READ ABOUT OTHER ASPECTS OF MEDICARE ADVANTAGE

Background

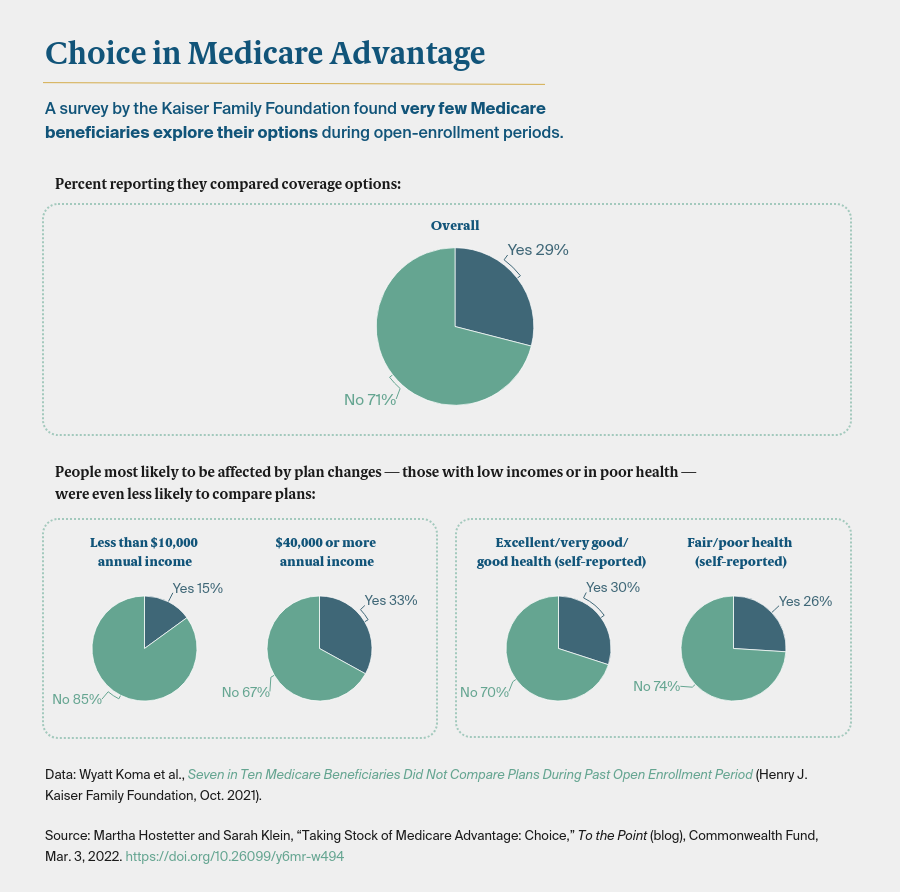

This year, the average Medicare beneficiary will choose from among 39 Medicare Advantage plans, the highest number in a decade. While a dozen rural counties still have no plans, in certain U.S. markets there are more than 50 plans available. But are beneficiaries able to choose the plan that’s best for them?

The health economists and Medicare experts we spoke with said choosing among plans can be difficult, even for the savviest consumers. First, beneficiaries must opt out of traditional Medicare, then choose a plan type (such as HMO or PPO) and determine what premium levels, copayments, and other parameters meet their needs. Many callers to the help lines run by State Health Insurance Assistance Programs — which most beneficiaries don’t make use of — are confused by basic insurance terminology.