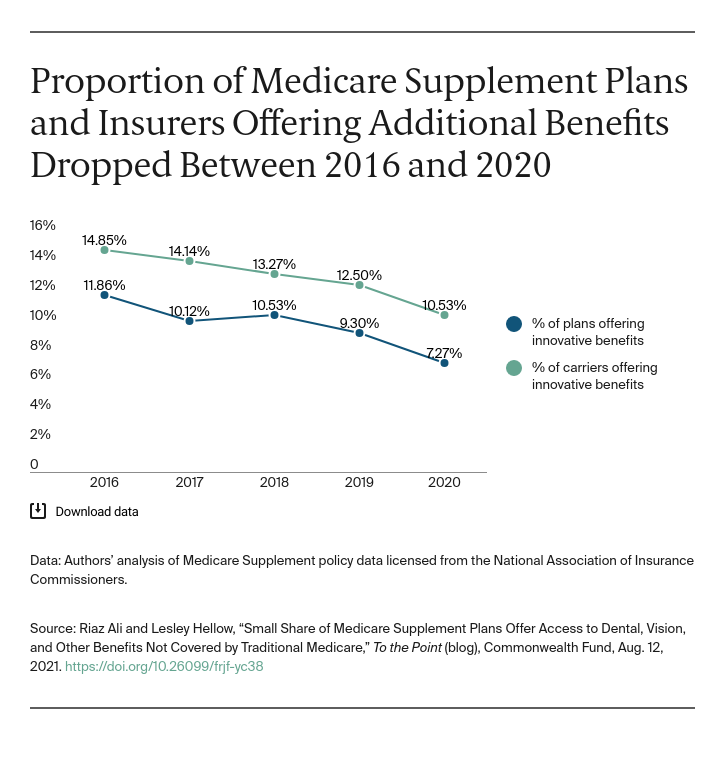

- A small, and declining share (7%) of Medigap plans, covering 12 percent of people with Medigap, provided access to these additional benefits not covered by traditional Medicare in 2020.

- These additional benefits are concentrated in a few plan types; nearly two-thirds (65%) of Medigap enrollees with access to these additional benefits are enrolled in Plan G.

The inclusion of these benefits complicates the otherwise standardized offering of Medigap and potentially complicates beneficiary decision-making. The added benefits also may increase premiums for Medigap plans, which may not always be clear or immediately apparent to beneficiaries.

On the other hand, lack of coverage for these benefits in traditional Medicare can increase beneficiaries’ out-of-pocket spending and limit access to these important services. The important question to consider is whether Medigap plans should be encouraged to provide broader access to these benefits to help more beneficiaries gain this coverage.

Additional benefits are most frequently found in the more commonly offered plans. In terms of beneficiaries covered, a single plan type represents nearly two-thirds of the covered lives with access to these additional benefits. Based on data reported to NAIC, in 2020, 12 percent of beneficiaries with Medigap were enrolled in plans with these additional benefits.

Impact on Beneficiary Decision-Making

Choosing whether to enroll in traditional Medicare, with or without a Medigap plan, or to enroll in a Medicare Advantage (MA) plan is complicated. This analysis highlights another way that traditional Medicare with Medigap diverges from MA, as access to additional benefits such as dental, vision, and hearing in MA is growing.

Beneficiaries are asked to make trade-offs about cost and access, with imperfect information about their future health needs. Moreover, given the differences between how Medicare Advantage and Medigap plans are designed, funded, and managed, with the former variable by county and the latter largely standardized, the decision is not a simple one for beneficiaries.

As the number of people enrolling in Medicare increases, policymakers must focus on the implications that Medigap benefit design has on quality, affordability, and access and whether efforts to provide additional benefits within Medigap plans is necessary to better meet beneficiaries’ needs.