Many people who purchase health insurance through the Affordable Care Act’s marketplaces are eligible for tax credits that lower their monthly premiums. In 2021, as the COVID-19 pandemic still raged, Congress made those tax credits more generous. This improved the affordability of marketplace health plans, which was a barrier to many people who needed coverage, even prior to the pandemic. Lower costs of coverage drove record enrollment in the marketplaces through 2025. But these lower premium costs will end after 2025, unless Congress acts to extend the tax credits.

What are the enhanced premium tax credits and how do they work?

As part of the American Rescue Plan Act of 2020, Congress increased the ACA marketplace premium tax credits (PTCs) to ensure that Americans had access to affordable health insurance during the pandemic. In 2022, Congress extended these enhanced tax credits through 2025 as part of the Inflation Reduction Act.

The tax credits reduce the insurance premiums that enrollees pay based on their projected income for the next year. The credits are paid directly to health insurers, who in turn lower the monthly amounts they charge. The credit amounts then need to be reconciled with actual income at year’s end when enrollees file their federal taxes.

Enhanced premium tax credits provide additional subsidies to people who are already eligible for the regular tax credits. In addition, they extend tax credits to people with annual income equivalent to 400 percent of the federal poverty level (see table below) or higher, thereby eliminating the ACA’s “subsidy cliff,” which rendered people with incomes even just above 400 percent of poverty ineligible to receive financial assistance for coverage. With the enhanced subsidies, most enrollees at the lowest income level — under 150 percent of poverty — pay little or nothing for their plan. Individuals with incomes of $60,240 or more, meanwhile, pay no more than 8.5 percent of their household income.

How have the enhanced tax credits affected the affordability of health coverage?

With the implementation of enhanced tax credits, marketplace plan premiums fell for people at all income levels, and plan choices increased. In 2023, enhanced subsidies provided 15 million people with an average of $800 in annual premium savings. In 2023 and 2024, 80 percent of marketplace enrollees could find a plan for $10 or less per month on HealthCare.gov, the federal marketplace that operates in 31 states (19 states and the District of Columbia run their own marketplaces). In 2020, before the tax credits were increased, only 36 percent of PTC-eligible enrollees could find such a plan. Across all income groups, projections of annual household spending on premiums and out-of-pocket costs fell in 2025.

The share of HealthCare.gov enrollees with a choice of three or more plans increased from 78 percent in 2021 to 96 percent in 2024. While enhanced PTCs do not directly alter patient cost sharing, they allow people to enroll in or switch to plans that have lower cost-sharing obligations. From 2021 to 2024, the number of people in plans with reduced cost sharing, including lower deductibles, climbed from 5.7 million to 10.6 million.

The enhanced subsidies are especially beneficial to people in rural areas of the country. Benchmark premiums in rural areas are about 10 percent higher than in urban areas, meaning that rural residents benefit the most from enhanced premium subsidies.

How have the enhanced tax credits affected how many people have coverage?

