Introduction

To help people afford plans sold in the health insurance marketplaces, the Affordable Care Act (ACA, also sometimes called Obamacare) provides low- and middle-income individuals with premium tax credits (PTCs). In 2021, Congress enhanced the generosity of these tax credits and made them available to more people. Authorized originally by the American Rescue Plan Act, the enhanced PTCs were later extended by the Inflation Reduction Act through December 2025. Together, these changes have made marketplace health insurance coverage more affordable.1 As of January 2025, 24 million Americans had selected a marketplace plan, about twice as many as in 2021.2

If Congress does not reauthorize the legislation that provides the more generous tax credits, this financial lifeline will no longer be available to consumers after December 31, 2025. There would be a sharp rise in the net cost of marketplace premiums, and many Americans would no longer be eligible for tax credits to defray the cost of their plan premiums.

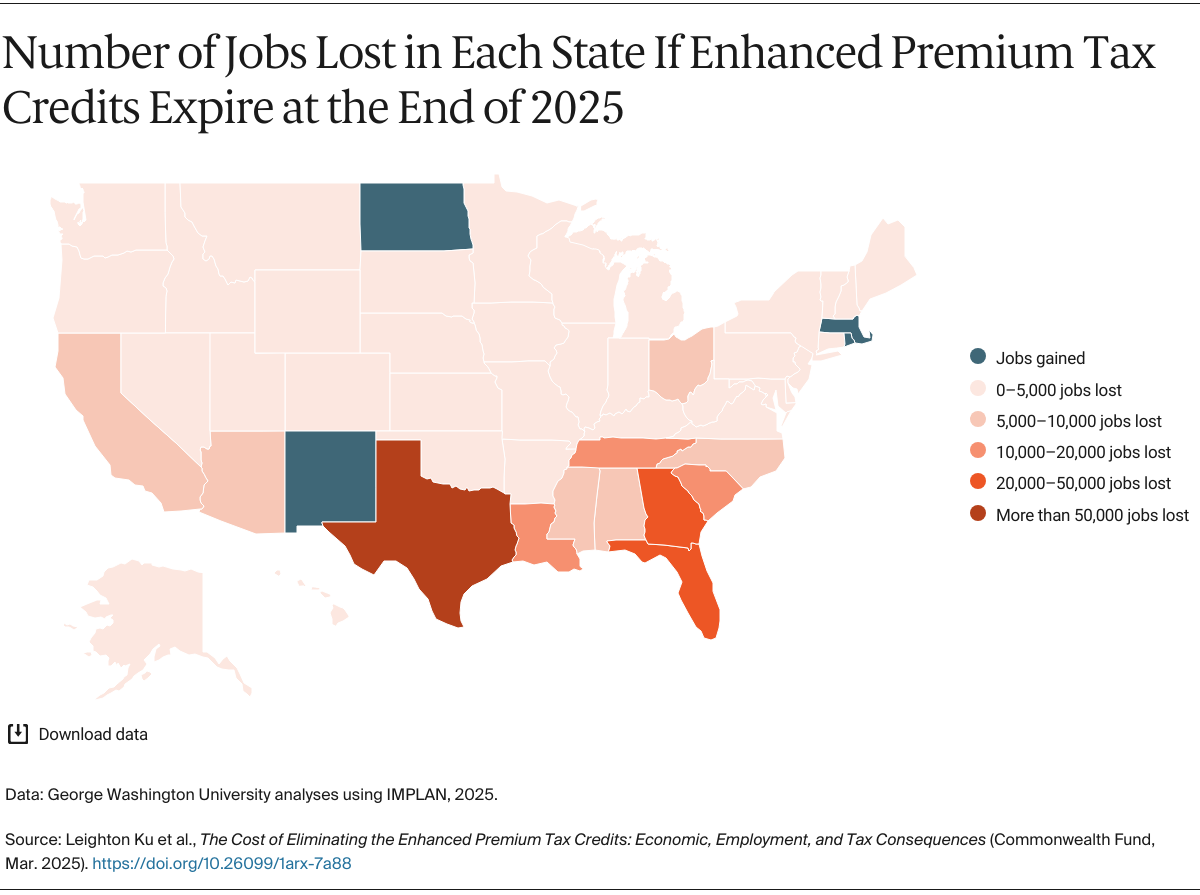

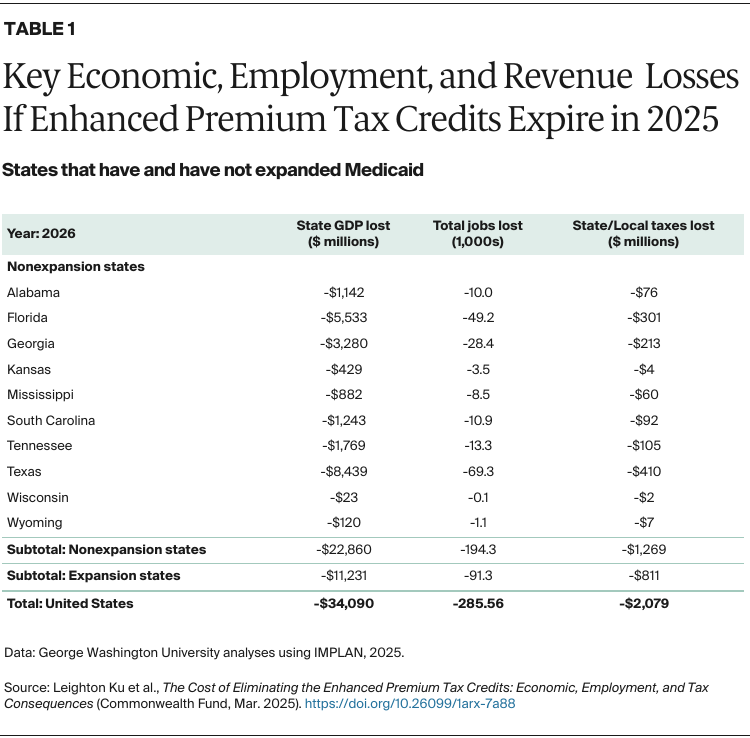

This will lead to dramatic losses in health coverage: 4 million more Americans will become uninsured.3 Among those who will feel the consequences most severely are Black and Latino Americans and people in states that have not expanded Medicaid under the ACA, including Alabama, Florida, Georgia, Idaho, South Carolina, Tennessee, and Texas, where disproportionately more residents depend on marketplace plan subsidies to get their health care.4

Beyond the direct impact on consumers, this policy change will have a ripple effect across the entire health care industry — hospitals and other care providers, insurers, health workers, businesses that supply health care facilities, and those companies’ employees. In this data brief, we project the impact on economies, employment, and tax revenue in all 50 states and the District of Columbia.

