Abstract

Issue: The Affordable Care Act aims to make private health insurance affordable for low-income individuals, but those with incomes above 250 percent of the federal poverty level face limited cost-sharing protections. While marketplace plans achieve premiums 15 percent to 23 percent lower than employer-sponsored insurance, they often do so through high cost-sharing requirements.

Goal: To analyze deductibles and out-of-pocket maximums in plans offered by insurers and evaluate a proposed reform designed to enhance coverage affordability.

Methods: We examined plan features in silver and bronze plans, comparing lowest- and highest-premium options from representative insurers in five regions. We analyzed deductibles and out-of-pocket maximums and estimated reform impacts using the Health Insurance Policy Simulation Model.

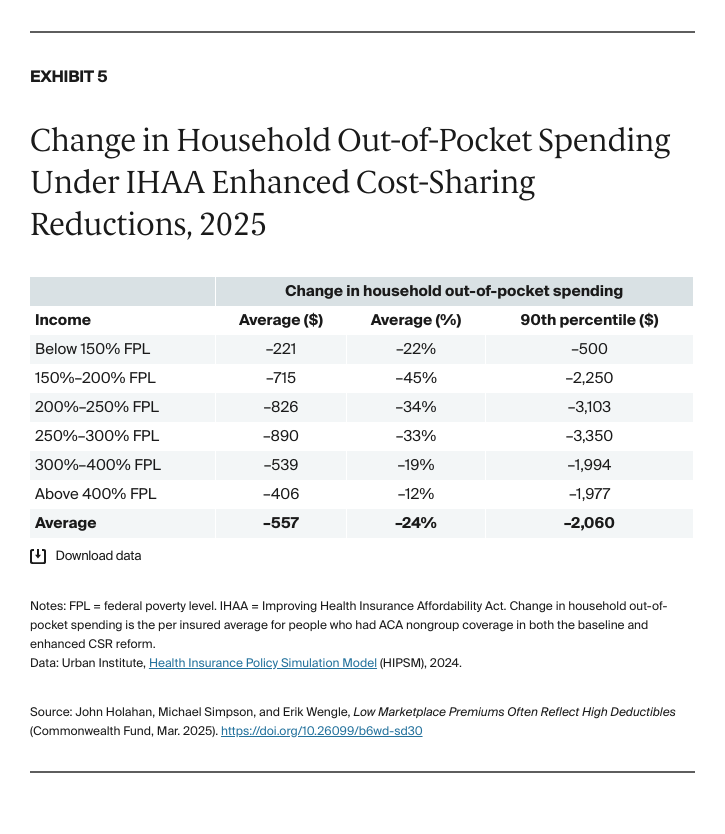

Key Findings and Conclusions: Silver-plan deductibles typically exceed $5,000, while bronze plans approach $7,500 — representing up to 21 percent of annual income for those at 250 percent of poverty. Out-of-pocket maximums are generally above $9,000 at both metal tiers. While higher-premium options offer lower deductibles, they often include substantial prescription drug deductibles. A proposed ACA reform would shift the benchmark plan from silver to gold coverage and expand cost-sharing subsidies, reducing out-of-pocket spending by an average of 24 percent at an estimated annual federal cost of $15 billion.

Introduction

The Affordable Care Act’s (ACA) marketplace insurance plans do not have particularly high premiums. A recent study that adjusted for age, benefit generosity, and the presence of cost-sharing subsidies revealed that premiums for marketplace plans were between 15 percent and 23 percent lower than for employer-sponsored insurance (ESI).1 Much of this difference was attributed to lower provider payment rates and narrower (more limited) provider networks. The finding suggests that ACA health plans could be financially attractive options for people who do not have ESI and are not eligible for Medicaid.

As we show in this brief, however, marketplace plans also achieve low premiums in part through lower plan generosity, which is often reflected in very high deductibles. Plans typically cover between 60 percent and 70 percent of an enrollee’s health care expenses — less generous than most ESI plans, which usually cover 80 percent or more. That means health care obtained through ACA plans can still be unaffordable for many low- and middle-income people.

