Abstract

- Issue: Employer-based health insurance has become less affordable for many Americans over the past decade, with premium contributions and deductibles taking up a larger share of household income. As millions of workers lose income through furloughs and wage cuts, COVID-19 may exacerbate this trend. One proposed solution is to make it easier for workers and their families to enroll in subsidized health plans through the Affordable Care Act (ACA) marketplaces. Such a change would remove the current “firewall” between employer plans and marketplace coverage.

- Goal: To analyze the potential effects of a proposal to allow more workers and their families to purchase ACA marketplace plans, both with the subsidies currently available and with more generous ones.

- Methods: Analysis of the 2018 and 2019 Current Population Survey’s Annual Social and Economic Supplement.

- Key Findings and Conclusions: Between 6 percent and 13 percent of people in nonelderly households covered by employer insurance could pay lower premiums through a marketplace plan if the firewall were lifted. The vast majority of those benefitting would be low- or middle-income families. Residents of southern states would particularly benefit, since their employee plan premiums often take up a larger percentage of household income than the national average.

Introduction

The COVID-19 pandemic has triggered the worst economic downturn since the Great Depression: Around 70 million people have lost jobs or been furloughed since March.1 An estimated 14.6 million people have lost jobs that also came with health insurance, with more possible if the virus continues to rage out of control and affect sectors where more workers get employer-based coverage.2

The Affordable Care Act’s (ACA) coverage expansions are expected to keep the number of newly uninsured lower than in past recessions.3 However, the deep contraction in the economy means that millions more will suffer income loss through furloughs, wage cuts, and falling business revenue. Thus, the premiums and out-of-pocket costs in employer health plans, which were already high for many with low and moderate incomes,4 could become an even larger share of shrinking household budgets.

President-elect Joe Biden and other policymakers have proposed addressing these affordability concerns by removing the barrier, or firewall, between employer coverage and marketplace subsidies. Doing so could allow more people to reduce the cost burden of employer coverage.5 In this analysis, we use data from the Current Population Survey in the two years prior to the pandemic to examine how much nonelderly people were spending on employer plan premiums on average relative to their income. We compare that to the burdens they could potentially face in marketplace plans at two different levels of subsidies — current-level subsidies and more generous subsidies.

What Is the Employer Coverage Firewall?

The ACA established a barrier, or firewall, to marketplace subsidies for people who have an affordable offer of comprehensive coverage through their employer. If employers do not offer comprehensive and affordable coverage to their employees, they face a federal tax penalty.

Workers with incomes between 100 percent and 399 percent of the federal poverty level ($26,200 and $104,800 for a family of four in 2021) who have employer premium expenses that exceed 9.83 percent of their income are eligible for marketplace subsidies, which triggers the employer tax penalty. This penalty is also triggered if the actuarial value of an employer’s plan is less than 60 percent (i.e., covers less than 60 percent of an employee’s costs, on average).

But there’s a catch: both provisions only apply to single-person policies. This so-called family coverage glitch has left millions of low- and middle-income families with expensive family plans unable to qualify for marketplace subsidies. The Urban Institute has estimated that more than 6 million people may be negatively impacted by this coverage glitch.6

Findings

Current Employee Premium Burden

As of 2019, around 160 million nonelderly people received health insurance through their employer.7 Although a majority of people with employer coverage have incomes of 400 percent of the federal poverty level or higher, more than 40 percent of people earn less than that amount.8