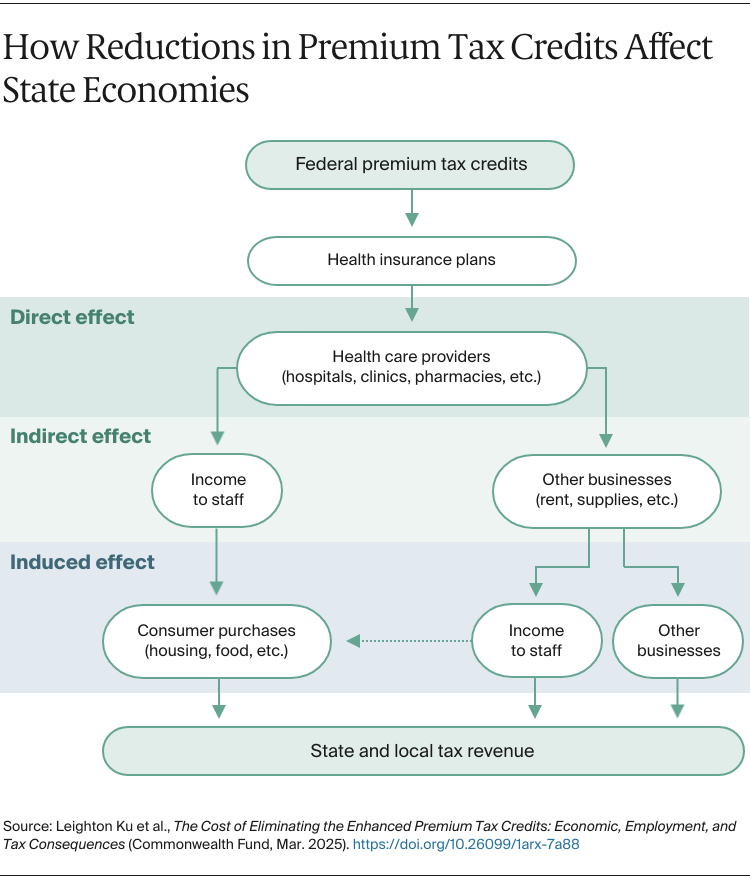

The dynamics of this ripple effect work as follows. As the enhanced PTCs disappear, former recipients will likely either become uninsured or shift to another form of health insurance.5 Health insurers, in turn, will no longer collect the PTCs (and other insurance payments), causing them to cut payments for patient care to hospitals, doctors’ offices, pharmacies, and other health providers.6 For their part, health providers will need to cut jobs — some could even close due to loss of revenue. This would lower access to health care overall, even for people who remain insured.

Providers will also need to reduce payments to businesses in their supply chains, and, in response, those firms will be forced to cut labor and other costs. As employees lose income, they must reduce spending on consumer goods and services. Finally, the loss of individual and business income results in less state and local tax revenue collected.

