In the past few years, the Affordable Care Act (ACA) marketplaces experienced significant enrollment growth, contributing to historically low uninsured rates. This is largely attributable to enhanced premium tax credits enacted in 2021 and to marketplace efforts to reduce barriers to coverage, including the expansion of open-enrollment and special-enrollment opportunities.

In March, the Trump administration released a draft regulation that would limit those enrollment opportunities and increase paperwork requirements for consumers to prove their eligibility for coverage and tax credits. The administration argues that the current policies have prompted less-healthy people to enroll (this is known as adverse selection), which led to an increase in premiums. However, there is limited evidence that expanded open- and special-enrollment periods have led to adverse selection. In fact, data from several state-based marketplaces (SBMs) suggest that reducing administrative burdens around enrollment and conducting robust consumer outreach can both grow enrollment and improve the health of marketplace risk pools.

What is the Purpose of Open- and Special-Enrollment Periods?

The marketplaces offer consumers a single annual open-enrollment period (OEP). If people experience certain life events, such as the loss of other insurance coverage, a move, marriage, or birth or adoption, they can qualify for a special-enrollment period (SEP). When enacted, the ACA created limited enrollment windows out of concern that if people could enroll at any time, they would wait until they were sick or injured to sign up. An insurance risk pool with only sick enrollees would have extremely high premiums and be unattractive for insurers.

At the same time, if enrollment opportunities are overly narrow, and the paperwork required to qualify burdensome, healthy individuals are likely to avoid the hassle and not sign up at all. Although the cost of premiums is the primary reason people cite for being uninsured, administrative burdens have also proven to be a major deterrent. Policies that strive to boost marketplace enrollment, for instance, through enhanced premium tax credits, robust marketing and outreach, and streamlined application processes, can improve the risk pool and keep premiums stable.

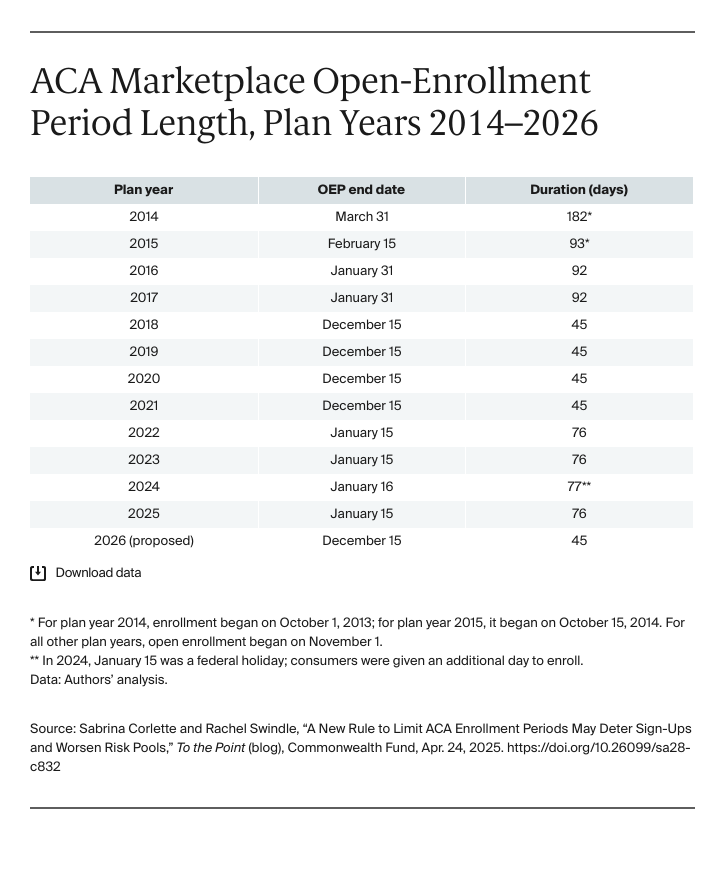

How Have Marketplace Enrollment Windows Evolved Over Time?

When the ACA marketplaces first launched in 2014, the annual OEP extended from the beginning of November into the spring, giving consumers time to understand their new options. By 2016, the window was shortened to 92 days, ending on January 31. In 2017, the OEP for the federally facilitated marketplace (FFM) was cut back significantly to end in mid-December; individuals seeking coverage outside the OEP were newly required to submit proof of eligibility for a SEP.

The Biden administration later extended the OEP for the FFM through January 15, noting that many consumers were not notified of premium changes until after December 15, giving them insufficient time to change plans. In addition, many lower-income individuals face financial stress and limited time during the holiday season and benefit from a longer OEP. The Biden administration added a new monthly “low-income SEP” for individuals with incomes under 150 percent of the federal poverty level (FPL, currently $22,590 in annual income for an individual), allowing those who qualify to enroll throughout the year. In addition, because paperwork can present a barrier to coverage and primarily inhibits younger, often healthier people from enrolling, the Biden administration eased many of the paperwork burdens for consumers who needed SEPs.

