Employer-sponsored insurance (ESI) — that is, health insurance people get through their jobs — is the primary source of health insurance coverage in the United States. ESI covered about 178 million people in the United States in 2023, including 63 percent of working-age adults ages 19 to 64 and 54 percent of young people under age 19. However, the costs of ESI paid by employees — premium contributions, deductibles, and copayments and coinsurance — can pose a considerable financial burden on U.S. households, particularly in those with low and moderate incomes.

To assess the affordability of health insurance costs for workers, we compared employee premium contributions and deductibles, relative to state median income, using federal survey data in all 50 states and the District of Columbia. We found that income growth helped improve the affordability of workers’ coverage between 2022 and 2023 overall, but there is significant variation in the affordability of premiums and deductibles across the country.

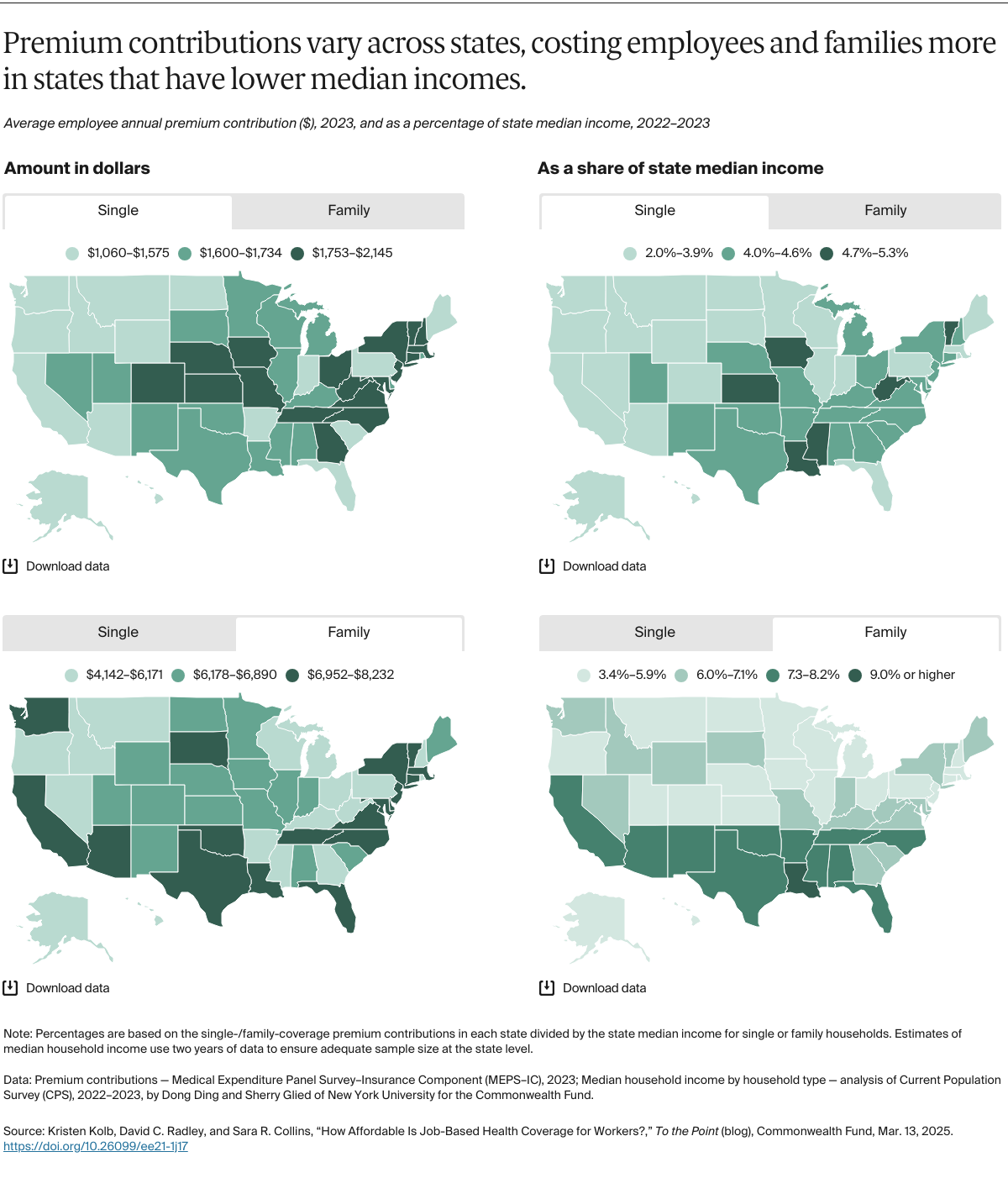

Total annual premiums for single coverage ranged from an average of $7,243 in Mississippi to $9,662 in New Jersey in 2023 (Appendix Table 5). Across the states, employers pay for 65 percent to 85 percent of health insurance premiums and workers contribute the balance. The average annual dollar amount workers contributed to their premiums for single-person coverage ranged from $1,060 in Hawaii to $2,145 in Vermont. Relative to income, worker contributions for single coverage ranged from 2 percent of the state median income in D.C. to over 5 percent in Mississippi. While the average premium contribution for single coverage in Mississippi was near the national average, the lower median income makes Mississippi one of the least affordable states in the country for workers enrolled in ESI.