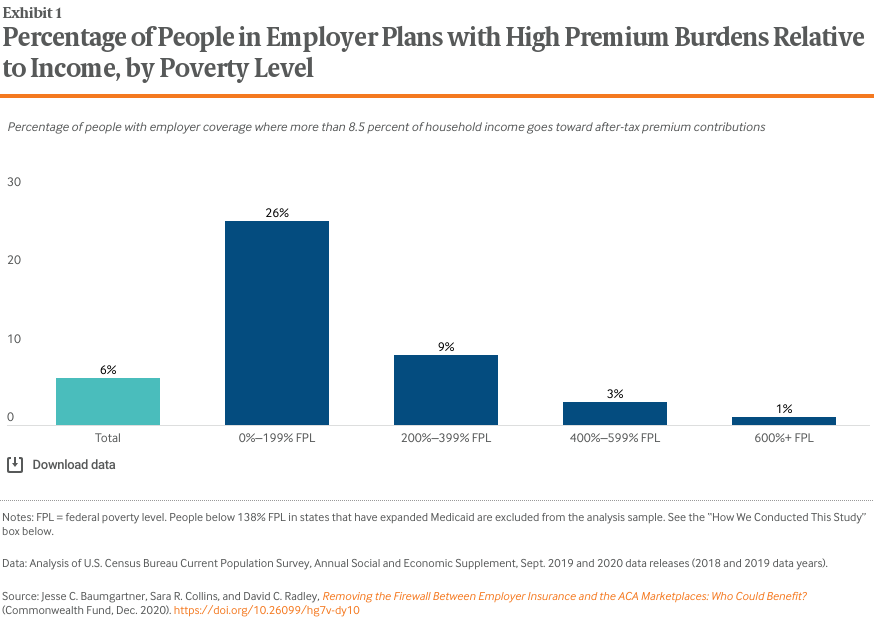

Entering the pandemic, an estimated 26 percent of nonelderly people with employer coverage in the lowest income group of our analytic sample (below 200% of poverty; $25,520 for an individual and $52,400 for a family of four in 2021) lived in households spending more than 8.5 percent of their income on after-tax premium contributions.9 In addition, nearly 10 percent of people with incomes between 200 percent and 399 percent of poverty ($51,040 for an individual and $104,800 for a family of four in 2021) spent this much on premiums (Exhibit 1, Table 1).

Firewall Reform Options and Analysis Approach

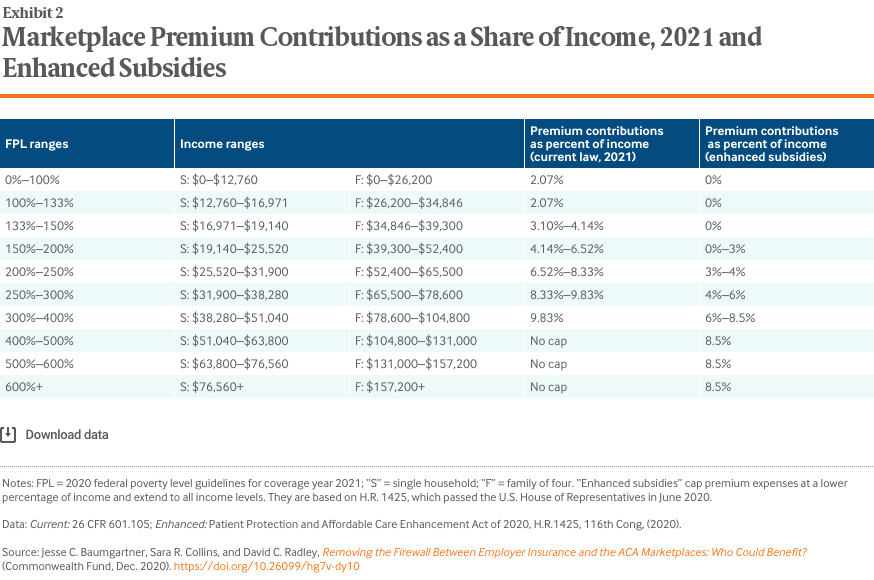

Several health care reform proposals, including President-elect Joe Biden’s, aim to lower people’s premium costs by enhancing and extending marketplace tax credits. These subsidies cap premium expenses at a percentage of income that increases as incomes rise.10 Some proposals also would remove the employer coverage firewall (see “What Is the Employer Coverage Firewall?”) and allow people with employer coverage with incomes between 100 percent and 399 percent of poverty to choose a plan and be eligible for these subsidies.