Insurers in the ACA marketplace compete for enrollees by keeping premiums low and offering financially attractive plans. The federal government provides tax credits that cover the difference between a percentage of enrollees’ household income (which varies based on income level) and a benchmark premium (described below). As household income decreases, the premium subsidy increases.

Tax credits are tied to a silver-tier “benchmark” plan offered within each rating area (a geographic region that determines ACA health insurance premiums).2 People who select plans with premiums higher than the benchmark must pay the difference. This creates strong incentives for insurers to keep premiums low, particularly since research has shown that while some enrollees will pay higher premiums for plans with a recognized brand name or broad provider networks, price remains the primary factor.3

Notably, an individual or family can use the tax credit for the benchmark plan to purchase a bronze plan (which pays approximately 60 percent of incurred medical costs), resulting in premiums, after tax credits, that are often close to zero. Alternatively, applying the benchmark tax credit to a gold plan can make insurance with more benefits relatively inexpensive.

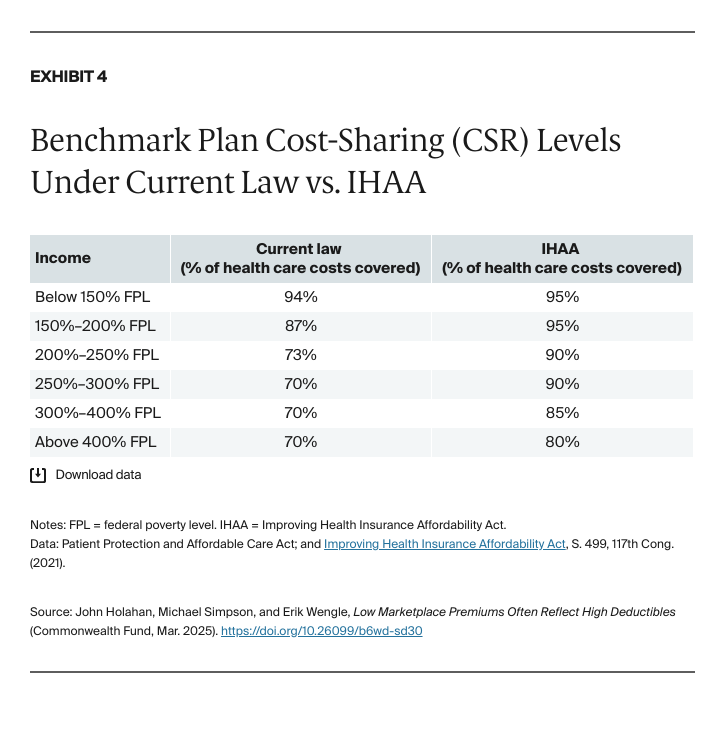

The decision to choose plans with low premiums and high deductibles, versus higher premiums and lower deductibles, depends in part on income. For instance, individuals and families with income below 250 percent of the federal poverty level (FPL) receive cost-sharing reduction (CSR) payments alongside premium subsidies. These CSR payments enable consumers with incomes below 150 percent of FPL, for example, to access plans that cover 94 percent of costs and have an average deductible of $90.4 Given these benefits, there is little incentive for low-income households to pay more in premiums to obtain a lower deductible.

However, CSR benefits disappear once income rises above 250 percent of FPL. Above this level, consumers could decide to pay more in premiums than the benchmark rate to reduce their deductible. The choice reflects individual preferences and does not affect government costs.

We examine whether marketplace coverage provides affordable access to care for those not eligible for CSRs, focusing particularly on the impact of high cost sharing (deductibles and out-of-pocket maximums). This question is crucial to determine if the marketplaces provide affordable options for low- and middle-income working families without access to ESI.