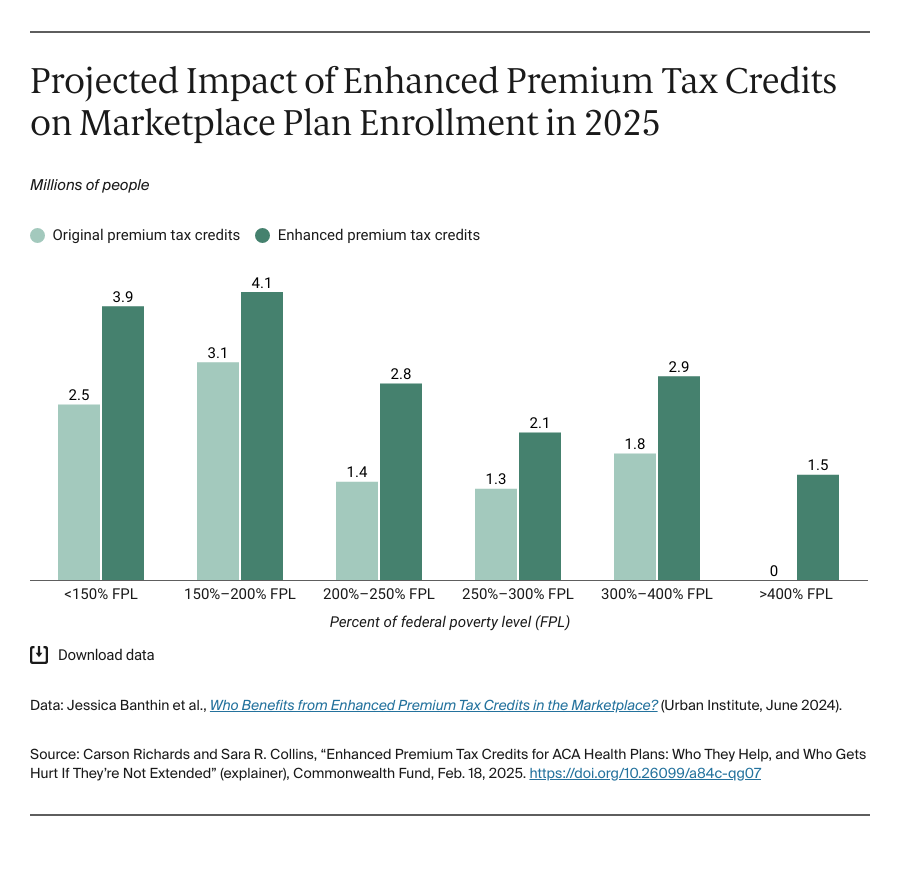

The enhanced subsidies have translated into higher enrollment in ACA marketplace plans and fewer uninsured people. They helped increase enrollment in the marketplaces from 12 million in 2021 to a record 24.2 million in 2025. Ninety-three percent of marketplace enrollees rely on the premium tax credits to make their insurance premiums affordable.

The enhanced credits will enable an estimated 3.4 million to 4.0 million previously uninsured people to gain coverage. These subsidies especially benefited people with the lowest incomes, increasing enrollment among people with incomes below 250 percent of poverty from 8.2 million in 2021 to 15.9 million in 2024. About 1 million more people with incomes above 400 percent signed up for ACA marketplace plans between 2021 and 2024.

The enhanced tax credits have been particularly important in states that have not expanded Medicaid. If the tax credits expire, five southern states — Texas, South Carolina, Mississippi, Tennessee, and Georgia — could see a 27 percent or greater increase in the number of residents without health insurance.

The enhanced tax credits also expanded the number of affordable coverage options for workers who were in employer plans they couldn’t afford, and they provided small businesses with more cost-effective options for their employees.

What would happen if Congress doesn’t extend the enhanced tax credits?

Without congressional action to extend the enhanced credits, net premium costs for eligible enrollees will spike by 25 percent to 100 percent. Four million people would likely become uninsured. If healthier people drop their insurance, leaving less healthy people in the marketplace, premiums could further increase.

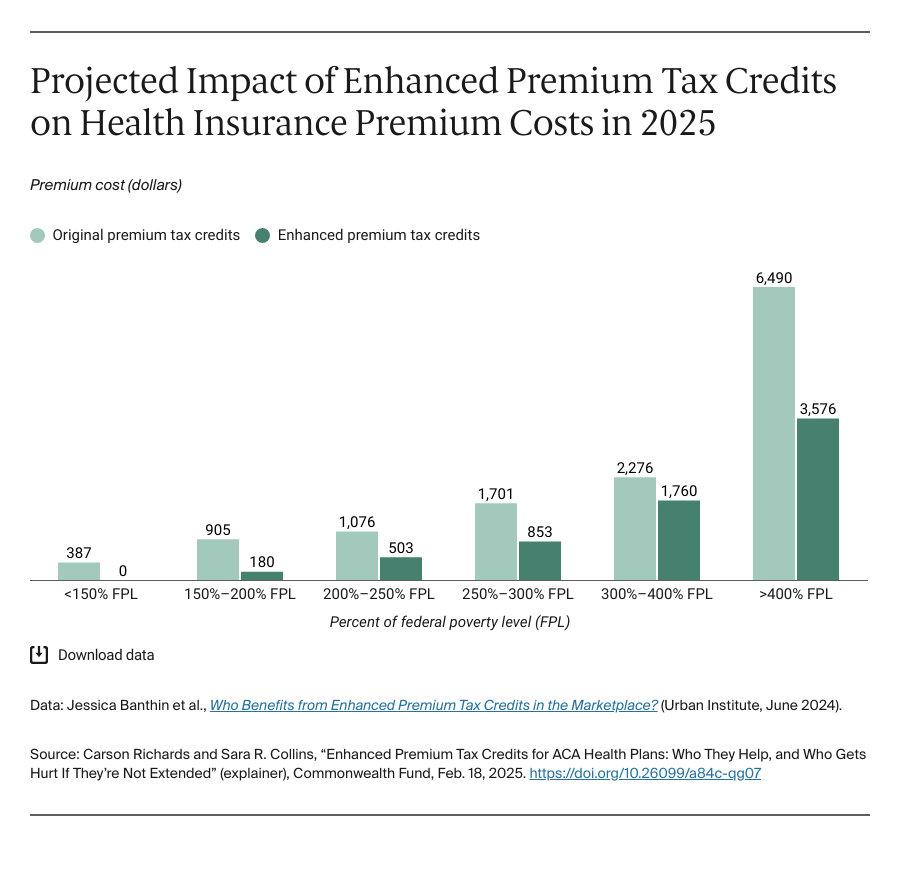

Projected average annual premiums would increase for marketplace enrollees across all income groups:

- <150% of the federal poverty level (FPL): $387 more

- 150%–200% FPL: $725 more

- 200%–250% FPL: $573 more

- 250%–300% FPL: $848 more

- 300%–400% FPL: $516 more

- >400% FPL: $2,914 more.