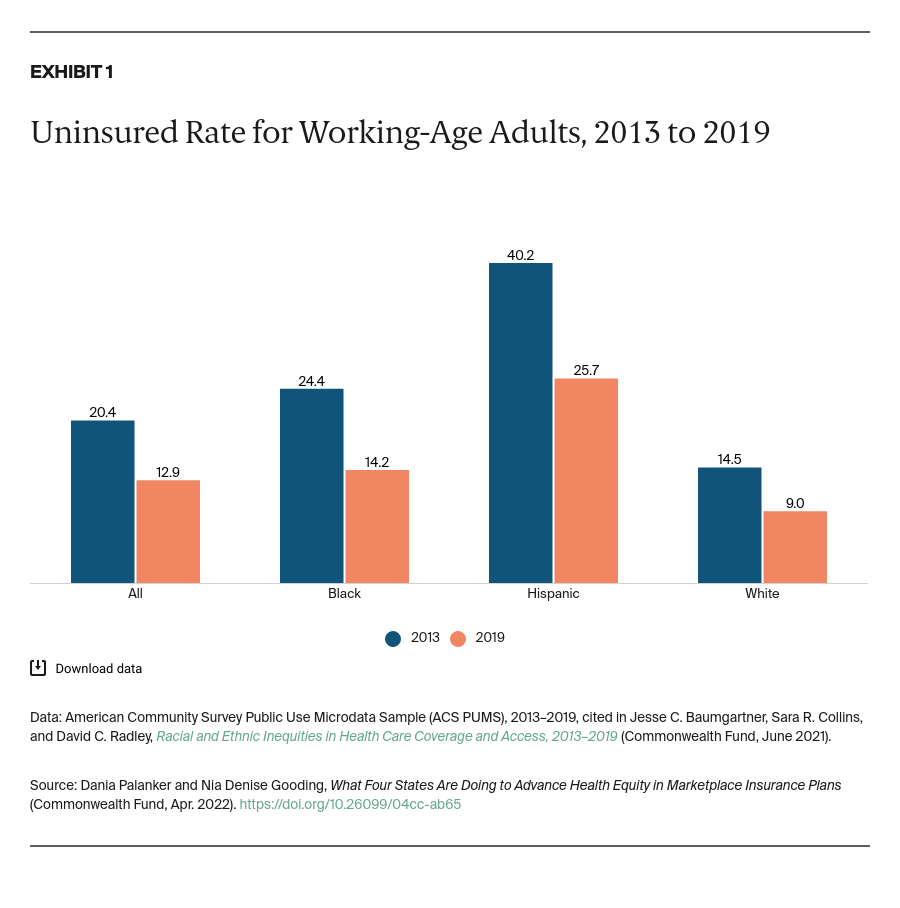

Providing equal access to health coverage, however, is not enough to ensure health equity. In the context of health coverage, health equity also entails the elimination of disparities that prevent enrollees from living as healthy a life as possible.3

More than 12 million people are enrolled in coverage through the state-based marketplaces (marketplaces) and the federal marketplace.4 The marketplaces were created under the ACA with a mission to expand enrollment in affordable health insurance and, in doing so, reduce enrollment disparities.5 The marketplaces also play a key role in implementing and overseeing the provisions of the ACA that can reduce health inequities, such as requiring insurers to contract with essential community providers, requiring preventive care coverage, and prohibiting health benefit design and other discrimination.6

While the marketplaces have not traditionally targeted equity as distinct from disparities and equality, some marketplaces are now leading efforts by crafting and implementing health equity strategies (Exhibit 2). This brief, based on a review of workgroup and board meeting materials, published reports, and interviews with marketplace officials and stakeholder representatives, explores marketplace equity strategies pursued in California, Connecticut, the District of Columbia, and Massachusetts (see “How We Conducted This Study” for further detail).

Findings

Shared Goals, But Lack of Clarity on Definitions or Approach

The state marketplaces we studied do not clearly define equity, although they do consider equity as broader than just reducing enrollment disparities and different from equality. One official explained that “equity goes beyond injustices in different access to health insurance,” and that it is possible that “components of the coverage experience . . . have increased burden, abrasion, inconvenience, difficulties, etc.” The marketplaces are targeting inequities based on race and ethnicity with a recognition that additional categories, such as gender identity, should be considered in the future. There is no consensus among the four states on how to reach equity; the strategies they are using are varied and in different stages of development and implementation.

Gathering Data to Better Understand Plan Enrollees

Stakeholders in our study articulated that collecting comprehensive data is a necessary first step to understanding the enrolled population and accurately identifying drivers of inequities. “The data will lead to knowledge, and the knowledge will lead to fixes internally,” one official noted.