We examined the potential effects if the firewall were removed, allowing nonelderly people with employer coverage to buy marketplace plans under two different premium subsidy schedules (Exhibit 2):

- The current 2021 marketplace premium tax credit schedule11

- A schedule with enhanced premium subsidies that extends to all income levels and is linked to a gold-level benchmark plan that covers a greater percentage of average costs than the current silver-level benchmark plan12

The enhanced subsidy schedule is based on the Patient Protection and Affordable Care Enhancement Act (H.R. 1425), which passed the U.S. House of Representatives in June 2020.

We used the 2018 and 2019 Current Population Survey to calculate what percentage of income a household covered by an employer plan was paying toward premiums. We adjusted these payments to reflect the estimated tax benefits associated with employer-provided health insurance. We then compared it to the percentage that the household could potentially pay for a subsidized benchmark marketplace plan if the firewall were removed.

Although people with incomes below the federal poverty level are not currently eligible for marketplace subsidies, our analysis assumed a policy change in which all people with employer coverage could access them. However, we did exclude households below 138 percent of poverty ($17,608 for an individual, $36,156 for a family of four in 2021) in Medicaid expansion states from the analysis because they are likely to be eligible for Medicaid (see “How We Conducted This Study”).

Estimated Effects

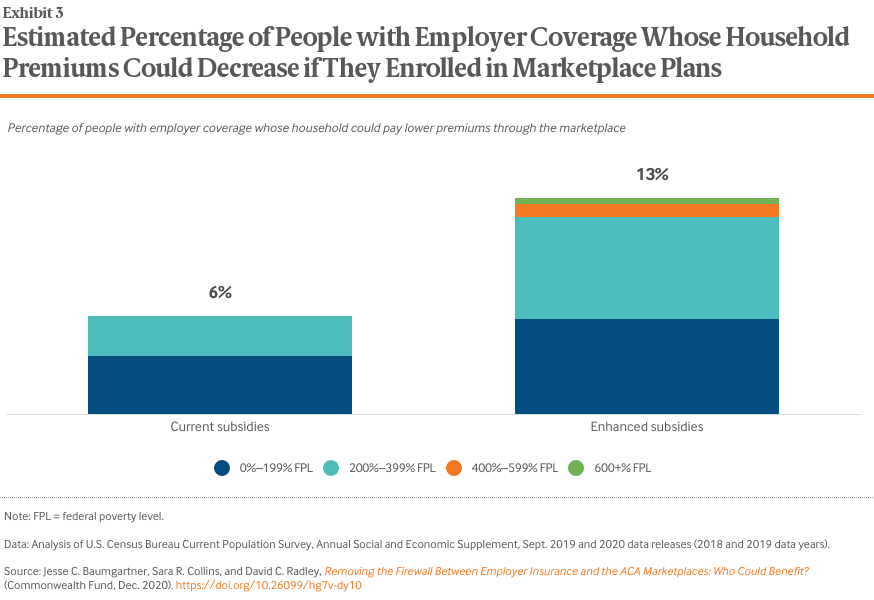

Under the two subsidy options, between 6 percent and 13 percent of people with employer coverage could pay a lower amount on premiums by enrolling in a marketplace plan (Exhibit 3, Table 1).

People in the two lowest income groups would benefit the most (0%–199% of poverty, $25,520 for an individual and $52,400 for a family of four; and 200%–399% of poverty, $51,040 for an individual and $104,800 for a family of four in 2021). They are the only groups currently able to access marketplace subsidies, which do not extend past 399 percent of poverty, and they make up the vast majority of those who could benefit from the enhanced subsidies.

People with incomes below 250 percent of poverty also receive subsidies to help with cost-sharing when they purchase marketplace plans, which significantly lower the amount they pay for copayments, deductibles, and coinsurance, as well as their annual out-of-pocket limits.13 Research shows that out-of-pocket spending can significantly burden people in employer plans with low to moderate incomes14 and deter their use of health services.15 At least two-thirds of the people in employer plans who could benefit from either the current or enhanced marketplace subsidies also could be eligible for these lower cost-sharing plans (data not shown).

