Introduction

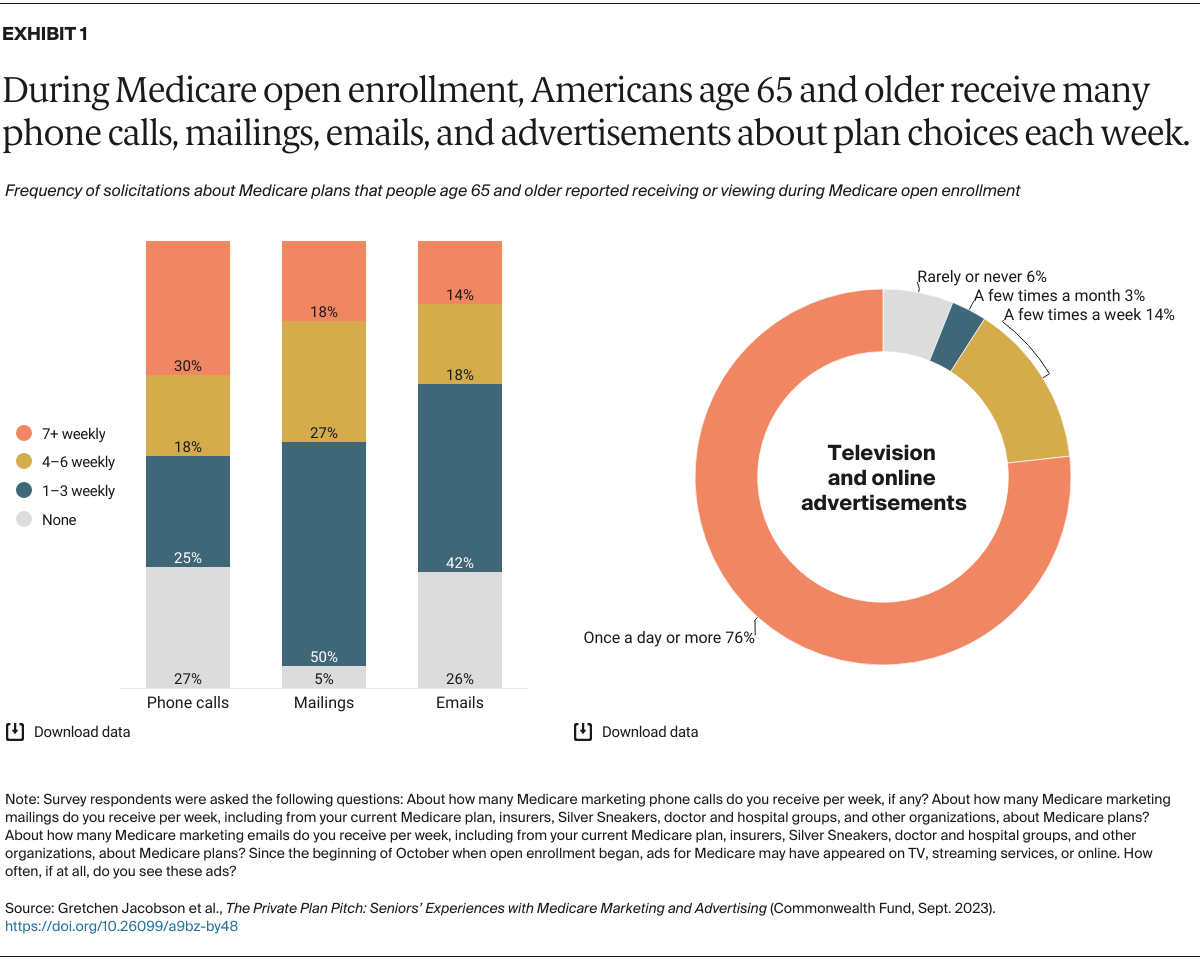

During Medicare’s annual open enrollment period, marketing pitches from private plans are seemingly everywhere. They can be seen on TV and the web. They’re on highway billboards and in brochures in physician waiting rooms. And they’re targeted to beneficiaries through email and phone calls. All types of Medicare plans are advertised, from Medicare Advantage plans to Medigap supplemental and stand-alone drug plans.