Among other policy changes, the recently proposed marketplace rule would 1) shorten the OEP to 45 days, reverting to a mid-December deadline; 2) eliminate the monthly SEP for low-income individuals; and 3) institute preenrollment documentation requirements to prove SEP eligibility.

State-Based Marketplaces React to the New Regulations

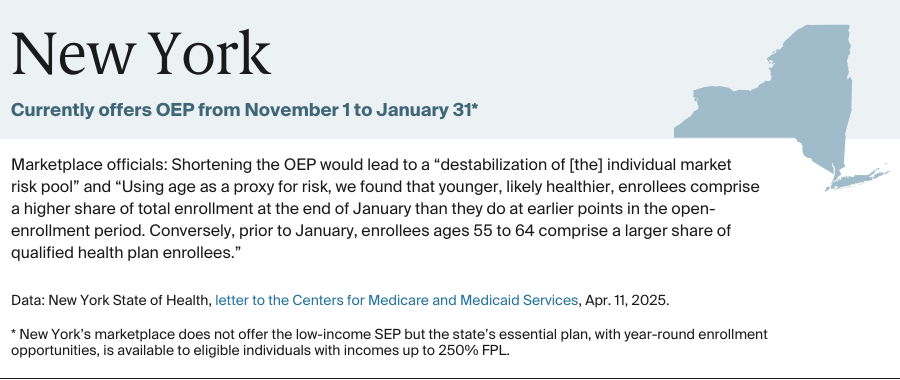

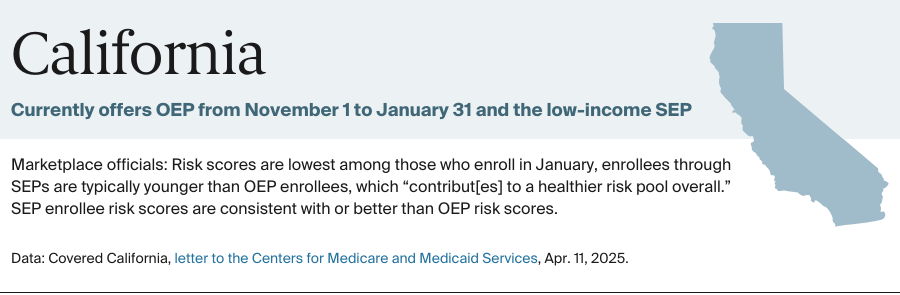

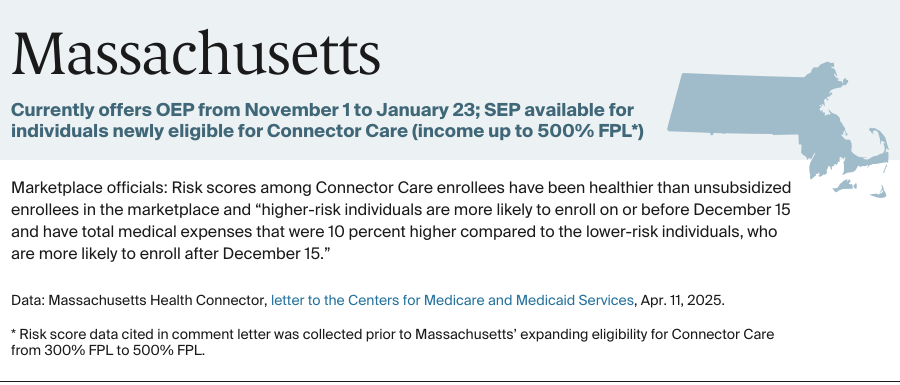

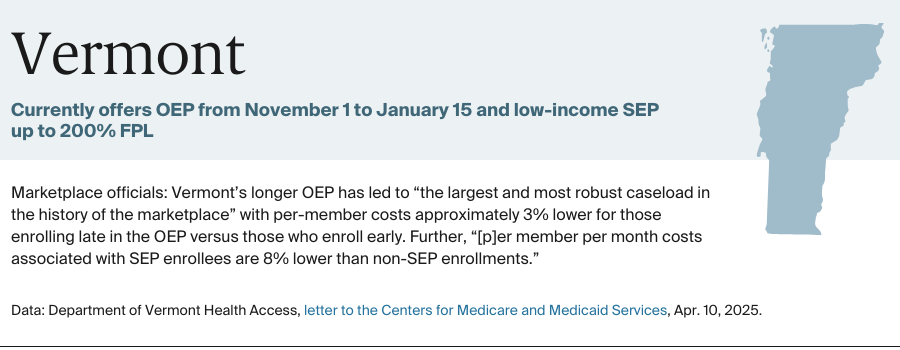

SBMs have long had discretion to establish their own enrollment periods, and many have adopted longer OEPs and more SEPs than the federal marketplace has. In a striking departure from past practice, the new rule would require all SBMs to adhere to more restrictive federal standards. Yet evidence suggests that expanded enrollment opportunities, when combined with robust consumer outreach, result in more insurance sign-ups, particularly among younger and healthier individuals. For example, four SBMs have recently shared helpful data about who enrolls during their OEPs and SEPs.