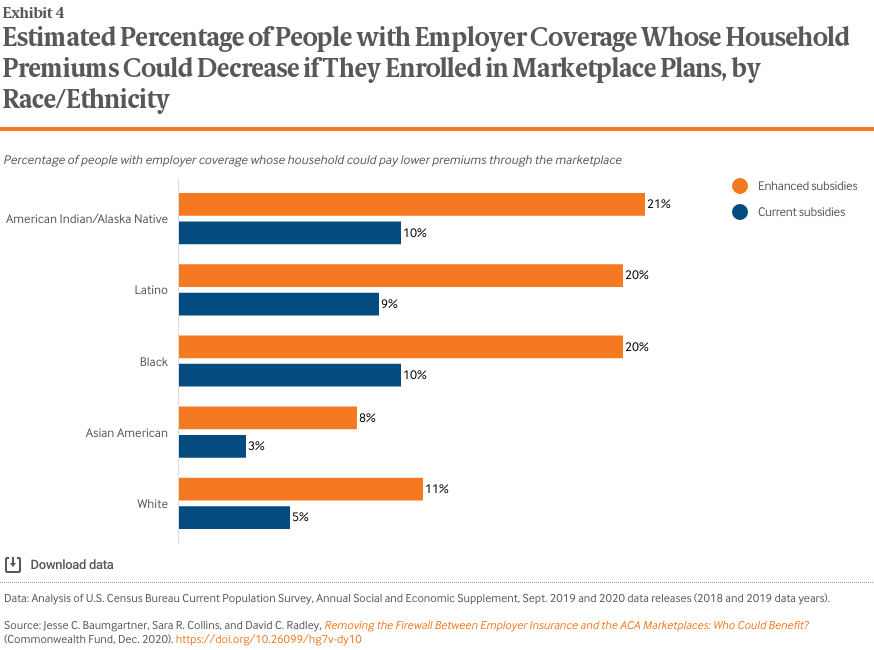

Larger shares of Black, Latino, and American Indian or Alaska Native individuals with employer plans could see lower premiums compared to white and Asian American people under each of the two subsidy options (Exhibit 4).

These three communities were all less likely to have employer coverage than white and Asian American people, but larger shares of those who did paid a high relative premium burden in their employer plans (spending greater than 8.5% of income; see Table 1).16

Estimated Regional Effects

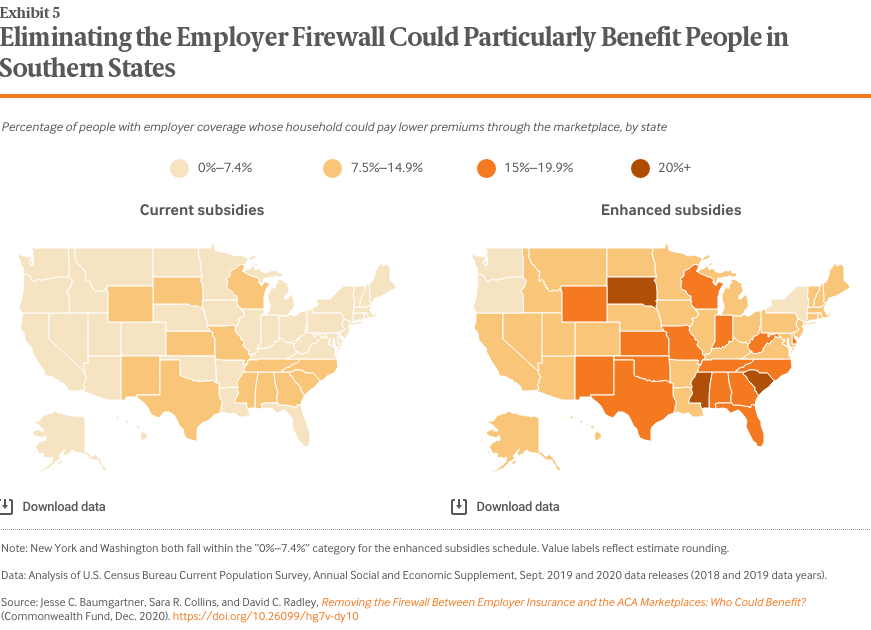

Because marketplace premium subsidies are pegged to income level, the potential effects of these policy changes could vary widely across states with different levels of average incomes and health care costs. We mapped the percentage of people in employer plans in each state whose household could pay lower premiums through a subsidized marketplace plan (Exhibit 5).