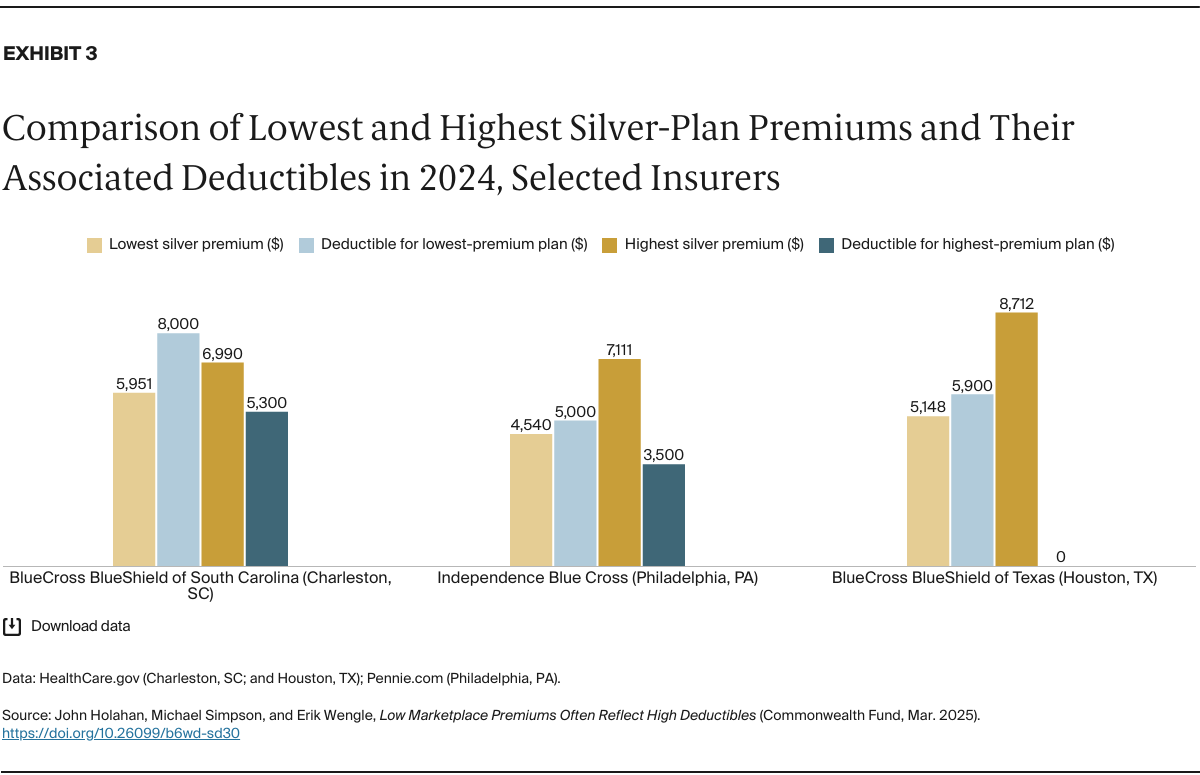

Our analysis focuses on silver and bronze plans of representative insurers in five urban rating regions, examining the relationship between premiums and cost-sharing features. We specifically investigate the deductibles and out-of-pocket limits associated with low-premium plans, while also analyzing how much deductibles can be reduced by paying higher premiums for plans offered by the same insurers.