Data collection. Marketplaces need to improve demographic data they and insurers collect on enrollees, including race and ethnicity. All marketplaces collect such data through questions on applications, but response rates are low — a problem that is common to most state marketplaces as well as the federal marketplace.7 To remedy this, the District of Columbia’s marketplace will begin sharing with insurers race and ethnicity data reported on applications, and insurers have agreed to reach out to enrollees to fill in missing data.8 California requires each insurer to collect “self-identified race and ethnicity data” for at least 80 percent of marketplace enrollees.9 California also will require that insurers achieve health equity accreditation — signifying compliance with standards including those for collecting race, ethnicity, and language data — from the National Committee for Quality Assurance (NCQA).10

Data aggregation, analysis, and use. After collecting demographic enrollment data, marketplaces or insurers have to aggregate and analyze the data to identify gaps in health care access and inform the development of options to reduce inequities. California is tying financial incentives to insurers’ use of data to drive improvements in quality of care.11 Massachusetts wants to analyze data to understand if administrative rules for enrolling in and maintaining coverage are “inadvertently more abrasive to populations of color,” as one official explained. The District of Columbia is working with insurers to determine whether race-based differences in medical treatment plans or clinical algorithms are contributing to differences in health outcomes.12

Designing Plans to Meets the Needs of People of Color

The four marketplaces are interested in using plan design as a lever for improving access to care for targeted populations. For example, respondents in three states highlighted a state or marketplace rule that insurers cover insulin at low or no cost, a requirement that promotes equity because diabetes disproportionately affects people of color.13

The ACA, however, limits states’ ability to leverage plan design. States must pay for any new benefit mandate that is not part of the essential health benefits package. In addition, the ACA requires plans meet specific ranges of actuarial value — the percentage of average health costs devoted to delivering covered benefits — which limits the ability of state marketplaces to vary cost-sharing features.

Equity-based insurance design. Starting in 2023, Massachusetts’ ConnectorCare plans — available to people with income under 300 percent of the federal poverty level — will have no cost sharing for primary care sick visits, mental health outpatient, and some medications for conditions that disproportionately affect communities of color.14 The District of Columbia’s marketplace introduced standardized plans for the entire individual market and for small-group markets; these eliminate cost sharing for services aimed at preventing and managing diabetes, starting in 2023. The marketplace intends to extend that policy change to four more chronic conditions prevalent among people of color.15 To balance plans’ actuarial value, the marketplace expects in future years to raise cost sharing on what are deemed to be “low value” services.16 (Higher cost sharing was not needed for the diabetes changes.)

However, the District to Columbia’s marketplace workgroup raised the concern that increased cost sharing might not change consumer behavior in accessing specific services, unintentionally resulting in some people of color paying more. Insurers will be expected to review claims data to analyze the effectiveness of the value-based design.17

Ensuring Enrollees Can Use Their Plans and Are Receiving Equitable Care

Nearly all stakeholders and officials noted that consumers are both underutilizing their plan coverage and experiencing barriers and inequities in accessing care. Marketplaces are identifying strategies for tackling these barriers.

Network adequacy. Marketplace officials and consumer advocates cited network adequacy as an important issue but did not have clear plans to create an equity-focused network. California aims to provide all enrollees with access to health care providers that are “high quality and efficient.”18 Insurers in the District of Columbia will analyze their provider networks to determine whether they reflect the demographics of the enrolled population and to learn where providers are located.19 Provider contracts will also require in-network providers to receive annual training in cultural competency — how to provide care that is responsive to patients’ social, cultural, and linguistic needs.

Multiple respondents mentioned larger problems with network adequacy that are outside marketplaces’ control, such as communities without hospitals and structural racism in the medical education system. Insurers in the District of Columbia will provide targeted medical education scholarships to students of color to increase the number of physicians of color.20 The Massachusetts marketplace will require ConnectorCare plans to contract with providers that will be certified under another state program aimed at improving access to community-based mental health and substance use care.21

Enrollee education. Connecticut is looking to create a subsidiary organization to address social determinants of health that are outside the scope of the state marketplace’s mission.22 For example, officials are looking to create a concierge service in one or more of Connecticut’s larger cities to ensure enrollees have access to transportation to health care appointments. An insurance literacy tool may also be developed to help enrollees learn how to use their insurance — an idea that emerged from survey data finding disparities in use of health services.23 But one stakeholder expressed concern that such efforts focus on the individual rather than on systemic issues, such as overall health literacy.

Quality improvement. California officials highlighted that the state’s marketplace is undertaking comprehensive data collection to improve quality of care. Insurers are required to create goals, based on collected data, to improve quality and increase equity. In the future, California intends to impose financial penalties on plans that fail to meet their equity goals.24

Ensuring the Marketplace Is Accountable for Meeting Equity Goals

Some of the marketplaces we studied are creating accountability structures for their equity programs. For example, three marketplaces have staff positions dedicated to overseeing work on health equity. Initially, California’s equity officer mainly oversaw marketing and outreach initiatives. But since the position was moved to the Plan Management Division, which works with insurers on plan requirements, the officer is now more directly focused on disparities reduction and quality improvement.

The District of Columbia promotes equity not only in marketplace policy but also in the workplace environment, through mandatory monthly staff trainings, a speaker series, and coaching by external experts. Massachusetts uses a “racial equity checklist” to ensure its marketplace staff consider equity in all major policy changes or programs.25 The equity advisor for the District of Columbia marketplace is using a similar tool to review internal policies.