Larger shares of people in employer plans in southern states could face lower premium burdens under both subsidy options compared to those in other regions of the country (Table 2). Employee premium contributions in these states tend to be higher relative to median income, as highlighted in a recent Commonwealth Fund study.17

Policy Implications

This analysis indicates that removing the firewall between employer plans and subsidized marketplace plans could provide financial relief to many low- and middle-income employees facing premium costs that are high relative to their incomes. If the pandemic-related recession continues to slow income growth, more people in employer plans may be eligible. Removing the firewall also would eliminate the well-documented “family glitch” that currently blocks millions of people from accessing subsidies. The enhanced subsidy option, which uses an identical tax credit schedule to that proposed in a Congressional bill (H.R. 1425) that passed the House of Representatives in 2020, significantly increases the estimated effects of this reform.

There are important implementation issues to consider. Research has demonstrated that marketplace plans may lead to a greater out-of-pocket burden than employer plans.18 This is a particular problem for people with incomes above 250 percent of poverty who don’t qualify for cost-sharing assistance ($31,900 for an individual and $65,500 for a family of four in 2021). Some consumers may choose to keep their employer plans despite higher premiums, although others may trade lower premiums for higher cost-sharing.19 This choice could lead to adverse selection in employer plans, raising premiums in those plans. It is also unclear how employers would respond to the option: Would they design employer plans to incentivize sicker employees to opt for marketplace plans, which could increase marketplace premiums? How many employers might stop offering coverage altogether? These behavioral uncertainties also have significant implications for federal budget costs.

These questions and others can help shape complementary policies to ensure greater affordability for people with employer coverage:

- Increasing the marketplace’s benchmark plan to a “gold” level. Premium subsidies are based on the benchmark plan, and gold-level plans have a significantly higher actuarial value that is similar to that of employer coverage on average (80% versus 70% for current benchmark silver plans).20 This has been proposed by President-elect Biden, among others, and would result in higher subsidies and less out-of-pocket costs for marketplace consumers.21

- Requiring employer contributions. If the firewall were removed, employers may want to incentivize certain groups of employees to enroll in the marketplace to save costs (at the federal government’s expense). Policymakers could address this possibility by requiring employers to pay the government an amount equal to what they were previously spending on an employee’s health care, as Senator Elizabeth Warren proposed in her presidential campaign’s single-payer health plan.22

- Introducing a public option. President-elect Biden and other policymakers have proposed a choice of a public-option plan in the marketplaces that would have the power to negotiate provider and pharmaceutical prices.23 If a public-option plan were able to attract significant enrollment, it could use its negotiating leverage to drive prices down for the entire individual market and limit the growth of overall health care costs. An Urban Institute analysis found that a public option combined with additional reforms could achieve near-universal coverage while actually lowering overall national health spending.24

- Filling in the Medicaid expansion gap. People in Medicaid expansion states with incomes under 138 percent of poverty have Medicaid as a lower-cost option — regardless of whether they have access to an employer plan. But 12 states still have not expanded. Federal policymakers could allow people who would otherwise be eligible for Medicaid to enroll in marketplace plans with low or zero premiums, as we did within this analysis. President-elect Biden has proposed this.

- Increasing Medicaid enrollment outreach. Our study sample excluded people with employer coverage with incomes under 138 percent of poverty in Medicaid expansion states because they are likely already eligible for Medicaid as a low-cost insurance option. But this group still includes millions of people in employer plans, and our analysis (not shown) indicates that many are paying more than they would under a Medicaid plan. Expanding federal and state outreach efforts could let more families know they are eligible for Medicaid.