Key Findings

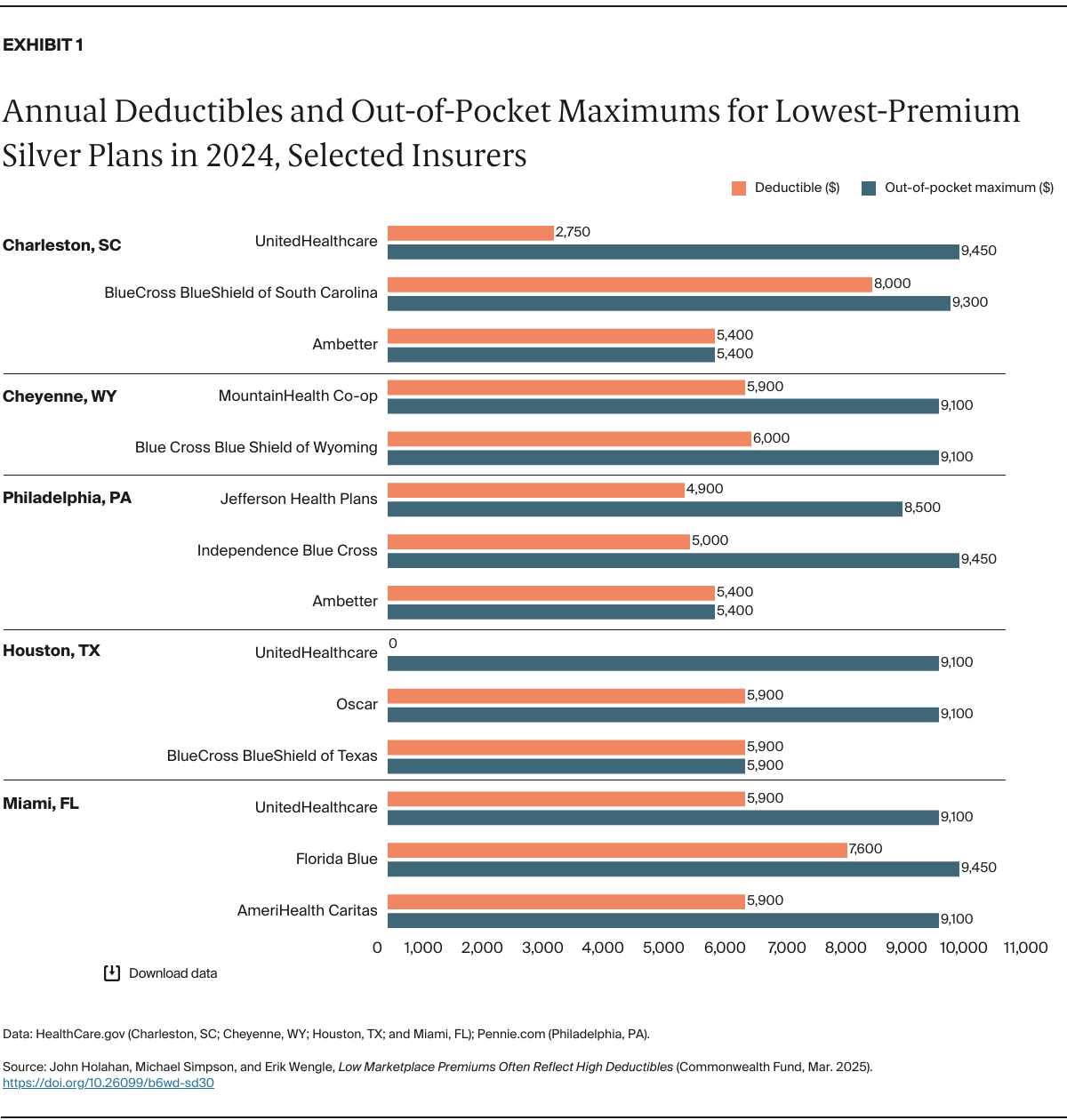

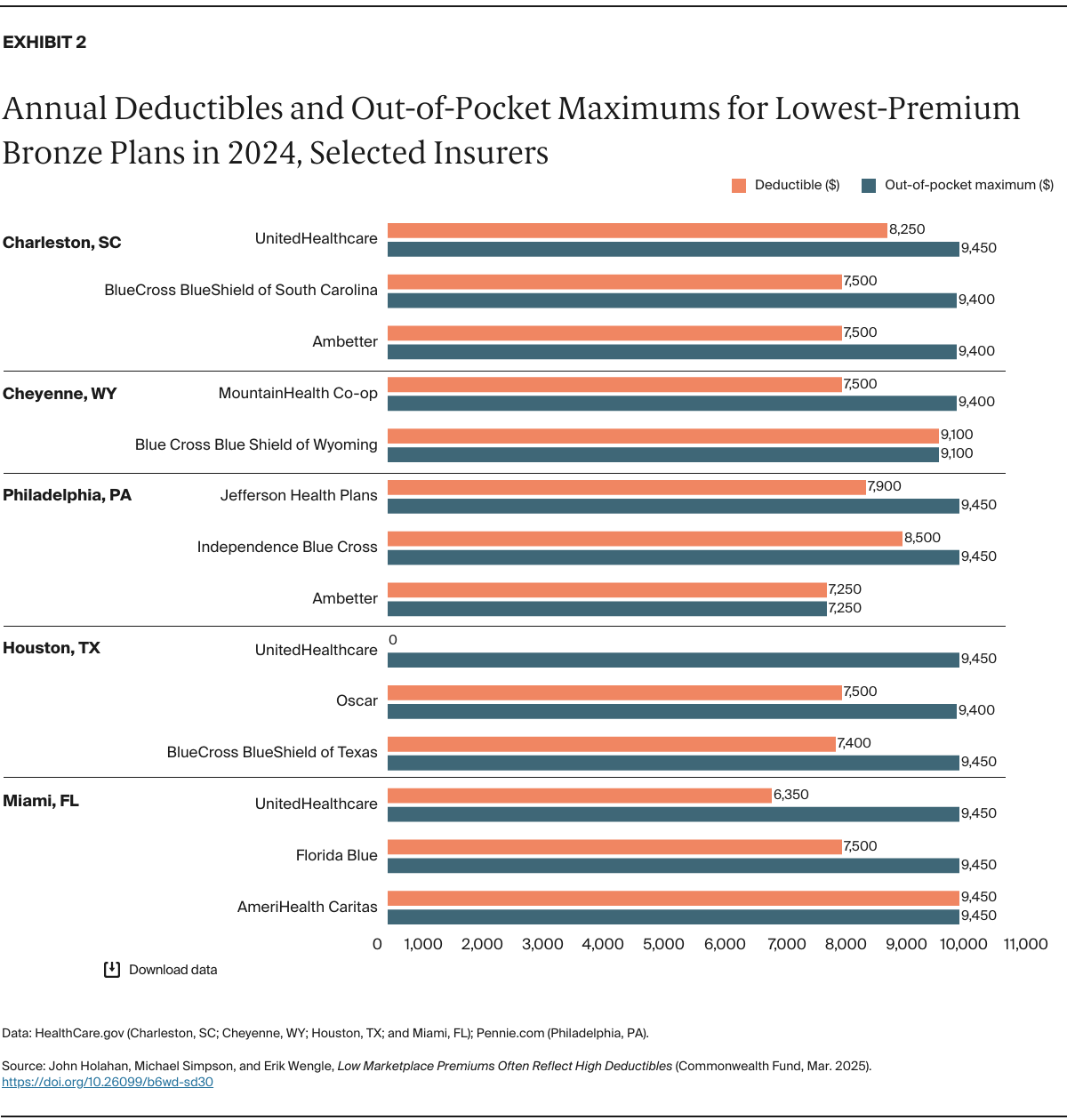

Our analysis examines plan features across five representative regions that span large and small cities and high- and low-cost markets: Charleston, South Carolina; Cheyenne, Wyoming; Philadelphia, Pennsylvania; Houston, Texas; and Miami, Florida. For each region, we analyze up to three insurers’ silver and bronze plans, focusing on deductibles and out-of-pocket maximums; for three regions, we also compare premiums and deductibles for insurers’ highest- and lowest-priced silver-tier options.5 For all plans, we show unsubsidized monthly premiums for a 40-year-old nonsmoker, along with their corresponding deductibles and out-of-pocket limits.6

The key patterns in marketplace plan deductibles and out-of-pocket costs are shown in Exhibits 1 and 2. Silver-plan deductibles typically range from $5,000 to $6,000 — significantly higher than the $1,800 average annual deductible for single coverage in ESI in 2024.7 In Miami’s marketplace, AmeriHealth Caritas and UnitedHealthcare set deductibles at $5,900, which would be over 16 percent of annual income for individuals earning just above 250 percent of FPL ($39,125 for an individual in 2025) — more than four times their share of the premium cost. Identical deductible levels appear in Houston for BlueCross BlueShield and Oscar.

UnitedHealthcare seemingly stands out as a notable exception in the Charleston and Houston markets. However, while the insurer eliminates the overall deductible in Houston and offers a lower $2,750 deductible in Charleston, these plans include separate prescription drug deductibles of $2,500 and $3,500, respectively. Out-of-pocket maximums for silver plans are generally $9,100 or higher — equivalent to 25 percent of annual income for individuals at 250 percent of FPL. Some insurers align their out-of-pocket maximums with their deductibles: Ambetter caps both at $5,400, while BCBS of Texas sets both at $5,900.