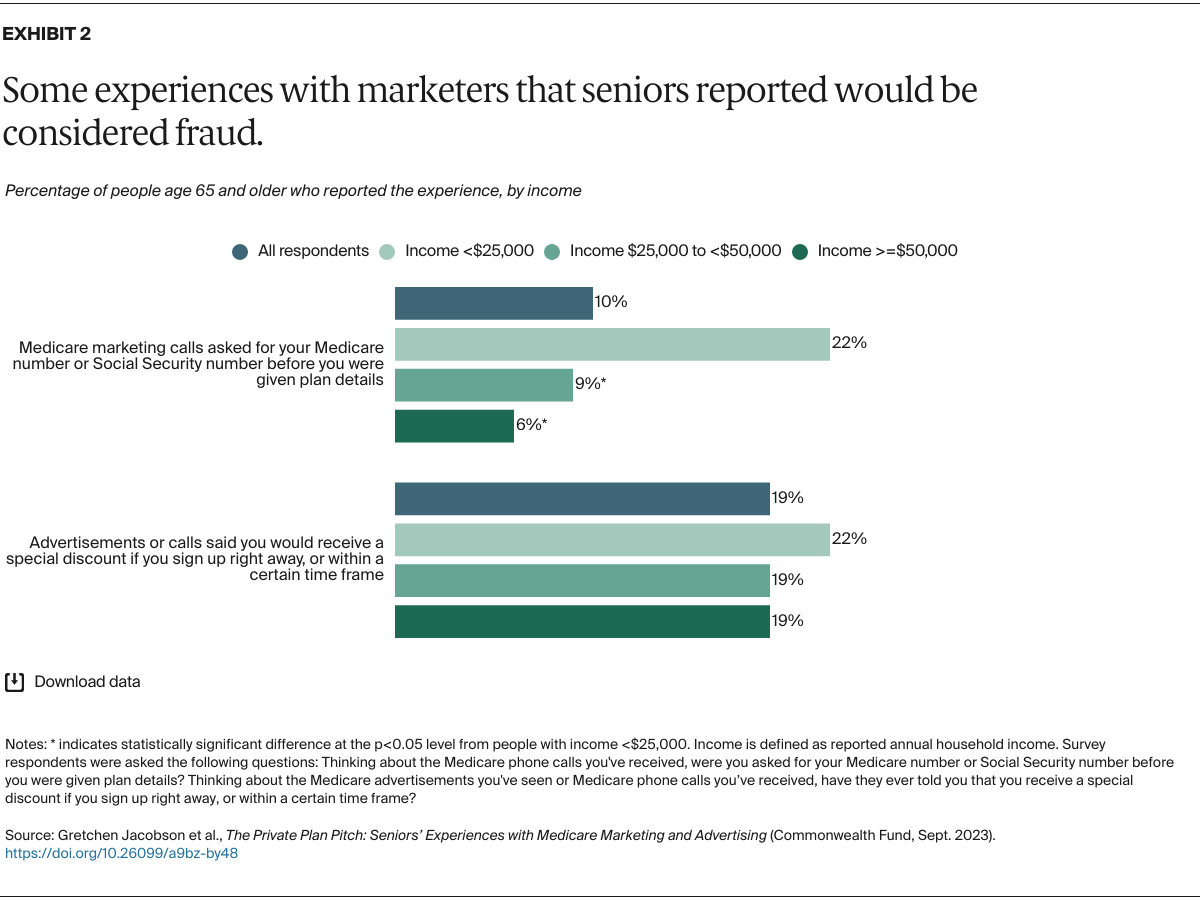

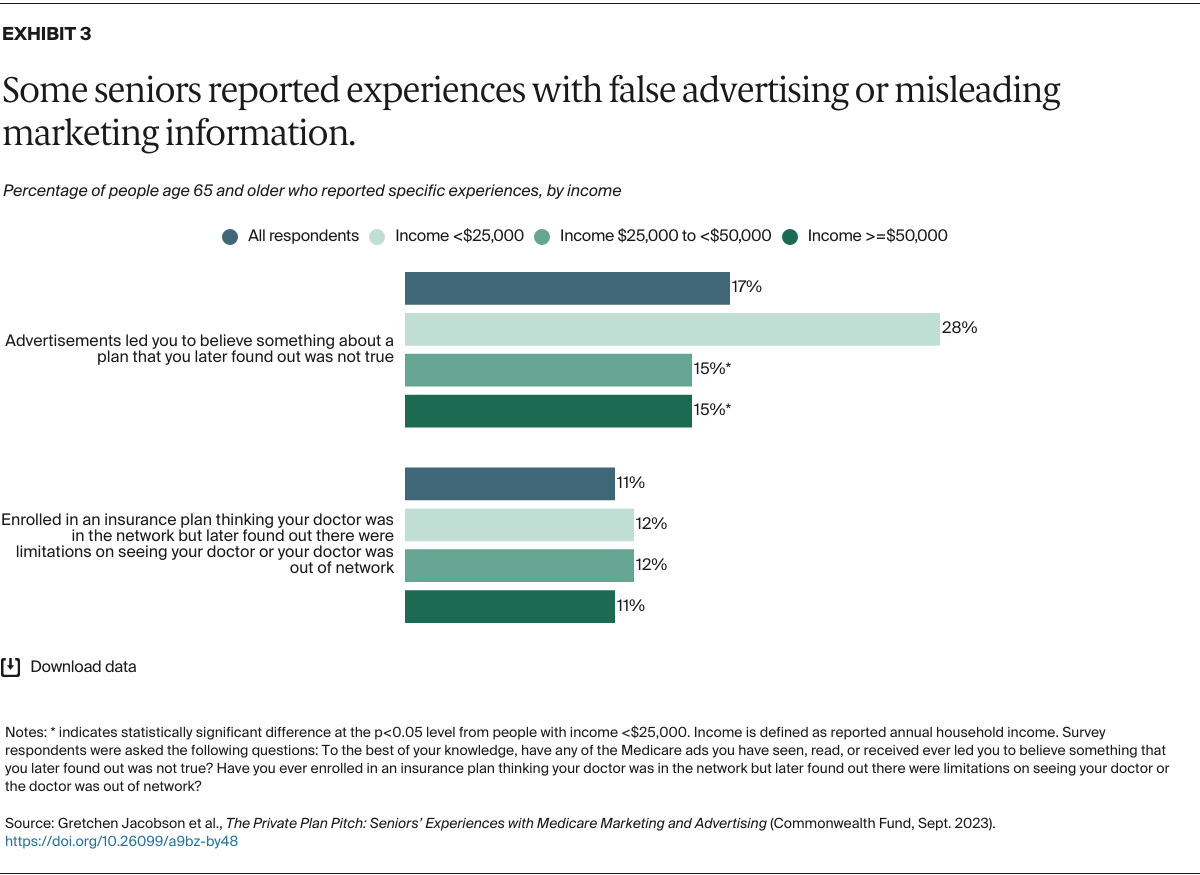

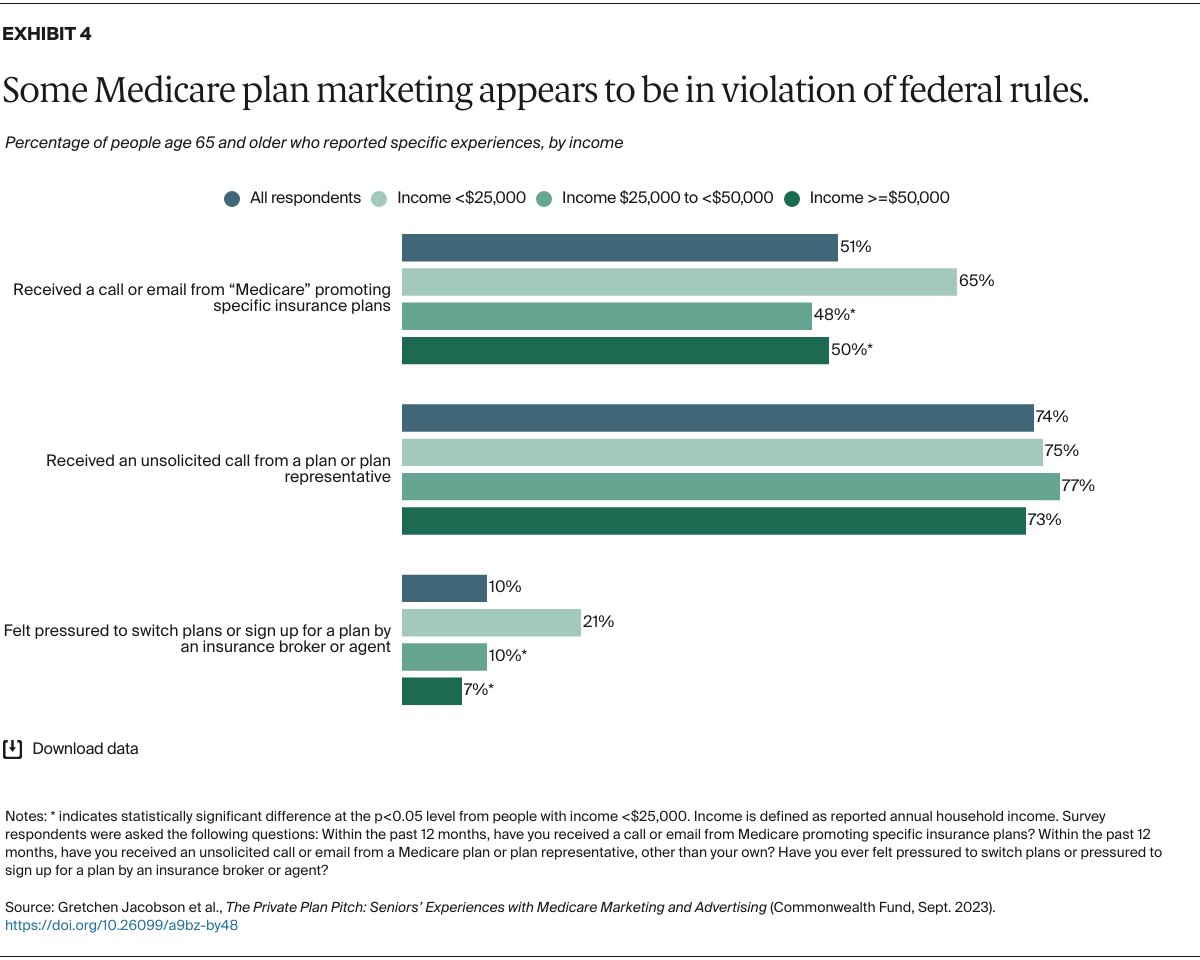

The proliferation of this marketing has led to an increase in complaints in recent years, with beneficiaries and brokers reporting confusing and misleading sales tactics.1 In response, the Biden administration has implemented several regulations in the past year to rein in Medicare plan marketing practices.

We asked people age 65 and older about their experiences with plan marketing and advertising efforts and how they may have informed their Medicare coverage decisions.2 Between November 30 and December 8, 2022 — a period covering the latter part of the 2023 open enrollment period for coverage beginning January 1 — the Commonwealth Fund and SSRS partnered to survey a nationally representative sample of 2,001 U.S. adults age 65 and older.

Below we present statistically significant findings from our survey. To learn more about how the survey was conducted including the sampling method, see “How We Conducted This Survey.”