- Immigration reform. Undocumented immigrants are not currently allowed to use the marketplace or its subsidies, even if the firewall were removed. Comprehensive immigration reform could make a significant difference toward ensuring that these communities can more easily access health insurance.

How We Conducted This Study

This analysis uses data from the U.S. Census Bureau’s Current Population Survey (CPS), Annual Social and Economic Supplement (ASEC). The ASEC includes the self-reported amount of money that people spend on health insurance premium contributions each year. We used both the 2018 and 2019 data years (2019 and 2020 data releases) to ensure adequate sample size for state-level estimates.25 CPS respondents were grouped into households based on the CPS-provided tax unit, and premium spending and income were aggregated and reported at the tax unit level. The Census Bureau found that income data for 2019, collected in March 2020, potentially overestimates household income as the result of a nonresponse bias introduced by data collection issues as travel and social distancing restrictions for COVID-19 were beginning to be implemented. We have adjusted 2019 incomes downward to account for this bias, using discount estimates from the Census Bureau.26

To maximize the likelihood that we were only capturing premium costs for employer coverage, we followed past methodology by limiting our population base to households in which all members are under age 65 and have employer coverage, and at least one member is a primary policyholder for an employer plan.27 Removing these limitations does not change the study results.

We excluded all households with incomes below 138 percent of the poverty level who live in states that have expanded Medicaid under the ACA, because most are likely eligible for Medicaid as a lower-cost option.28 The final analysis sample included approximately 145,000 respondents across more than 64,000 tax unit households, corresponding to an annual weighted, nationally-representative population base of approximately 137 million individuals.

For our analysis, we first calculated the percentage of income that a household was currently spending on premium contributions for employer coverage. To limit the effect of outlier values for very-low-income households, we followed past methodology by bottom-coding household income at $100. To account for the tax benefits of employer-sponsored insurance expenses, we followed past analyses29 and adjusted premium contributions for the tax unit downward by an estimated effective marginal individual income plus payroll tax rate. This rate was taken from 2018 and 2019 marginal rate estimates from the Urban Institute and Brookings Institution Tax Policy Center, based on the tax unit’s income group.30

We then compared that percentage to what the people in a household might pay for a benchmark marketplace plan under two different sets of income-based premium subsidies (Exhibit 2):

- The current 2021 marketplace subsidy schedule

- An enhanced schedule of subsidies which extend to all income levels and are capped at 8.5 percent of income.31

Although households under 100 percent of poverty are not currently eligible to use marketplace subsidies, our analysis assumed a policy change in which all people with employer coverage could access subsidies. These households could access the most generous subsidy level on the schedule (2.07% of income for current subsidies; 0% for enhanced subsidies). This assumption only affected low-income households in Medicaid nonexpansion states because those within expansion states were already excluded.

Under each scenario, we compared a household’s income to the annual 2018 or 2019 federal poverty level guidelines32 to establish potential eligibility for a marketplace subsidy. We then calculated how many individuals could access a subsidized benchmark marketplace plan with lower household premium costs than their current employer coverage.

One limitation of the analysis is that it does not account for undocumented immigrants with employer coverage, who may appear eligible for marketplace subsidies or Medicaid but are not currently allowed to access either. Another limitation is that the analysis does not capture smoking status, and tobacco users may be issued a surcharge by insurers depending on their state and plan. Finally, state income taxes are not incorporated in the marginal individual income plus payroll tax rate discount. Doing so would lower the estimated after-tax cost of employer-sponsored insurance even further.

Acknowledgments

The authors thank David Blumenthal, Liz Fowler, Barry Scholl, Chris Hollander, Paul Frame, Jen Wilson, Munira Gunja, and Gabriella Aboulafia, all of the Commonwealth Fund, for providing constructive guidance and editorial and production support; and Naomi Zewde of City University of New York, for helpful discussion around the analysis approach.