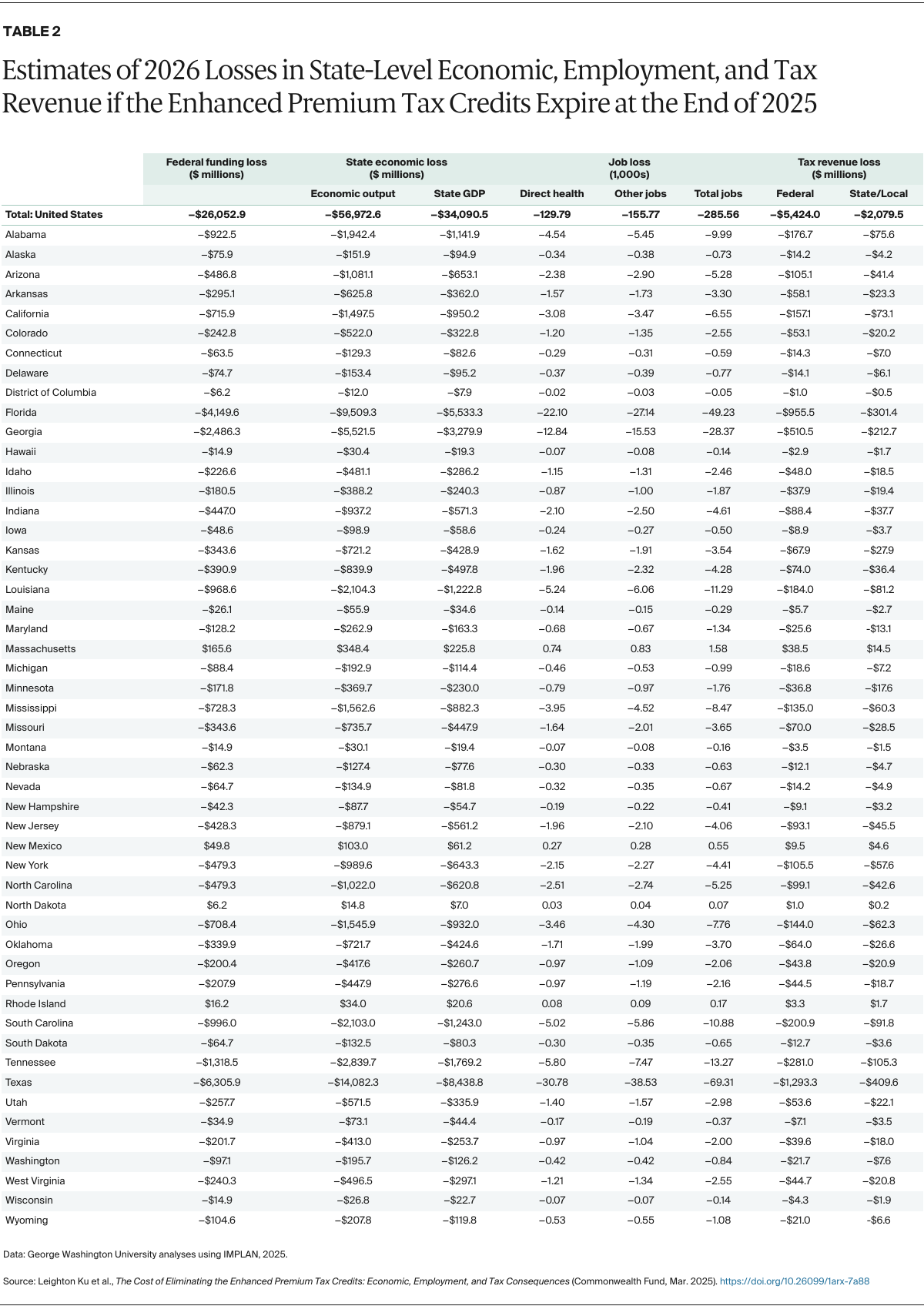

To produce our estimates of this cascading economic impact, we ran data through a widely used software program called IMPLAN (for complete methods, see “How We Conducted This Study”). Table 2 at the end provides detailed findings of the estimated impacts for states in 2026. We highlight key findings below.

National Findings

Loss of financial support. Across states, the federal tax credits that individuals, health insurers, and, ultimately, health care providers receive would fall by $26.1 billion in 2026, compared to a baseline in which the enhanced PTCs were continued. (Although we do not show this here, the losses climb in subsequent years, as projected by the Congressional Budget Office.7)

Reduced economic activity and personal income. Ending enhanced PTCs would reduce state economies across the nation. Total state gross domestic products (GDPs) would fall by $34.1 billion and total economic output would fall by $57.0 billion. The net economic harm for states would therefore be much larger than the loss of federal funds ($26.1 billion) to states. This includes direct losses to health care providers and indirect and induced impacts to other economic sectors, as losses spread across businesses and their employees in each state. For example, with lower funding, health care providers will need to reduce the goods and services they purchase from other businesses, such as information technology and real estate, which in turn will lead them to reduce the number of their employees.

For individuals and families, the loss of personal income means less money to spend on consumer goods and services like groceries, housing, and transportation. The impacts will extend beyond the health care sector to affect most parts of states’ economies.

Loss of jobs. Overall employment would decline by a total of 286,000 jobs nationwide in 2026. This includes 130,000 jobs lost because of direct reductions in the provision of hospital, physician, and other ambulatory care as well as reductions in pharmacy-related services. It also includes 156,000 jobs lost in nonhealth sectors like retail, real estate, and manufacturing as a result of the indirect or induced effects of health care funding losses. Rural communities in particular could be among the areas hardest hit.

Reduced tax revenues. The reductions in income and economic activity will lead to losses of $2.1 billion in state and local tax revenues in 2026, as well as $5.4 billion in reduced federal tax revenues. The loss of state and local tax revenues would make it harder for state and local governments to balance their budgets and continue paying for crucial services like education.

The estimates detailed above are similar, but somewhat larger, for 2027 and 2028, as the value of enhanced PTCs would grow if they were to be continued.