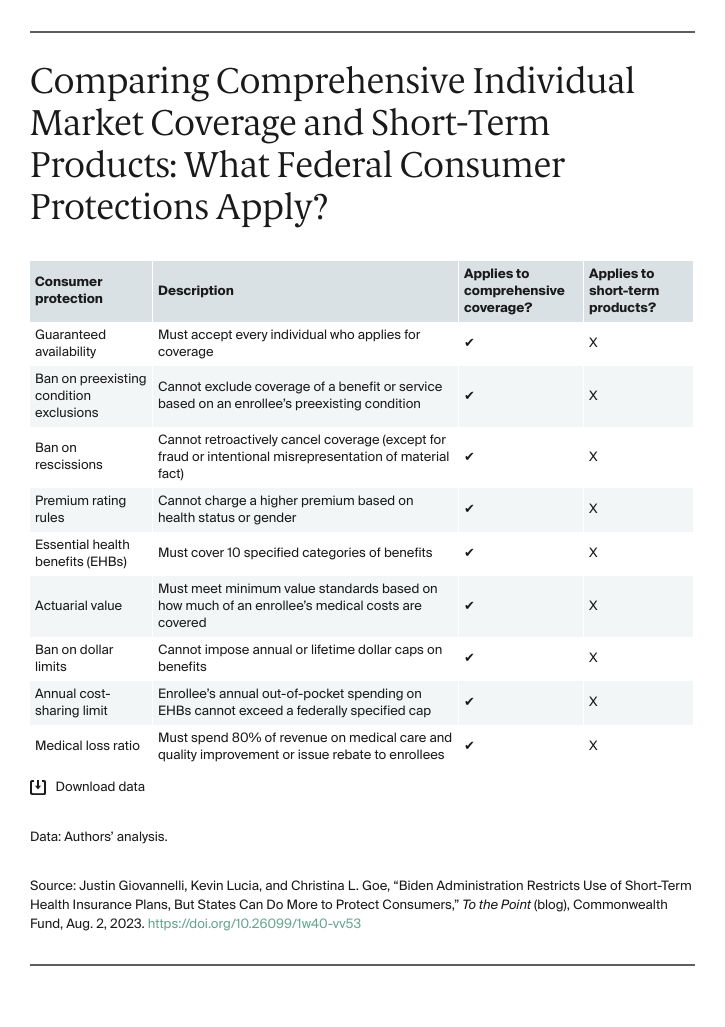

In July, the Biden administration proposed safeguards designed to help consumers navigate the critical differences between comprehensive coverage that is subject to the Affordable Care Act’s (ACA) consumer protections and other coverage arrangements — like short-term insurance plans — that are not.

As the name suggests, short-term plans were originally intended for people experiencing a short gap in comprehensive coverage; for instance, when switching from one job-based plan to another. Even though short-term plans aren’t covered by the ACA’s consumer safeguards, the Trump administration sought to promote these products as a cheap alternative to year-round comprehensive coverage. In 2018, the administration rescinded rules that limited the plans’ duration. This allowed short-term products to last 364 days and be renewed for an additional two years, for a maximum length of 36 months.

In the years since, new laws have significantly improved the affordability of ACA marketplace coverage. At the same time, the dangers to consumers of ACA-exempt products have become more evident. The Biden administration’s proposed regulations would reestablish tighter limits on the length of short-term plans. It is also considering policies that would make it easier for consumers to evaluate their coverage options.

Evidence Shows Unregulated Short-Term Products Endanger Consumers

Unlike ACA-compliant coverage, short-term plans don’t cover preexisting conditions and may decline to sell a policy based on a person’s health. They usually exclude common benefits such as prescription drugs, mental health care, maternity care, and preventive services. And they limit the benefits they do cover, with dollar caps and unregulated cost-sharing designs that require out-of-pocket spending that is far higher than what is permitted in comprehensive coverage. These limitations typically make for a product with a low upfront cost, which may be appealing to some people who are healthy (and stay that way) and they are highly profitable for the companies that sell them. But for enrollees who do need care, short-term plans are likely to result in much higher overall costs. Depending on a consumer’s diagnosis, they open the door to potentially catastrophic financial hardship.